This edition of the Auto Market Weekly Summary includes updates on energy prices, benchmark interest rates and mortgages, consumer sentiment, and employment. The coming weeks will test whether tax refund dollars and continued credit availability can offset the headwinds building from energy prices and consumer uncertainty.

Bottom Line Up Front

The Middle East conflict is the defining economic story of the moment, and its reach is broad. Oil prices jumped over $110 per barrel late last week and retail prices were near $4. Inflation concerns have been reignited, effectively closing the door on a Fed rate cut in the foreseeable future. Treasury yields and mortgage rates have reversed late-February declines, erasing a brief window of affordability relief heading into the spring selling season. Consumer sentiment has moved lower in response, with one-year inflation expectations climbing to 3.8%.

For dealers, the picture is more balanced than the macro headlines suggest. Tax refund season is running strong — the average refund is just below $3,600, up 10.9% against last year, with $203 billion already returned to consumers as of March 20. Used-vehicle sales and wholesale pricing continue to reflect a healthy spring bounce, providing support for trade-in values and inventory positions. Credit availability remains near its highest level in over two years.

Energy Prices

With the conflict in the Middle East showing no signs of a quick end, the implications of higher-for-longer energy prices are seeping into inflation expectations, pushing out expectations for any Fed rate cut well into 2027 and raising the possibility that the next action could be an increase, not a cut.

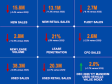

- Oil futures rose to over $111 per barrel—an increase of 60% so far in March and 55% year over year.

- Gas prices—likely the most-watched price for U.S. consumers—have climbed to a national average near $4 and are up 26% from last year.

Benchmark Rates and Mortgages

Both the 10-year Treasury yield and mortgage rates have moved higher over the course of March, after ending February on a lower note and providing some relief to consumers. The conflict in the Middle East has increased uncertainty as well as caused inflation expectations to rise, leading to upward pressure on interest rates.

- After briefly dipping below 4% in late February, the 10-year Treasury yield increased dramatically as concerns surrounding the Middle East conflict picked up this week, with yields rising to over 4.4% in the latest week.

- Mortgage rates for a 30-year contract climbed in response after ending February below 6%, a level that had not been seen since September 2022. Rates moved to 6.38% late last week, per Freddie Mac. Rates are roughly 30 bps below last year’s level but up substantially in March.

- With existing home prices higher by only 0.3% according to the National Association of Realtors, the average monthly payment for a home is $1,987, down 2.7% from a year earlier driven primarily by lower interest rates.

Consumer Sentiment

Consumer sentiment softened in March as inflation expectations rose and broader economic uncertainty weighed on outlooks, a trend echoed across multiple sentiment measures.

- The University of Michigan Consumer Sentiment Index revised report was lower than initially reported in March, falling to 53.3—a 6.5% decline year over year and down almost 6% for the month.

- Survey respondents also indicated they expected prices to increase 3.8% year over year, up from 3.4% in February. Inflation expectations for the next five years, however, remained at 3.2%.

- The Morning Consult Index of Consumer Sentiment fell to 88.7 last week, a decline of 6.1% in March and lower by 9% year over year.

Jobless Claims

Initial jobless claims continue to hold relatively steady, suggesting layoffs remain subdued despite heightened economic uncertainty.

- Initial claims rose to 210,000 for the week ending March 21, up slightly from 205,000 the prior week. The four-week moving average held steady at 210,500—near its lowest level since late January.

- Continuing claims fell to 1.82 million for the week ending March 14, the lowest level since May 2024, indicating that while hiring remains weak, it hasn’t deteriorated further.

- Claims remain below year-ago levels, down 7% year over year in the latest week.