It’s been four months since President Trump announced his administration’s new tariff plans for the auto market, and the impacts are already being felt far and wide. As we’ve noted, the automotive industry is highly globalized, with nearly half of the vehicles sold in the U.S. manufactured outside of the U.S.

The most challenging aspect of this tariff cycle has been the constant, on-again-off-again nature of the policies. Just last Thursday, the U.S. delayed, by 90 days, higher tariffs on Mexico, our largest trading partner. And tariff negotiations are ongoing with Canada and China, a major automobile manufacturing hub and major parts supplier, respectively.

We’re watching a reshaping of the auto market – one where cost pressures and policy pivots are rewriting the playbook for manufacturers, dealers and consumers alike.

With an Aug. 1 deadline in the rearview mirror, here’s a snapshot of where things stand now for the automotive industry.

What’s New on the Tariff Front?

Since April, when initial tariffs for imported automobiles were set at 25%, the import tax has been lowered for many source countries. Vehicles from the U.K. are now subject to a 10% tariff, and, in the past few weeks, 15% automobile import tariffs were established with several other major trading partners, including Japan, South Korea and the EU. This level of tariffs is obviously better than the previous level of 25% (which still applies to vehicles built in Canada and Mexico, minus USMCA content). Still, it is far higher than the rates of nearly 0% or 2.5% in 2024. As noted, negotiations with Canada are ongoing at the time this is being drafted, and discussions with Mexico and China have been extended.

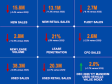

To provide a perspective on the costs of tariffs on the U.S. auto industry, Cox Automotive estimates indicate that, based on volumes and average listing prices of imported vehicles through the first seven months of 2025, automakers have theoretically racked up more than $25 billion in tariff obligations so far (if tariffs were in place from Jan. 1). This is equal to the average imported vehicle being charged roughly $5,200 at the U.S. border. Land Rovers are obviously paying more; Chevrolets from South Korea are paying less. But in this scenario, Toyota, General Motors and Hyundai Motor Group would have paid the most so far in 2025. When spread across all vehicles sold year to date, that $25 billion is roughly equal to an additional $2,500 per vehicle in added cost for the industry.

Even vehicles assembled in the U.S. are feeling the squeeze, with tariffs on steel, aluminum, copper, parts and battery materials driving up costs for automakers and auto dealers. Tariffs are inflationary, adding significantly to the cost of producing and selling automobiles.

Are Automakers Feeling It?

Most certainly. Second-quarter earnings reports from several automakers in the past few weeks clearly show the impact of tariffs. Many cited tariffs as a direct hit to profitability. General Motors reported that it had absorbed $1.1 billion in tariff costs last quarter but prioritized maintaining imports to support customers and dealers. In all, the company is bracing for a $4-to-$5 billion impact in 2025. Ford cited tariff costs of roughly $800 million in Q2 and is expecting a total impact this year of nearly $3 billion. Similar narratives were told by Toyota, Nissan, Hyundai and many of the European automakers.

According to general estimates from Cox Automotive, the total bill so far in 2025 for vehicles imported from Korea would be $3.8 billion, or roughly $4,000 per unit (if tariffs were in place since Jan. 1). From the EU, tariff costs thus in 2025 would have been $4.6 billion, or $8,500 per unit imported. More than 1.8 million new vehicles have been imported into the U.S. from Mexico so far this year. The added cost to the auto industry is in the neighborhood of $8.6 billion, or roughly $4,800 per vehicle, entirely flipping the build-in-Mexico business model. In the auto industry, the red ink flows fast.

Declining margins and lower profitability will be common themes for automakers and dealers alike through the remainder of 2025, as higher tariffs – higher costs – on imported automobiles appear to be the new norm for the industry. These higher costs will eventually trickle through the economy over time.

What About Vehicle Prices for Consumers?

So far, consumers have been shielded from higher prices. Average transaction prices (ATP) are mostly flat or slightly down year over year, even as manufacturer’s suggested retail prices (MSRPs) continue to rise. We believe MSRPs are more closely related to the cost of producing a vehicle, and our estimates show that MSRPs were up 2.3% year over year in June, marking the third consecutive month of higher MSRPs. This increase is lower than long-term averages, but after nearly two years of steady new-vehicle prices, the trajectory is clearly on the rise now.

ATPs, on the other hand, were higher by only 1.2% in June, suggesting consumers are not yet feeling the full force of higher costs. Instead, automakers and dealers are containing the higher costs created by tariffs while watching profitability decline. Popular compact SUVs are being hardest hit by tariff policy, as many are imported. With tariffs in place, automaker costs increase by an average of $2,800 per imported unit. Subcompact SUVs are hit hard as well: The average tariff bill is nearly $3,000. Consumers, however, are not yet seeing this level of increase at retail.

But that won’t last. The Cox Automotive team still expects consumers to see retail prices climb by 4–8% by year-end, with price increases accelerating as 2026 model-year vehicles hit the market. An update on July prices from Cox Automotive will be available next week.

Have New-Vehicle Sales Suffered Because of the Tariffs?

Not much is the simple answer. As the administration’s aggressive tariff policy came to light in early spring, the new-vehicle sales pace surged in March and April and then cooled in May and June. Through the first half of 2025, total new-vehicle sales were higher year over year by nearly 3%.

In July, consumers seemingly got “uncertainty” fatigue, and the sales pace increased again, as the wealth effect of a strong equities market in Q2 and pent-up demand likely helped push the sales pace to 16.4 million, the highest seasonally adjusted annual rate (SAAR) for July since 2019. Overall, new-vehicle sales have held up remarkably well despite obvious challenges faced by the industry.

New-vehicle inventory volume saw a dip in April and May, as the initial sales surge drew supply down to roughly 2.47 million units at dealerships across the U.S. By the start of July, inventory volume was close to where it began in 2025, at 2.83 million units and slightly below year-earlier levels.

Importantly, inventory measures in late June showed that MY2026 vehicles had only begun to appear on dealer lots, but that mix is expected to increase notably in the coming months. With new-model-year vehicles arriving, higher prices are expected as increases are easy to manage with a model-year change.

Is There More to This Story?

Yes, this story continues to unfold. While tariffs are adding cost that automakers have to bear, there is other good news. The One Big Beautiful Bill Act certainly has some sugar for the automakers that will help ease the bitterness of higher tariffs. And new policies by the Trump administration are reducing other costs, particularly for the domestic automakers that specialize in larger, less-fuel-efficient vehicles. It is clear now that the administration is easing environmental regulations, as proposals are in place to roll back emissions penalties, EPA fines, and greenhouse gas standards created to incentivize fuel efficiency.

Ford CEO Jim Farley recently noted that these changes could provide a financial tailwind to help offset the headwinds from tariffs.

Importantly, the Trump administration has also committed to dialing back federal EV incentives. The government-backed tax incentives of up to $7,500 for qualified new EV sales will be mothballed on October 1, and the popular “leasing loophole,” which greatly expanded the pool of qualified sales, is also dead. Money allocated to support important infrastructure improvements for EVs has also been curtailed. With these changes, Cox Automotive is expecting an EV sales surge through Q3 and a significant decline in Q4.

How’s the Second Half of 2025 Looking for the Auto Industry?

The auto industry is clearly under pressure. Tariffs are increasing costs across the board for automakers, dealers and consumers—not only for new vehicles, but for aftermarket parts and insurance costs. As Cox Automotive has noted, tariffs on automobiles and automobile parts contribute to inflation and pose a challenge for an industry already facing stagnant growth, partly due to affordability issues.

Even the rollback of emissions standards may have unintended consequences, encouraging automakers to prioritize larger, higher-margin vehicles over affordable, efficient models. And as a result, prices rise. The Cox Automotive Economic and Industry Insights team expects higher prices to put downward pressure on new-vehicle sales in the second half of 2025. We expect the average price of a new vehicle in the U.S. to break the $50,000 barrier in 2025, as automakers begin to pass along the costs of tariffs and the market sells a larger share of higher-end vehicles. Our forecast for new-vehicle sales remains below 16 million units for the year, a decline compared to 2024, as higher prices continue to move the auto market in a direction that favors high-net-worth households with excellent credit, leaving many on the outside looking in.