The U.S. new‑vehicle market entered April with a cleaner inventory position, thanks mostly to an improved sales pace in March helping lower elevated days’ supply. Total industry inventory stood at 2.89 million units in March, up from 2.85 million units in February, representing a month‑over‑month increase of 1.3%.

2.89M

Total Inventory

as of Mar. 2026

79

Days’ Supply

$48,667

Average Listing Price

Compared to last year, inventory volume in March was higher by 6.1%. The higher relative inventory this year is likely skewed some, since March 2025 saw significant pull‑ahead purchases following auto tariff announcements, driving inventory artificially lower a year ago.

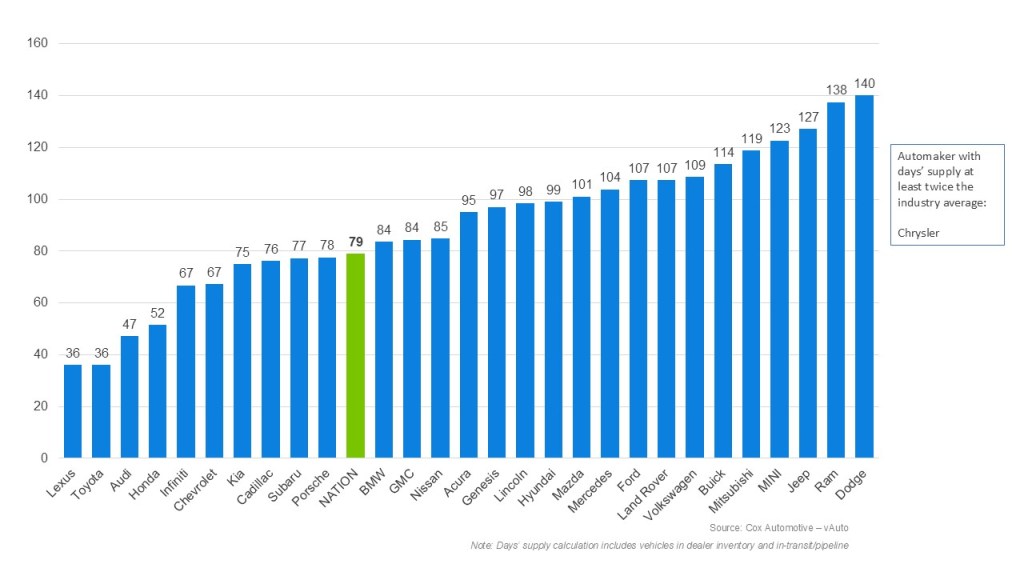

The March sales pace improved notably compared to January and February, with implied industry sales rising roughly 36% month over month. Days’ supply tightened sharply in March, falling to 79 days from an upwardly revised 96 in February, a 17.7% month‑over‑month decline. (Days’ supply in January: 94).

The sales pace last month, however, was down 4.8% from a strong result in March 2025. Year over year, days’ supply in March was 11.4% higher, again reflecting slower sales relative to last year’s tariff-driven sales frenzy.

Following a lackluster January and February, which were challenged by tough winter weather, the March sales uptick helped improve the broader inventory picture, notably lowering the industry-wide days’ supply and helping keep inventory levels mostly in check.

Industry View: Tight Inventory Among Less Expensive Vehicles

The strong March result was seasonally normal, and the improved sales pace helped nearly every brand reduce days’ supply measures. The interesting note about inventory is with the relative tightness of inventory of vehicles listed for under $40,000, and that there is no one model skewing those numbers. Rather, over the last year, the market has seen several models either discontinued or on a sell-down given model year 2026 redesigns. Additionally, this segment of more-affordable vehicles was noted from the tariff announcements to be most impacted by the new policies, as many are typically assembled outside of the U.S. Automakers are likely being very strategic in supply management.

March Days’ Supply of Inventory by Brand

Pricing and Incentives: Stability Masks Selective Pressure

While average listing prices for new vehicles remain essentially flat month over month at $48,667, this stability is increasingly driven by inventory mix. Dealers are able to protect margins where inventory allows, but the firmness in listing prices is largely supported by the limited supply of affordable vehicles under $40,000, while inventory growth is concentrated mostly in vehicles above $40,000. This dynamic restricts dealers from significantly raising asking prices without risking slower sales.

Meanwhile, according to Kelley Blue Book, the average new‑vehicle transaction price stood at $49,275 in March, up 3.4% year over year, and the average MSRP reached $51,456, a 3.9% increase versus last year. Both ATP and MSRP remain elevated, but these higher figures are more reflective of a continued skew toward trucks, mid-size SUVs and fewer entry-level options, rather than a true resurgence in pricing power or consumers absorbing higher prices. Automakers beginning to pass along tariff costs should not be underestimated either.

Incentives confirm that dynamic. In March 2026, average industry incentive spending rose to $3,541 per vehicle, equivalent to 7.2% of ATP, up from $3,388, or 6.9% of ATP, in the prior month. On a month‑over‑month basis, incentives increased both in dollar terms (+$153 per unit) and as a share of transaction prices (+0.3 percentage points), signaling that automakers are leaning more on targeted discounting to support volume.

The Bottom Line: Balance Achieved, Vulnerability Remains

March’s inventory picture reflects gradual progress rather than a decisive upswing. Days’ supply has dropped from January and February, yet demand is not robust enough to drive consistent gains in sales volume. March sales were healthy, but one month is not a trend.

The market remains discerning. Affordable, competitively priced models continue to sell quickly, but mismatched inventory still needs additional support. Success in the second quarter will depend less on total volume and more on offering the right vehicles for the specific buyers who are actively in the market.