Cox Automotive’s Auto Market Report video delivers a comprehensive analysis of the current automotive market. Chief Economist Jonathan Smoke leads our effort to translate data and trends into actionable insights. This video covers a wide range of topics, including consumer spending patterns, consumer sentiment, retail vehicle sales, financing rates, supply dynamics, pricing trends and leading indicators from Cox Automotive’s extensive data ecosystem.

Report Summary – Oct. 28, 2025

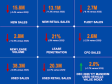

Key Highlights

- Consumer spending growth slowed in October, with sentiment and retail activity showing signs of strain.

- Auto loan rates have climbed, with new rates averaging 9.6% and used rates reaching 14.24%.

- Retail sales and supply trends are stabilizing, but dealer leads and service activity are down compared to last year.

Consumer Spending and Sentiment

Consumer spending growth decelerated in September and turned negative in early October before rebounding.

- The Index of Consumer Sentiment declined 3.3% in September and is down 3.8% so far in October.

- Slower spending and lower sentiment reflect ongoing economic uncertainty and higher costs.

Retail Sales Trends

New and used vehicle sales trended down for most of September but have shown modest recovery in October.

- Retail sales are rising as October begins, signaling some resilience in consumer demand.

- Dealer leads are up year over year on Autotrader but down on Kelley Blue Book, with overall leads lower than September.

Auto Loan Rates and Financing

Low-interest rate offerings have declined further in October, and average loan rates have increased.

- The average new auto loan rate is now 9.6%, while the average used rate has climbed to 14.24%.

- Unique credit applications per dealer are up just 1% year over year, with a declining trend in used loan applications.

Supply and Pricing

New and used days’ supply remain relatively unchanged, with used price trends for retail stronger than wholesale.

- The average MY 2022 retail price declined 0.4% last week, while wholesale prices fell another 0.7%.

- New and used supply levels have stabilized, but price pressures persist.

Cox Automotive Leading Indicators

- Dealer leads are up year over year so far in October on Autotrader, but down on Kelley Blue Book, and leads are down for the month compared to September on both sites.

- Unique leads per dealer are down year over year so far in October for new and used vehicles on websites hosted by Dealer.com, and new and used leads are down for the month compared to September.

- Unique credit applications per dealer on Dealertrack were up just 1% year over year last week, with the trend down week over week in aggregate, with a declining trend in used loan applications.

- Service trends on Xtime relative to last year declined in the week ending Oct. 18, as completed appointments were down 6% year over year.

Final Thoughts

Coming into this month, we expected slowing in October but not a collapse — in the vehicle market or in the broader economy — and that appears to be what is happening. Auto loan rates are higher, sentiment is lower, and the seasonal trend all point to lower sales from less urgency to buy. We think that the labor market is holding up, with consumers holding onto their jobs. November is not likely to see improvement, but maybe we can hope for the shutdown to end so that wet blanket is removed before December.