New research by Cox Automotive on Chinese automakers shows a polarized U.S. market, limited brand awareness, and a wide gap between consumer curiosity and dealer readiness — highlighting why low prices alone may not be enough for Chinese brands to succeed if they enter the U.S. market.

Five insights shaping the conversation

As Chinese automakers continue to dominate global EV headlines, questions about U.S. entry are intensifying. This research explores how consumers and dealers actually feel — and what those perceptions signal for automakers, retailers and the broader market.

Consumer sentiment toward Chinese auto brands is sharply divided. Younger, EV-oriented shoppers show meaningful openness, while older and domestic-loyal buyers remain resistant.

Consideration of Chinese Brands in the U.S.

extremely/very likely

not very/not at all likely

of Gen Z more likely

This polarization suggests early traction would be concentrated — not broad-based — creating both opportunity for targeted entry and vulnerability for specific incumbents. Understanding who sits on each side of the divide is critical as entry timelines move from “if” to “when.”

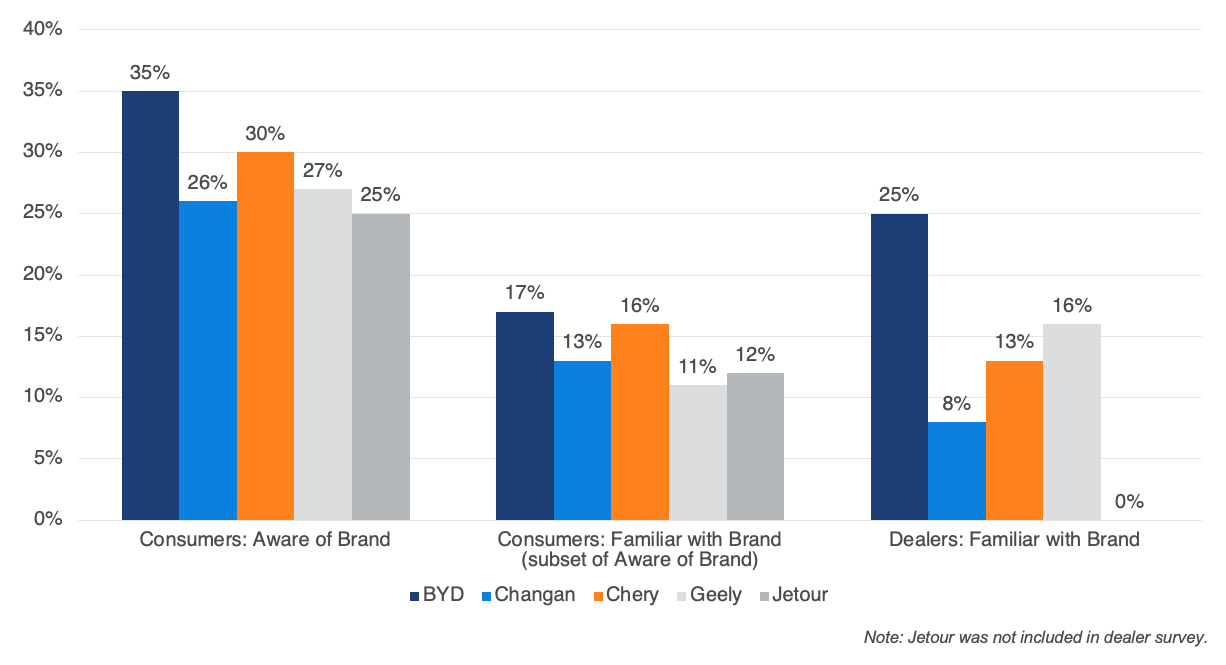

Nearly half of consumers say they are familiar with Chinese auto brands, yet that familiarity is largely superficial when asked about specific brands.

Chinese Brand Awareness and Familiarity

BYD leads awareness among consumers at 35%, but even the most recognized Chinese brand lacks a deep understanding among U.S. shoppers, with only 17% being familiar with the brand. This gap leaves Chinese automakers vulnerable to broad country-of-origin perceptions rather than product-specific evaluations — making education and credibility-building foundational to any successful entry strategy. Meanwhile, only a quarter of dealers are familiar with BYD.

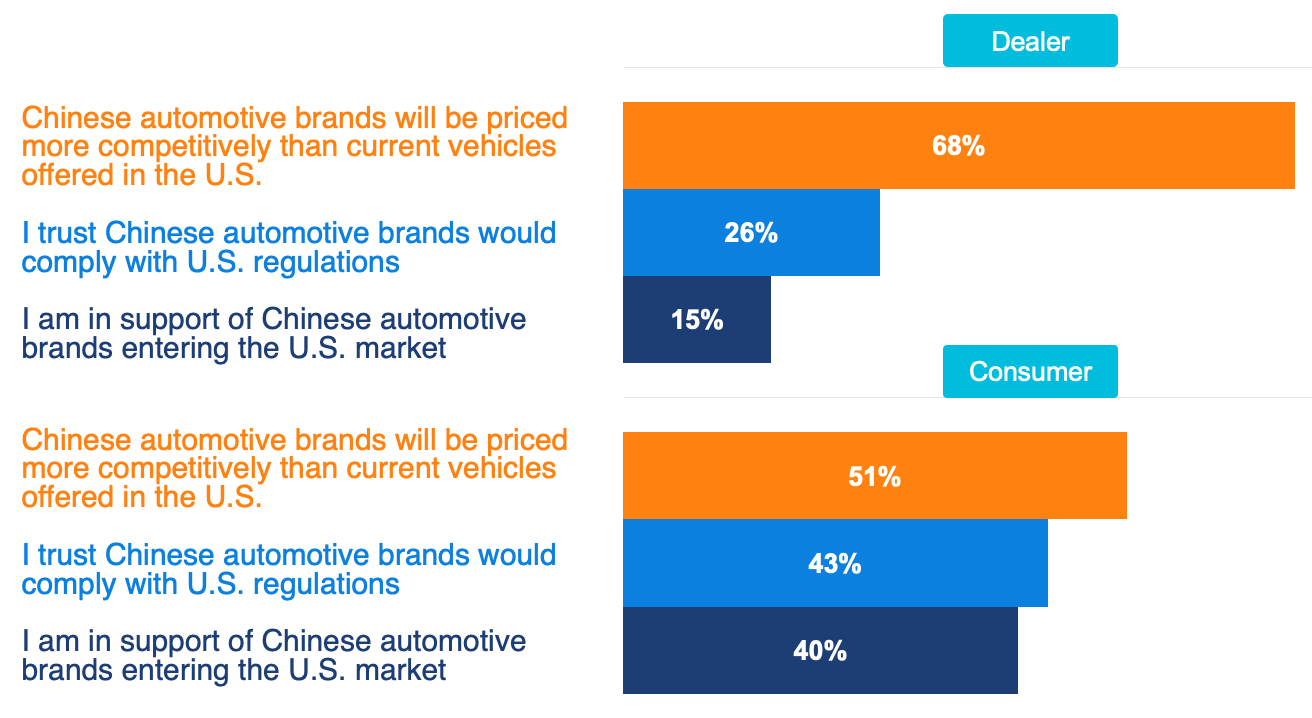

Dealers consistently underestimate consumer openness to Chinese brands. Consumer openness is notable, with 40% supporting Chinese automotive brands entering the U.S. market. By comparison, only 15% of dealers say they support such an entry. This gap matters — especially as partnerships emerge as a powerful credibility lever.

Dealer and Consumer Comparisons

(Strongly or Somewhat Agree)

In China, all foreign automotive brands were introduced to the market “partnered” with an established, local Chinese brand, and those partnerships for the most part remain today. If this same strategy were applied in the U.S., the dynamics would change.

When paired with an established U.S. brand, consumer consideration rises sharply to 76%, signaling that who a Chinese automaker aligns with may matter as much as pricing or product. For dealers, partnerships could accelerate acceptance while reshaping strategy. The research shows that 70% of dealers would change their strategies to stay competitive if Chinese brands entered the U.S.

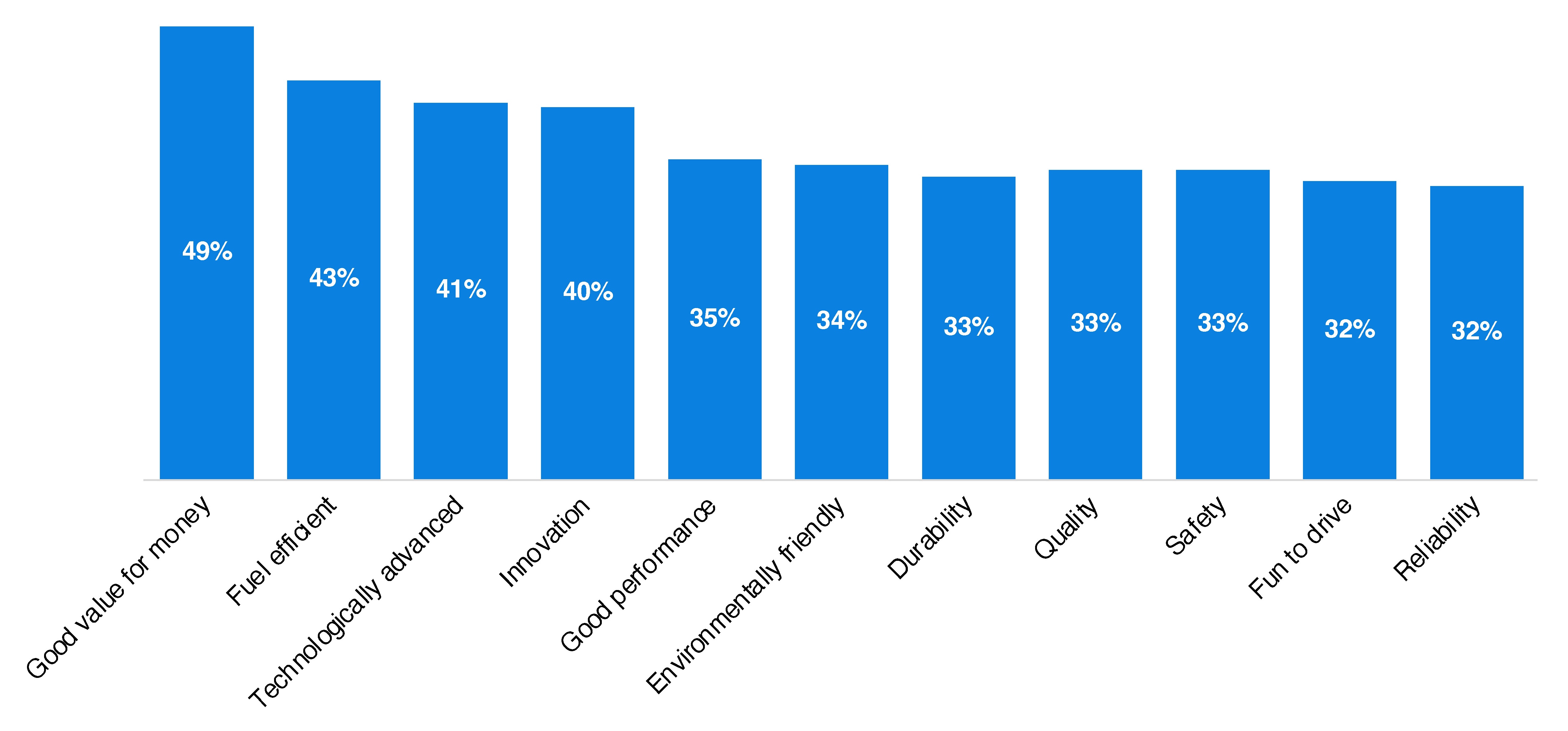

Affordability and fresh design generate consumer interest, but trust determines whether consumers follow through with a purchase.

Consumers Rate Chinese Brands Lower on Buying Criteria

(Durability, Quality, Safety and Reliability)

Consumer perceptions of Chinese automotive brands skew most positively toward value, with 49% of consumers rating them as excellent or very good for value for money. Performance also registers relatively well, earning strong marks from 35% of consumers. Views are more mixed on fundamentals such as durability, quality and safety, which each received top ratings from roughly a third of respondents, while reliability trails slightly.

Among dealers, the story is similar, with reliability, safety and long-term viability the significant concerns. This study shows that 92% of dealers have concerns about selling Chinese-brand vehicles. These trust gaps suggest that competitive pricing alone will not be enough; proof points, transparency and dealer support will be essential to changing perceptions.

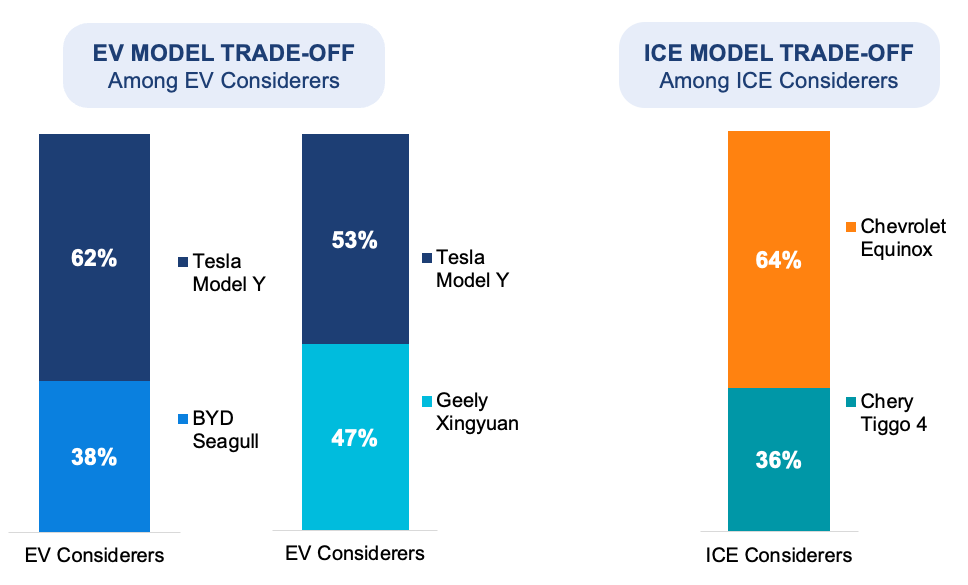

In direct comparisons with Chinese brands, U.S. brands maintain an edge — but not an unbreakable one.

Choosing Between Brands: U.S. vs. China

U.S. brands continue to hold the advantage when consumers weigh vehicles side by side, driven largely by trust, familiarity and brand equity. In both EV and ICE comparisons, Tesla and Chevrolet outperform Chinese competitors on overall appeal and purchase consideration, particularly when branding is visible. Tesla’s Model Y stands apart among EVs, while the Chevrolet Equinox maintains an edge among ICE models, reinforcing the strength of established U.S. nameplates.

That advantage, however, is not absolute. When price enters the equation, consumer preferences begin to shift. Trade‑off exercises show that a meaningful share of shoppers are willing to defect from U.S. brands when Chinese vehicles are offered at deep discounts. While Tesla and Chevrolet are still chosen more often overall, Chinese models gain ground quickly as price becomes the dominant decision factor, especially among lower‑income buyers and more price‑sensitive segments.

Methodology

This research is based on an online survey of 802 U.S. consumers who expect to purchase a vehicle within the next two years and identify as the primary decision‑maker in the buying process. The study was conducted between Dec. 29, 2025, and Jan. 2, 2026, and was designed to assess perceptions of Chinese vehicle brands, including awareness, appeal, consideration and openness to purchase. The sample includes consumers considering electric vehicles, hybrids and internal combustion engine vehicles, with natural overlap across powertrain consideration groups.

The Dealer Sentiment research was fielded from October to November 2025 and was conducted among 132 franchised dealers in management or sales roles.