This edition of the Auto Market Weekly Summary includes updates on new vehicle sales, the labor market, consumer credit, and Manheim values. Many market metrics showed signs of strengthening in late February, likely supported by improving weather across much of the country. At the same time, rising geopolitical tensions in the Middle East have introduced a new variable, pushing gas prices higher — a potential headwind for consumers as tax refunds hit their accounts.

Bottom Line Up Front

The spring selling season was showing signs of real momentum before running into a new wildcard. Tax refund season continues to deliver meaningful consumer purchasing power. Through Feb. 27, the average refund stood at just over $3,700, up 10.6% from a year earlier. Total dollars returned to consumers reached $137 billion, up 9%, even as the number of returns filed was down about 2% from last year’s pace. That tailwind is already showing up in wholesale markets, as the Manheim Used Vehicle Value Index surged in February to its highest levels since September 2023.

But geopolitical tensions in the Middle East have introduced a sudden headwind. Gas prices jumped more than 13% in the past week to $3.46, arriving precisely when consumers are weighing how to deploy their refund dollars. At the same time, interest rates reversed course, with the 10-year Treasury rising more than 10 basis points as markets price in a more inflationary environment.

For the automotive market, the timing is frustrating. Traffic patterns were just beginning to recover from the winter weather disruptions that weighed on January and early February. At this point, we do not expect the geopolitical impact to be long-lasting, but March warrants close attention as consumers react to both the news cycle and higher prices at the pump.

The labor market added a layer of caution this week as well. The economy shed 92,000 jobs in February, with negative revisions to prior months pushing the three-month average to just 6,000 jobs — a fragile backdrop for big-ticket discretionary purchases.

Consumer credit growth also decelerated in January, with total credit expanding at just a 1.9% annualized rate. For auto dealers, the near-term bridge provided by tax refund season remains intact, wholesale values are firm and the longer-term outlook is still favorable. The key question for March is whether that momentum can hold in the face of rising gas prices and a softer labor market.

New Vehicle Sales and Pricing

New-vehicle sales in February were lower than a year ago but improved from January. Cox Automotive’s weekly tracking showed sales running below last year’s pace for much of February, with activity beginning to strengthen late in the month. As evidenced in our Q1 Cox Automotive Dealer Sentiment Index, winter weather wreaked havoc in dealership traffic patterns in late January and early February, but subsided as the weather warmed across much of the US.

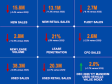

- February SAAR finished at 15.8 million, lower by 1.4% against last year, just above our estimate. The sales pace was up 6.3% from January.

- The sales volume in February was 1.197 million units, down 1.5% against last year’s rate, but up 8.5% from January.

- Fleet sales were essentially flat compared to last year, but higher by nearly 9% from January levels, driven by a 23% increase in commercial sales. Stellantis and General Motors showed the largest gains in February, while Nissan, Mazda, and Ford were lower.

- The vehicle average transaction price (ATP) rose 3.4% compared to February 2025, according to Kelley Blue Book estimates, and showed an accelerating rate of growth. The February ATP was higher by 0.3% from January levels, as the market started to heat up towards the end of the month.

- Incentives also moved higher as automakers and dealers worked to sustain momentum heading into spring. Incentives across the industry increased to 6.9% of ATP, up from 6.5% in January and slightly below last February.

- Additional details on the February ATP will be released on March 10.

Employment Trends & Retail Sales

February’s stark decline in jobs served as an acute reminder of the state of the labor market. While the unemployment rate remains relatively low and hourly earnings are still rising, the labor market looks more fragile even as the breakeven rate for job creation may be as low as 20,000 per month given tightening immigration policies.

- The economy shed 92,000 jobs in aggregate in February, driven by declines in health care, IT, and government roles. The January report was revised down slightly and the December reading went from positive 49,000 jobs to a loss of 17,000.

- Taken together, those revisions brought the three-month average for job creation down to just 6,000. The unemployment rate rose one-tenth of a point to 4.4%, while the labor force participation rate edged lower in the month.

- Average hourly earnings through February are 3.8% higher against last year.

- Retail sales grew 2.4% year over year in December, the smallest gain since February 2025 on an adjusted basis, as the pace of growth decelerated into year end. Preliminary reads for January sales show an acceleration to 3.2% growth year over year.

- Non-adjusted sales metrics for motor vehicles & parts were higher by 1.8% year over year in December, while new car dealer sales were only 1.5% higher. Early January estimates for auto dealers show a decline of 0.3% year over year on a non-adjusted basis.

Consumer Credit

The Federal Reserve’s latest consumer credit report, released Friday afternoon, came in below expectations and showed slower growth across both revolving and non-revolving credit.

- Total consumer credit rose by $8 billion in January, up 0.2% in the month, reflecting an annualized growth rate of 1.9%.

- Non-revolving credit increased 0.1% in the month, at an annual rate of 1.1%. The growth in December was at a 4.1% rate.

- Revolving credit was higher by 0.4% in the month, growing at an annual rate of 4.3%, and down from the 11.3% pace in December.

Manheim Values Hit Highest Level since September 2023

Wholesale values according to the Manheim Used Vehicle Value Index (MUVVI) surged to the highest levels since September 2023, as the MUVVI rose to 212.3, buoyed by solid dealer demand.

- Seasonally adjusted wholesale values were up 4% year over year and rose 0.8% in February alone, much stronger than the typical move for the month.

- Non-seasonally adjusted prices rose a 4.2% year over year and were higher by 3% from January.

- MMR prices for the Three-Year-Old Index jumped 3.1% in February, well above typical seasonal patterns.

- Demand strengthened further, with sales conversion at Manheim hitting 61.5%, above the three-year average.