As expected, the Fed cut rate policy for a second time in 2025 at the conclusion of its seventh scheduled Federal Open Market Committee (FOMC) meeting. The policy statement from the FOMC was little changed, but Chair Powell made it clear that a decision to cut rates again in December was far from a foregone conclusion.

This meeting did not produce updated forecasts or expectations for rates in the future. The median expectation communicated in September was for two more cuts in 2025, but members were divided in their outlook. With the shutdown interrupting government data on the economy, labor market, and inflation, it is going to be a tougher call in December, the final meeting of the year. Today’s vote revealed divided views, with one voting member pushing for more cuts, as in September, and one pushing for no cut.

Perhaps the most notable aspect of today’s announcement was the official end of quantitative tightening (QT) on Dec. 1. QT places downward pressure on longer term rates, which have a greater impact on auto loans and mortgages. With the end of QT, the Fed will be seeking to maintain the size of its balance sheet and that will mean buying treasuries and possibly mortgage-backed securities as existing holdings mature. That buying activity should at least remove upward pressure on longer rates, including for auto loans.

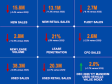

The Fed Funds Rate is now 3.75-4.00%, which is still considered to be restrictive, meaning there is room for additional cuts if risks to the labor market persist.

The 10-year U.S. Treasury bond moved 8 basis points (BPs) higher today to 4.06%. After today’s increase, the 10-year has fallen 9 BPs in October and is now down 51 BPs for the year. The average mortgage rate has fallen 24 BPs in October and is now down 93 BPs this year.

Auto loan rates, however, have moved in the opposite direction of bond yields and mortgage rates again in October, just as they did in September. The average new auto loan rate increased 32 basis points (BPs) in September to 9.41%, which was down 17 BPs year over year. In October, interest rates have increased another 19 BPs, leaving them down 24 BPs year over year.

A similar story has unfolded with used auto loans, as rates increased 25 BPs in September to 14.19%, up 22 BPs year over year, and have climbed another 5 BPs so far in October, leaving rates up 28 BPs year over year and roughly half-a-point below the 25-year peak reached in February.

(Worth noting: Consumers with credit scores of 760 or more are seeing average rates in October of 5.5% on new loans and 6.9% on used loans. Credit scores matter!)

It is important to remember that the recent moves in auto loan rates are not directly related to the Fed. New rates are moving higher mostly due to fewer special offers from the captive finance arms of the manufacturers. Fewer special, low-rate offers means an increase for prime-and-above borrowers who disproportionately benefit from the special offers.

Meanwhile, in the used market, average rates have moved higher mainly for subprime buyers as lender risk aversion by has increased in the wake of a few anomalous but high-profile bankruptcies in auto lending, which I posted about last week: Auto Loan Health, Separating Fact from Fear. These higher rates are not dissuading subprime borrowers, so the average rate for used loans has increased from the low point of 2025 measured in August.

Average auto loan rates are likely to remain high through November. December will bring more year-end rate offers in the new market, which should help pull the average rate back down. The used market is not likely to see rates decline until loan performance improves, and this is the time of year when loan performance always degrades.

The seasonal pattern suggests that loan performance should begin improving by March, and 2026 could see improvement start sooner as consumers benefit from reduced tax withholdings leading to higher take-home pay in January. Then, starting in February, we should begin to see the impact of record-high tax refunds.

As noted, Chair Powell made it clear that a cut is not guaranteed in December, but we still believe the Fed will cut one or two more times by spring. With loan performance likely to be improved by then as well, consumers should see average auto loan rates lower by a full percentage point or more by the summer of 2026, which is just one more reason we remain optimistic for improving conditions in the year ahead.