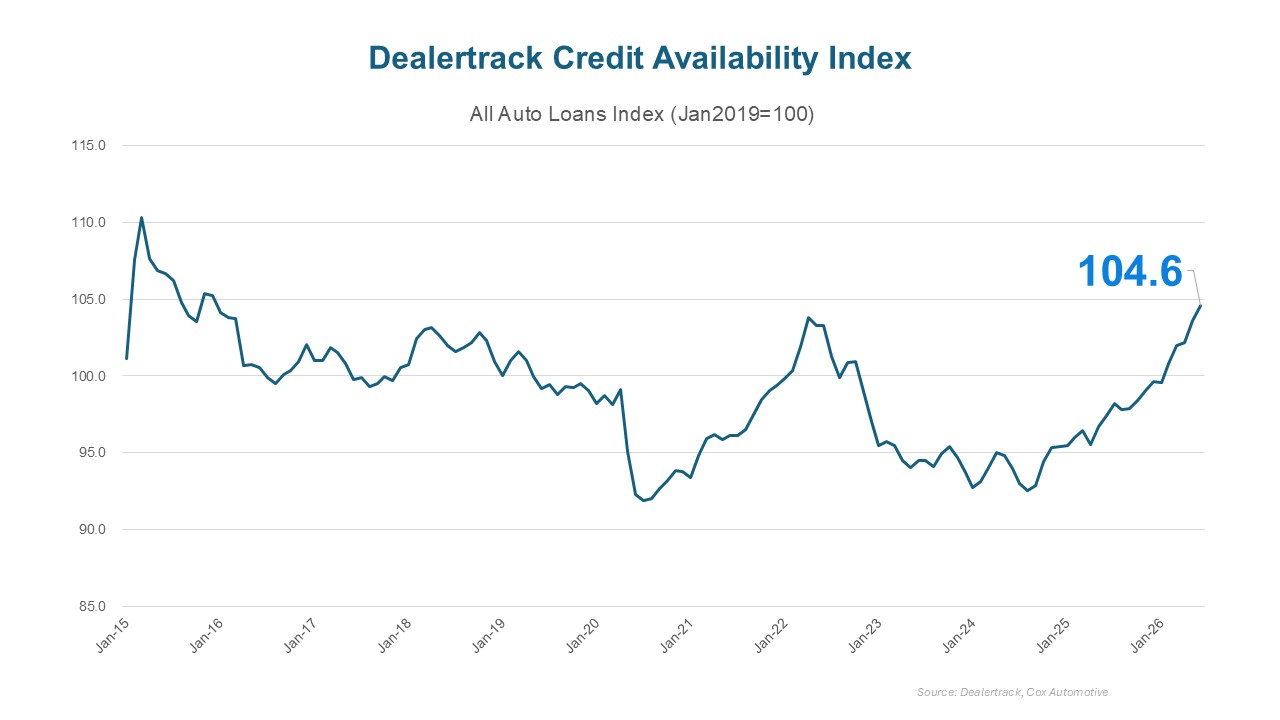

In June 2026, the Dealertrack Credit Availability Index rose to 104.6, its highest level in more than a decade. The All-Loans Index increased 0.9% from May’s 103.6, marking its fifth consecutive monthly increase, and a rise of 7.3% from June 2025.

The monthly gain was driven primarily by a sharp improvement in approval rates and a continued uptick in long-term loan share, with a modest widening in the yield spread. A further pullback in subprime share only partially offset those gains.

Key Metrics

- Approval Rates: The overall loan approval rate rose to 73.8% in June, up 170 bps from May, marking the largest monthly gain of 2026. Year over year, the rate is up 150 bps. The significant jump made approval rates the single largest contributor to June’s index gain.

- Subprime Share: The share of loans to subprime borrowers declined 10 bps month over month, to 16.6%, the third consecutive monthly decline following March’s surge to 19.5%. Despite three months of pullback, subprime share remains up 250 bps year over year, reflecting conditions that are still more positive for higher-risk borrowers than a year ago.

- Yield Spread: The yield spread widened 5 bps (from 6.72% to 6.77%), doing little to reverse May’s sharp 53 bps narrowing. The average contract rate rose 11 bps to 10.98%, a bit faster than the 5-year Treasury yield’s 6 bps rise to 4.21%, slightly widening the spread. Year over year, the spread remains down 43 bps from 7.2% in June 2025.

- Loan Term Length: The share of loans with terms greater than 72 months reached 31.1% in June, a new all-time high in the dataset and up 110 bps from May. The increase suggests lenders and consumers continue to stretch loan length to make deals work. Long-term loan share was the second-largest contributor to June’s index gain. Year over year, the share is up 410 bps from 27% in June 2025.

- Negative Equity Share: The share of loans with negative equity declined 30 bps, from 57%, the third consecutive monthly decline following March’s record high of 59.2%. Despite the monthly easing, negative equity remains up 220 bps year over, with most borrowers starting their new loan with a balance that already exceeds their vehicle’s value.

- Down Payment Percentage: Down payments declined 30 bps to 13.2%, after ticking up slightly in May, consistent with the largely flat trend seen throughout 2026. Down payment percentage is now running below year-ago levels of 13.7%.

Channel and Lender Trends

- Channels: Credit access improved unevenly by channel in June. Independent Used posted the largest monthly gain, up 2.2%, followed by All Used, up 1.3%, and Used CPO, up 0.3%. Franchise Used and All New were roughly flat on the month, while Non-Captive New declined 0.5%, the only channel to lose ground.

- Lender Types: All four lender types posted gains in June. Captives rose 1.8% and Finance Companies rose 1.6%, the largest monthly gains, followed by Credit Unions, up 0.7%, and Banks, up 0.2%.

Year-Over-Year Comparison

- Channels: All New posted the largest year-over-year gain, up 9%, followed by Independent Used, up 8%, and All Used, up 7%. Franchise Used and Non-Captive New each improved a little over 6%. Used CPO posted the smallest year-over-year gain, up 1.7%. All channels remain meaningfully above year-ago levels, with All New leading year-over-year gains.

- Lender Types: Captives led year-over-year improvement, up 14.9%, followed by Banks, up 13.4%. Finance Companies improved 8% and Credit Unions improved 6.9% year over year. All four lender types remain well above year-ago levels, with Captives and Banks continuing to lead year-over-year improvement.

Implications for Consumers and Lenders

- Consumers: June extended May’s gains, with financing becoming even more accessible on the strength of a further jump in approval rates. That improvement came alongside a slight uptick in borrowing costs: The average contract rate rose 11 bps to 10.98%, and the yield spread widened 5 bps. For consumers, this means more buyers gained access to financing in June, though at a marginally higher cost.

- The broader financing picture still carries the same cautions seen in prior months. The share of loans with terms beyond 72 months reached a new all-time high of 31.1% and negative equity remains above year-ago levels, even after three straight months of improvement. Down payments, at 13.2%, are running below year-ago levels as well. Longer terms combined with more negative equity and lower down payments increase total loan cost and risk exposure over the life of the loan.

- Lenders: The index reached its highest level since December 2015, and the gain was broad-based across lender types in June. The rise in approval rates points to a growing willingness among lenders to extend credit, reflecting looser underwriting standards and a broader risk appetite across the industry. The yield spread’s 5 bps widening in June is a reversal from May’s sharp narrowing, offering lenders a modest amount of margin relief after that compression, though it recovers only a small fraction of what was lost in May and the spread remains far tighter than it was heading into May.

- The continued pullback in subprime share is shifting the loan mix toward less risky borrowers, though subprime remains meaningfully elevated relative to a year ago. Long-term loan share and negative equity levels are ongoing watchpoints, as writing longer-term loans to borrowers already carrying negative equity compounds duration and collateral risk in lender portfolios.

Bottom Line: The June 2026 Dealertrack Credit Availability Index closed at 104.6, its highest level since December 2015, marking a fifth straight monthly increase. The advance was driven primarily by a sharp recovery in approval rates coupled with a new all-time high in long-term loan share. Modest widening in yield spread and a continued pullback in subprime lending served as primary offsets to index growth. Extended loan terms at a new all-time high and elevated negative equity continue to present risk potential as the index improves.

View historical Dealertrack Credit Availability Index reports.

The Dealertrack Credit Availability Index tracks six factors that affect auto credit access: loan approval rates, subprime share, yield spreads, loan term length, negative equity and down payments. Reported monthly, the index indicates whether access to auto credit is improving or declining. This typically means that it is cheaper and easier for consumers to obtain a loan or more expensive and harder. The index is published around the tenth of each month.