The U.S. new-vehicle market may shift direction in March with consumer sentiment likely to fall due to uncertainty in the Middle East, in contrast with February which showed modest signs of recovery after a slow January. According to Cox Automotive’s vAuto Live Market View, the national sales pace improved month-over-month and remained relatively stable year over year on an adjusted basis.

2.85M

Total Inventory

as of Feb. 2026

92

Days’ Supply

$49,170

Average Listing Price

Total new-vehicle inventory in February was 2.85 million units, translating to 92 days of supply, with the average listing price at $49,170. February had two fewer selling days than January. Adjusting for this calendar difference, the sales pace increased by 2.4% month over month but decreased 1.6% year over year.

Inventory volume increased 4.1% month over month (from 2.74 million to 2.85 million units), a typical seasonal pattern as dealers build ahead of spring demand, but supply declined 4.4% year over year. Days’ supply dropped 2 days from the revised January measure of 94 and was lower by 3 days year over year, suggesting broad market balance.

Pricing remained measured. Average listing price increased 1.9% year over year but declined 0.9% compared to January, reflecting mix shifts and selective repositioning rather than broad discounting.

Behind the Aggregate: Where Demand Is and Where It Isn’t

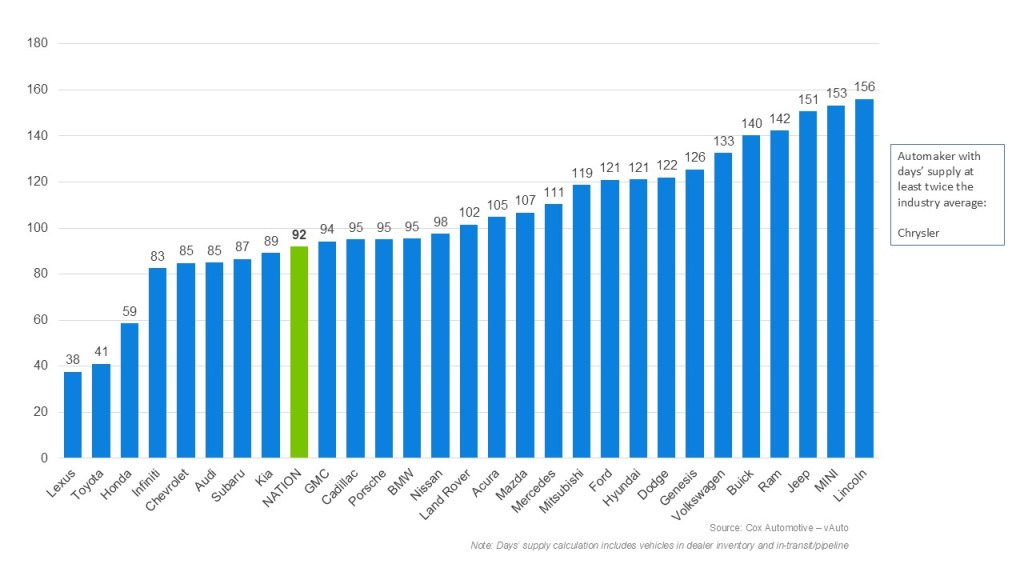

The February numbers indicate that demand varies widely by price band. Vehicles priced in the $35,000 to $45,000 range continue to outperform, carrying the leanest inventory at roughly 81 days of supply, indicating that real demand is running ahead of available stock. Toyota at 41 days and Honda at 59 days are especially tight, while Nissan at 98 days and Kia at 89 days also maintain controlled inventory. These brands retain pricing power, and dealers often want more stock, not less.

The opposite dynamic plays with vehicles in the $45,000 to $55,000 range, which has become the industry’s stretch zone. Middle-income buyers returning to market after four to five years are likely surprised by the escalating price of a familiar vehicle, with monthly payments much higher than they remember from their last purchase. This mid-range band represents the weakest inventory efficiency at approximately 120 days of supply.

Brands with heavier mid-market exposure are struggling. Ford sits at roughly 121 days, while Jeep at 151 days clearly illustrates the inventory and demand mismatch. Jeep’s year-over-year deterioration is stark, with days’ supply growing from 123 to 151 days, an increase of 28 days. Month over month, the brand improved 14 days (from 165 days in January), but this tightening occurs within a substantially bloated year-over-year position. Such imbalances resolve through margin pressure first via carrying costs, then incentives. Jeep’s aggressive new product launches and selective price reductions suggest awareness of this dynamic.

February Days’ Supply of Inventory by Brand

Pricing and Incentives Remain Restrained

Average listing price increased 1.9% year over year, while average transaction price rose to $49,353 according to Kelley Blue Book data, up 3.4% year over year. Higher transaction prices suggest buyers are choosing more expensive versions of the available inventory.

Incentives increased modestly but remain contained at 6.9% of transaction price, up from January but nearly flat year over year. Softening sales have not forced widespread discounting. Instead, manufacturers and dealers respond selectively, using incentives to address specific inventory pockets rather than the market broadly.

The Deeper Lesson: Alignment Is Everything

February reflects a bifurcated market weighed down by mismatched supply and demand. National metrics remain stable, inventory is leaner year over year, and pricing discipline is intact. But beneath the surface, the mainstream market struggles against inventory imbalances it has yet to fully resolve.

Vehicles in the $35,000 to $45,000 tier absorb demand and maintain leverage, while the mid-market tier carries excess supply and faces margin risk. For dealers, February’s lesson is less about volume and more about alignment. Where inventory matches real demand, the market functions well. Where it does not, adjustment is underway and will likely accelerate as spring demand either materializes or fails to arrive.