Job growth in November did not slow as much as expected or as desired by the Fed. The unemployment rate was steady at 3.7%, and wage growth accelerated. Jobless claims increased throughout November. Continuing claims have risen from historic lows but are at the highest levels in 38 weeks.

Consumer spending growth accelerated in November as personal income growth also accelerated. The Fed’s favorite measure of inflation showed inflation cooling but still high.

The light new-vehicle sales seasonally adjusted annual rate (SAAR) declined in November to 14.1 million. New-vehicle prices increased. The average manufacturer’s suggested retail price (MSRP) is now growing faster than the prices paid, but the average price paid is still higher than the average MSRP.

Job Growth Doesn’t Slow Enough for Fed

Job growth in November did not slow as much as expected or desired by the Fed. November saw 263,000 jobs created when only 200,000 had been expected. The last two monthly numbers were revised for a net decline of 23,000 fewer jobs than originally estimated, even though job creation in October was revised up to 284,000.

Most of the November gains were in the service sector, with Leisure and Hospitality and Education and Health Services delivering 173,000 jobs collectively. Retail Trade shed 29,900 jobs. Auto dealers added 6,900 jobs, leaving employment down 69,000 or 5.3% below the February 2020 level. Total payrolls now exceed February 2020 payrolls by 1 million.

Unemployment Rate Unchanged, Underemployment Hits 53-Year Low

The headline unemployment rate was unchanged at 3.7% in November. The labor force participation rate declined to 62.1% from 62.2% in October. Participation is down 1.3 percentage points from February 2020 and represents 3.4 million fewer people in the labor force compared to February 2020.

The underemployment rate, the broadest measure of unemployment, declined to 6.7% from 6.8% in October and back to a 53-year low. Monthly average hourly earnings growth accelerated to 0.6% from an upwardly revised 0.5% in October. Earnings growth y/y accelerated to 5.1%.

Jobless claims increased in November. Continuing claims have risen from historic lows but are at the highest levels in 38 weeks.

Consumer Spending and Personal Income Growth Accelerates

Consumer spending growth accelerated in October with nominal growth of 0.8% following an increase of 0.6% in September. Personal income growth also accelerated to 0.7% from 0.4%.

Employee compensation growth decelerated to 0.5% from 0.6%. Government transfer payments increased by 1.6%, driven by increases in unemployment benefits. Proprietors’ income slowed to show no growth from September.

Spending on durable goods increased by 2.1% in October, spending on nondurable goods increased by 1.1%, and spending on services increased by 0.5%. Spending on motor vehicles and parts increased by 2.1% following a 0.5% increase in September.

The personal savings rate declined to 2.3%, the lowest level since July 2005.

The Personal Consumption Expenditure (PCE) Index, the key gauge of inflation that the Fed follows, increased 0.3% in October and was unchanged from September. Overall price inflation, according to the PCE was down to 6.0% in October from a year ago, while the core inflation rate declined to 5.0% from 5.2% in September. Factoring in inflation, real spending increased by 0.5% in October, up from 0.3% in September.

New-Vehicle Sales Rise

November total new-light-vehicle sales were up 10.4% year over year. By volume, November new-vehicle sales were down 4.2% from October. The November SAAR was 14.1 million, which was a 7.9% increase from last year’s 13.1 million but down 6.5% from October’s upwardly revised 15.1 million. Through November, the SAAR year to date is 13.8 million, which is down 8% from 2021’s 14.9 million.

Combined sales into large rental, commercial, and government fleets were up 55% in November from a year ago. Sales into rental fleets were up 127% year to year, while sales into commercial fleets were up 29% and sales into government fleets were up 15%.

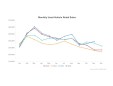

Average Transaction Price Continues to Exceed MSRP

The average transaction price of a new vehicle in November exceeded the average MSRP for the 17th month in a row, and the average price at $48,681 increased by 0.9% and was up 4.4% from a year ago. Check back in the Newsroom on Monday, December 12, for a full report from Kelley Blue Book.

The gap between the price paid and MSRP is closing, as the average MSRP increased 1.2% in November from October and was up 5.4% from a year ago.

The average incentive spending from manufacturers increased by 2.7% to $1,066 in November. Still, incentives as a percentage of average transaction price were unchanged at 2.2% and remained just barely higher than the 2.1% recorded in September, which had been a 20-year low. Pricing power is still strong but starting to decline as new-vehicle inventory grows.

Join us for the 2023 Cox Automotive Industry Insights and Forecast Call hosted by Chief Economist Jonathan Smoke and the Industry Insights team on Thursday, January 12, at 11 a.m. EST. During this 90-minute session, you will hear how the auto industry performed in 2022 and how the Cox Automotive team sees the industry progressing in the new year.

Jonathan Smoke is the chief economist at Cox Automotive.