Electric-vehicle sales in March rebounded notably from February, across both new and used models. The influence of high gas prices can’t be ignored in the numbers, but the year-over-year story provides better perspective. As expected, the used EV market continues to expand in a very positive way; the new EV market, however, continues to be challenged, with demand and product availability down notably from year-ago levels.

New and Used EV Sales – March

New EV Sales: EV sales in March totaled an estimated 82,629 units, down 24.7% year over year but up 20.2% month over month. EVs accounted for 5.9% of total new‑vehicle sales, up slightly from 5.8% in February. The month‑over‑month gain was notable and outpaced the broader industry increase of 17.8%. However, the year‑over‑year comparison provides important context: despite elevated gas prices, EV market share declined from 6.8% a year earlier.

Tesla remained the clear volume leader at 41,055 units, followed by Chevrolet, Hyundai, Toyota, and Cadillac. Although Tesla sales increased from February, its EV market share declined to 49.7% in March, down from a revised 56.3% in February. Most brands recorded month‑over‑month sales gains in March, following a challenging February.

Used EV Sales: Used EV sales totaled 42,924 units in March, up 27.7% year over year and 53.9% month over month, with used EV market share increasing to 2.5%. Tesla led used EV sales in March with 15,385 units sold, followed by Chevrolet, Ford, Hyundai, and BMW.

Among higher‑volume brands, several recorded month‑over‑month increases of more than 50%, including Chevrolet), Ford, Hyundai, and Volkswagen, thanks in part of increasing availability of used models.

New and Used EV Days’ Supply – March

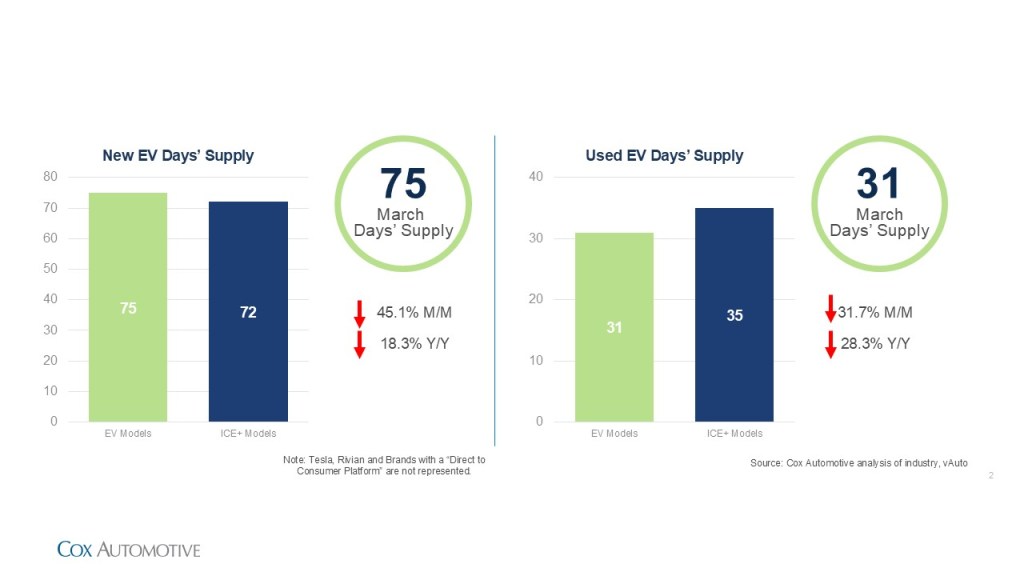

New EV Days’ Supply: New EV days’ supply fell to 75 days in March, down 45.1% month over month and 18.3% below year‑earlier levels. Days’ supply in March was at the lowest point since October, a time when the shelves had been emptied by strong sales ahead government-backed sales incentives being canceled.

The gap between EV and ICE+ days’ supply narrowed to 3 days in March, down from 168 days at the beginning of the year, as inventories tightened. Among brands, Volkswagen, Nissan, and Chevrolet carried the highest days’ supply, while Hyundai and Toyota remained the leanest. Ford recorded the largest month‑over‑month decline in days’ supply, falling 61%.

Used EV Days’ Supply: Used EV days’ supply declined to 31 days in March, down 31.7% month over month and 28.3% below year-earlier levels, falling 4 days below ICE+ levels after being 4 days above last month.

Supply tightened broadly among brands, with Kia, Chevrolet, and Volkswagen posting the largest declines among high-volume brands. Tesla remained the major brand with the lowest days’ supply at 30 days. Note: Tesla figures reflect only vehicles available through traditional dealerships, excluding vehicles at Tesla-owned outlets.

New and Used EV Prices – March

New EV ATP: The average transaction price (ATP) for a new EV in March was $54,508, down 6% year over year and 0.7% month over month. Incentives increased 3.1% month over month to an average of $7,967, representing 14.6% of ATP.

The month‑over‑month ATP decline reflected both per‑unit price pressure and mix shifts. With Tesla accounting for nearly 50% of total EV volume, its per‑unit price declines had an outsized impact on the market average, while rising volume from Chevrolet and Toyota added further downward pressure, given their lower‑than‑average ATPs. Cadillac and Ford were notable exceptions, each posting month‑over‑month ATP increases.

The EV price premium over ICE+ narrowed to roughly $5,800, marking another record low.

Used EV Listing Price: The average listing price for used EVs was $34,653 in March, down 6.1% year over year and lower by 0.4% month over month. Tesla listing prices increased 1.5% to $32,045, partially offsetting downward mix pressure from strong volume growth in lower‑priced brands such as Hyundai, Chevrolet, and Volkswagen. Among other high‑volume brands, Ford posted the largest month‑over‑month increase (+4.4%), while Cadillac and Audi recorded the steepest declines, falling 4.5% and 3.7%, respectively.

The used EV price premium over ICE+ vehicles narrowed to $1,012 in March, continuing a trend toward parity.

Looking Ahead

Elevated gas prices are certainly beginning to push more shoppers toward EV consideration, driving higher shopping activity on Kelley Blue Book and Autotrader, both Cox Automotive brands. History, however, suggests prices will need to remain elevated for an extended period — years, not weeks — before a meaningful shift in sales is reflected in the data. Further, EV consideration is also influenced by factors beyond gas prices, including charging infrastructure availability and higher price points.

New‑EV sales were healthy in March and marked a clear improvement from February, but volumes remain well below levels seen before the major shifts in government emissions and incentive policies.

Meanwhile, the used‑EV market continues to gain momentum as inventory availability improves and shoppers see more product variety across price points. With supply improving and applying downward pressure on pricing, used‑EV growth is expected to remain a bright spot through the remainder of the year.

View Historical EV Market Monitor reports.