Cox Automotive’s Auto Market Report video delivers a comprehensive analysis of the current automotive market. Chief Economist Jonathan Smoke leads our effort to translate data and trends into actionable insights. This video covers a wide range of topics, including consumer spending patterns, consumer sentiment, retail vehicle sales, financing rates, supply dynamics, pricing trends and leading indicators from Cox Automotive’s extensive data ecosystem.

Download this week’s presentation

Report Summary – May 27, 2025

Key Highlights:

- Consumer sentiment is rebounding in May, signaling renewed optimism despite economic headwinds.

- Retail vehicle sales remain stronger than last year, even as May shows signs of softening.

- Used vehicle prices are trending downward again, offering potential opportunities for buyers.

Consumer Confidence Rebounds Amid Spending Surge

After months of decline, the Index of Consumer Sentiment is showing signs of life, rising 6.1% so far in May. This uptick follows a robust April in which total consumer spending posted its strongest year-over-year growth since early January.

- Weekly spending data from Bloomberg indicates a clear acceleration in April.

- Despite higher continuing jobless claims—now at 1.90 million—consumers appear more willing to spend.

- The correlation between sentiment and gas prices remains strong, with recent declines in fuel costs likely contributing to improved outlooks.

Retail Sales Stay Strong, But Momentum Slows

Retail vehicle sales – both new and used – have softened in May but continue to outperform last year’s levels, reflecting resilient demand in a constrained market.

- New and used sales volumes are still ahead of 2024, despite a month-over-month dip.

- Dealer incentives have tightened, especially on low-interest financing, as OEMs adjust to tariff pressures.

- The share of loans with APRs below 3% has declined significantly in 2025.

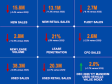

Financing Conditions Shift as Rates Rise

While average loan rates for used vehicles held steady at 14.16% in May, new vehicle rates edged higher to 9.62%, reflecting broader interest rate trends.

- The Federal Reserve’s policy stance and 10-year Treasury yields continue to influence auto loan rates.

- March and April saw modest declines in average rates, but May reversed that trend for new vehicles.

- Consumers face a more expensive borrowing environment, especially for new purchases.

Inventory Levels Improve, But Remain Tight

Supply levels for both new and used vehicles have increased in recent weeks, though they remain below historical norms.

- New vehicle days’ supply has risen modestly but is still constrained relative to pre-pandemic levels.

- Used vehicle inventory has also improved, offering more options for buyers.

- Weekly fluctuations suggest a fragile balance between supply and demand.

Used Vehicle Prices Resume Downward Trend

After a brief plateau, used vehicle prices are once again declining – a welcome development for budget-conscious shoppers.

- Retail prices for 3-year-old models dipped 0.1% last week, while wholesale prices fell 0.8%.

- The Manheim Index shows a consistent downward trajectory for both retail and wholesale segments.

- This trend may continue if supply levels remain stable and demand softens.

Cox Automotive Leading Indicators

- Dealer leads are up year over year so far in May on Autotrader but are down on Kelley Blue Book, and leads are up for the month compared to April on Autotrader but down on Kelley Blue Book.

- Unique leads per dealer for new vehicles are down year over year but up on used vehicles so far in May on websites hosted by Dealer.com, and new and used leads are down for the month compared to April.

- Unique credit applications per dealer on Dealertrack were up 2% year over year last week, with the trend in applications per dealer declining week over week in new and used.

- Service trends on Xtime relative to last year improved in the week ending May 17, as completed appointments were down 1.5% year over year.