Now that we’re officially into the new year, here’s a market update from the holiday-shortened week. The final week of 2025 brought limited economic data releases, but the updates we received were largely positive. We’ll cover December’s housing and labor market indicators, the growing disconnect between consumer sentiment and spending behavior, and how declining interest rates are affecting automotive retail sales heading into 2026.

On Thursday, Jan. 8, we will host the Q4 Manheim Vehicle Value Index call. Register to attend.

Pending Home Sales and Jobless Claims

Last week, we received updates on both pending home sales and jobless claims.

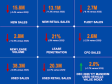

- Pending home sales showed growth of 2.6% year over year through November, exceeding estimates with 3.3% monthly gains, according to a report released by the National Association of Realtors. Compared to last year, pending home sales are up the most in the South, followed by the West. However, the month-over-month figures show the most growth in the West, registering 9.2% growth against October’s figure. The higher reading for the month showed the strongest performance of the year on a seasonally adjusted basis, and the best reading in almost three years.

- Jobless claims have trended lower for three weeks in a row, hitting 199,000 for this last week of December, a figure almost 5% lower than last year’s level. Continuing Claims also declined in the last week but remain 2.1% higher than last year.

Consumer Sentiment and Spending

Consumer sentiment has risen again in December but remains lower against last year. Meanwhile, the updated reading on consumer spending shows more evidence of a slowdown in December.

- Morning Consult’s daily consumer sentiment tracker is now down 3% from last year but higher by 3.8% from the end of November, on top of a 2.6% gain last month. It appears the end of the government shutdown in the second week of November pushed most consumers to feel somewhat better, though readings held lower against year-earlier levels.

- Going into the holiday season, many consumers indicated they were planning on reducing their spending this season, and updated data from Bloomberg appear to reflect those feelings. This week’s reading showed the fifth consecutive week of negative year-over-year growth in consumer spending, a key factor to watch as many market participants look for signs of slowdown in the economy more broadly. Weakness in consumer spending typically shows up first in discretionary big-ticket purchases like vehicles, making these trends particularly relevant for automotive markets

Interest Rates and Automotive Sales

Interest rates declined through December, providing relief for consumers during a critical retail period.

- The average Fed Funds rate in December fell 16 bps from November following the Fed’s rate cut earlier in the month. Though the 10-year Treasury yield remained relatively flat, auto financing rates improved: new vehicle APRs declined 13 bps while used rates dropped 25 bps, bringing both to their lowest levels in a year.

- New retail sales in December were averaging 4% lower year over year, with days’ supply down 2%, according to the latest reading from our Cox Automotive data.

- Used retail sales in the month were down roughly 1% through the third week of December, resulting in days’ supply running about 6% higher in the most recent week.

- While results are down month to date, we did see improvement in sales week over week for both new and used metrics.

Bottom Line

December’s data present a mixed picture for automotive markets heading into 2026. While lower interest rates provided meaningful relief – with auto APRs hitting their lowest levels in a year – sales remain muted, with new retail down recently despite the rate improvements. This disconnect suggests rate relief alone may not be enough to offset broader consumer caution.

The tension between rising consumer sentiment and weakening spending is particularly notable. Consumers report feeling better following the government shutdown resolution, yet actual spending behavior tells a different story, with five consecutive weeks of year-over-year declines. This gap matters for dealers: Optimism doesn’t translate to showroom traffic when consumers are holding off on making purchases.

Labor market stability, evidenced by declining jobless claims, provides some foundation as we end 2025, but the consumer spending slowdown in big-ticket categories like vehicles warrants close attention. The late-month improvement in weekly sales offers a glimmer of momentum, and we know consumers are about to enter a strong tax refund season. As we enter the new year, watch whether rate improvements can finally convert positive sentiment into actual sales.