Key Highlights

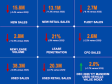

- September’s job growth significantly surpassed expectations, with 254,000 jobs created compared to an expected 150,000, marking the highest surge since March.

- Despite the robust job creation, the automotive industry exhibited slower growth, with auto dealers adding only 1,300 jobs, leaving overall dealership employment 0.7% lower than February 2020 levels.

- September also saw new light-vehicle sales drop by 12.8% year over year, recovering slightly to a seasonally adjusted annual rate (SAAR) of 15.8 million, up from the previous year’s 15.7 million figure and August’s 15.3 million.

Job Growth Surges in September

September registered a stronger-than-expected uptick in job growth, with a total of 254,000 jobs created, outpacing the anticipated 150,000.

- The private sector contributed the lion’s share, adding 223,000 jobs, marking the highest growth since March.

- The manufacturing sector lost 7,000 jobs, following a decline of 27,000 in August.

- The automotive sector saw a modest rise, with 1,300 jobs added at auto dealerships. However, dealership employment remains down by 8,800 (or 0.7%) compared to February 2020.

Unemployment Rate and Labor Market Evolution

While the headline unemployment rate saw a slight decline, overall market indicators and the deterioration in the labor market suggest a potential recession on the horizon as per the Sahm rule.

- The unemployment rate declined slightly to 4.1% from 4.2% yet increased by 0.5 percentage points year over year.

- The labor force participation rate remained steady at 62.7% but is still down by 0.6 percentage points since the pre-pandemic period. Despite adding 6.8 million jobs, there are 1.6 million fewer people in the labor force.

- The underemployment rate, a significant measure of unemployment, declined to 7.7%, slightly higher than the February 2020 mark.

New-Vehicle Sales Experience a Dip

Despite a slight recovery in the SAAR, new light-vehicle sales in September witnessed a 12.8% year-over-year decline, with new vehicle sales volume down by 17.9% month over month. A key driver of the volume decline was fewer selling days.

- The September SAAR recovered to 15.8 million, marking a 0.5% rise from last year and a 3.3% increase from August’s revised 15.3 million.

- Fleet sales saw a 6.4% year-over-year decrease in August, with large rental fleet sales experiencing a 1.5% rise, but commercial and government fleet sales down 11.7% and 12.3%, respectively.

- Estimated retail sales were down 12.2% from last year, leading to an estimated retail SAAR of 12.4 million, a decrease from both last year’s 13.3 million and last month’s 12.7 million pace.