ATLANTA, Dec. 3, 2025 – The Q4 Cox Automotive Dealer Sentiment Index (CADSI) reveals a significant decline in dealer confidence as economic and market challenges persist. Market sentiment for both current and future conditions fell below the positive threshold in the fourth quarter, signaling caution as dealers face rising costs, higher prices and economic uncertainty, all contributing to weaker demand.

“Dealers are signaling caution as 2025 ends,” said Mark Strand, deputy chief economist at Cox Automotive. “Persistent economic uncertainty and fading consumer confidence are weighing on sentiment. Compared to the rest of the year, the current market feels like it’s running out of gas. As we look ahead at 2026, renewed market momentum is entirely possible, especially if we get material interest-rate relief and a rebound in consumer confidence.”

Key Findings from Q4 2025 CADSI

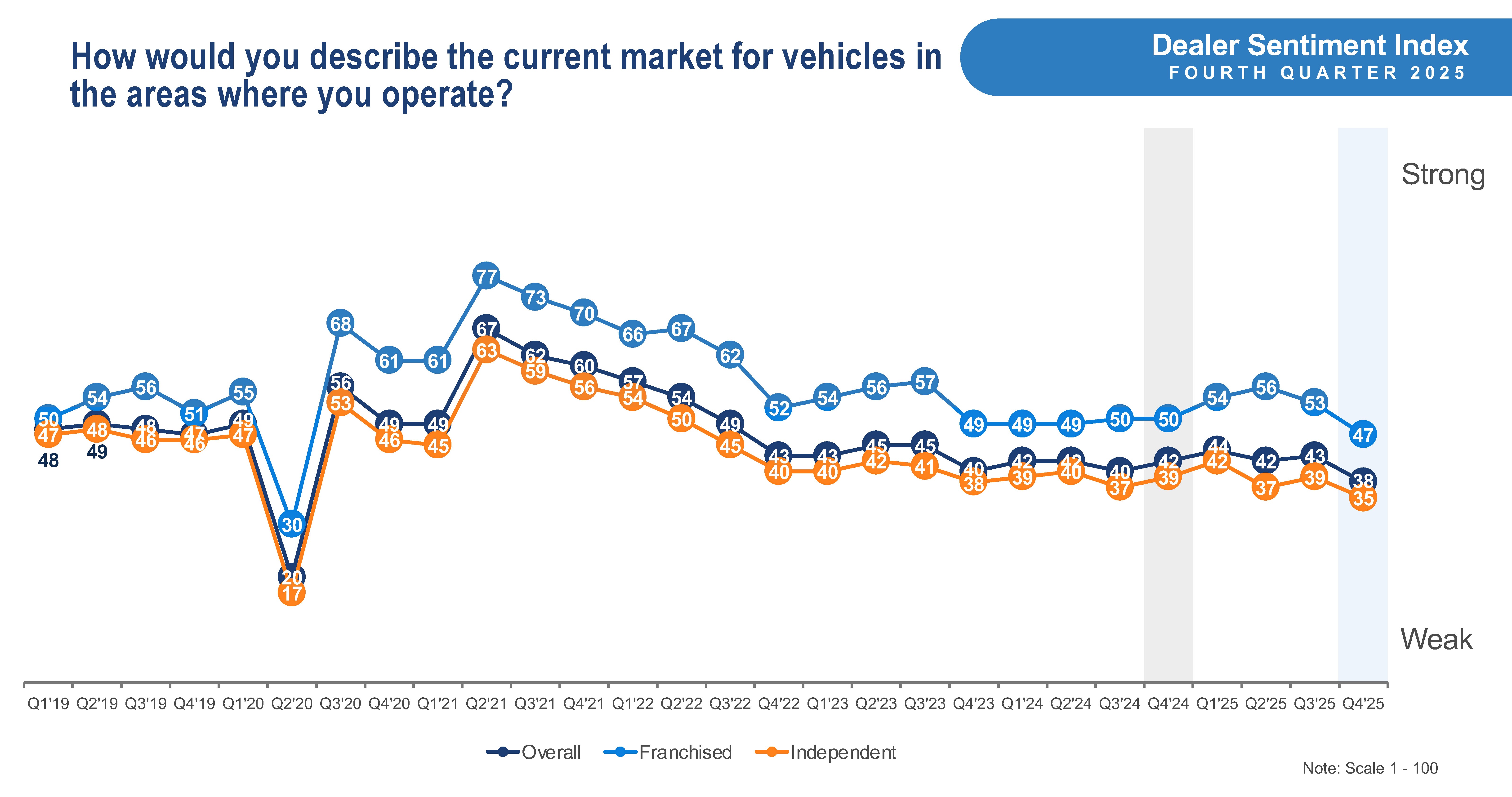

- Market Sentiment Drops Sharply: Current market index fell to 38 (from 43 in Q3), and future outlook declined to 42 (from 46), both well below the positive threshold of 50. Franchised dealers reported a current market index of 47, notably higher than independents at 35, but both groups saw declines and remain below the positive threshold, reflecting widespread caution.

- Customer Traffic Hits Record Lows: Overall traffic dropped to 31, with in-person traffic at 29 and digital at 40. The decline in customer traffic was especially pronounced for franchised dealers, with in-person and digital traffic both reaching all-time lows, while independent dealers also saw weak but less severe declines.

- Profitability Under Pressure: Profit sentiment declined to 36 overall, with franchised dealers at 44 and independents at 33, reflecting margin compression from rising costs and softer demand. The profitability gap between franchised and independent dealers persisted, with independents experiencing a more pronounced impact.

- Sales Environment Weakens: New-vehicle sales sentiment fell to 49 and used-vehicle sales to 42, both below 50, indicating a challenging retail environment. Franchised dealers saw new-vehicle sales sentiment fall to 49 and used-vehicle sales to 53, while independent dealers reported even lower used-vehicle sales sentiment at 39, highlighting tougher conditions for independents.

- Inventory Mixed: New-vehicle inventory increased slightly to 59, while overall used inventory remains tight at 43. Franchised dealers view their new-vehicle inventory as growing (59), while independent dealers continued to face tight used inventory (41), limiting their ability to meet demand.

- Economic Sentiment Declines: The economy index dropped to 39 from 43 in Q3, reinforcing concerns about macro headwinds. Both franchised (44) and independent dealers (37) saw economic sentiment decline, but independents expressed greater concern about macroeconomic headwinds.

- Electric Vehicle (EV) Outlook Slumps: Overall, dealer sentiment regarding the future of electric vehicle sales and leasing declined sharply in Q4, reflecting growing uncertainty and diminished optimism for the segment. Among franchised dealers, future EV sales sentiment dropped significantly to 24 (from 33 in Q3), and EV leasing sentiment fell to 27 (from 36), highlighting the most pronounced decline and the impact of expiring tax credits. Independent dealers continued to report lower engagement and less optimism in the EV segment, with sentiment remaining subdued and little change from previous quarters.

Q4 closes a turbulent year for automotive retail. After a brief tariff-fueled surge in Q2 and a spike in EV sales in Q3, the market has begun to show signs of slowing in Q4. Dealer sentiment has declined as the market slows, but if consumer confidence improves and auto loan rates start to trend lower, momentum and sentiment could recover in the first half of 2026.

Cox Automotive Dealer Sentiment Index Methodology

The Cox Automotive Dealer Sentiment Index (CADSI) is derived from a quarterly survey issued to a representative sample of franchised and independent auto dealers across the United States. The Q4 2025 CADSI is based on responses from 919 dealers, including 492 franchised and 427 independent dealers.

The survey, conducted from Oct. 22 to Nov. 6, 2025, measures dealer perceptions of current retail auto sales and sales expectations for the next three months as “strong,” “average,” or “weak.” Responses are weighted by dealership type and sales volume to represent the national dealer population. Indices are calculated by assigning values to responses: 100 for strong/increasing, 50 for average/stable, and 0 for weak/decreasing. Respondents who select “don’t know” are excluded from the index calculation. The reported metrics have a margin of error of +/- 3.23%.

About Cox Automotive

Cox Automotive is the world’s largest automotive services and technology provider. Fueled by the largest breadth of first-party data fed by 2.3 billion online interactions a year, Cox Automotive tailors leading solutions for car shoppers, auto manufacturers, dealers, lenders and fleets. The company has 29,000+ employees on five continents and a portfolio of industry-leading brands that include Autotrader®, Kelley Blue Book®, Manheim®, vAuto®, Dealertrack®, NextGear Capital™, CentralDispatch® and FleetNet America®. Cox Automotive is a subsidiary of Cox Enterprises Inc., a privately owned, Atlanta-based company with $23 billion in annual revenue. Visit coxautoinc.com or connect via @CoxAutomotive on X, CoxAutoInc on Facebook or Cox-Automotive-Inc on LinkedIn.

Media Contacts:

Mark Schirmer

734 883 6346

mark.schirmer@coxautoinc.com

Dara Hailes

470 658 0656

dara.hailes@coxautoinc.com