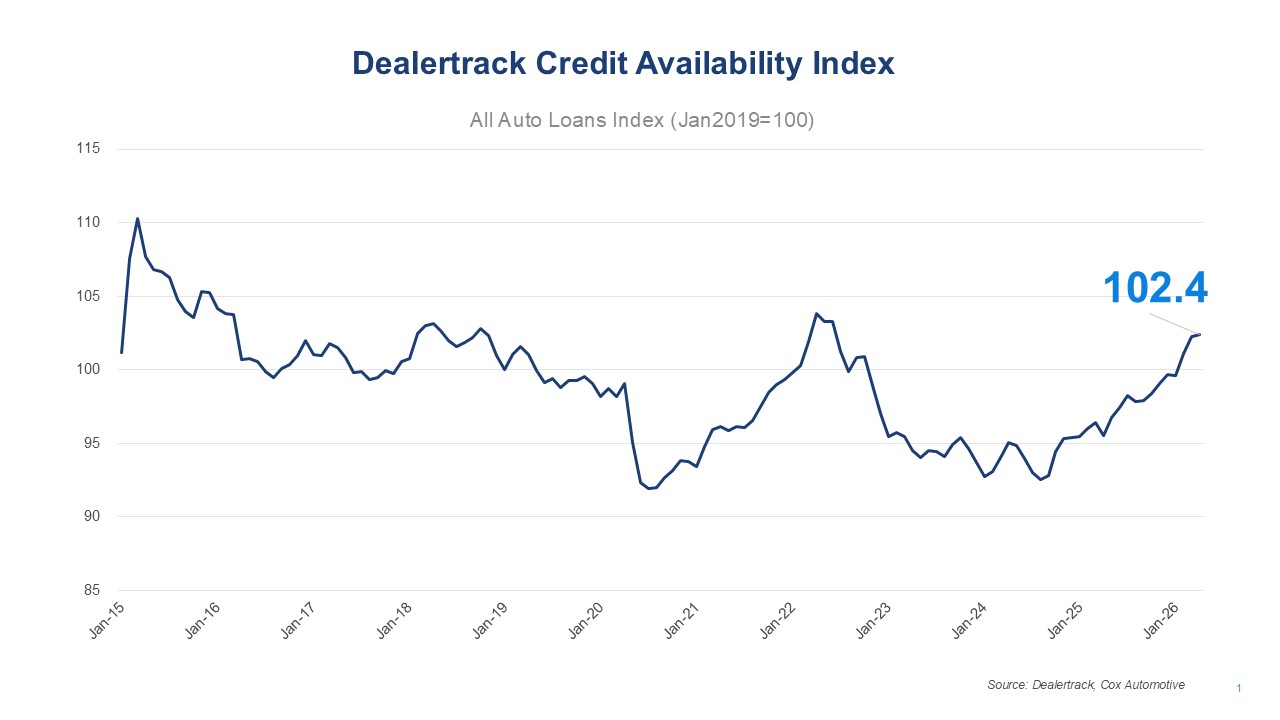

In April 2026, the Dealertrack Credit Availability Index rose to 102.4, its highest level since June 2022, though essentially unchanged from March’s revised-lower 102.3. The All-Loans Index increased just 0.1% from March and is up approximately 7.2% from April 2025. April’s modest gain masked a more complex picture beneath, as gains in some key metrics offset losses in others.

Key Metrics

- Approval Rates: The approval rate for auto loans rose to 71.0% in April, up 60 basis points (bps) from March’s revised-lower 70.4%. Approval rates remain down 120 bps from April 2025, continuing a trend of year-over-year tightening of loan approvals even as month-over-month conditions improved.

- Subprime Share: The share of loans to subprime borrowers fell sharply, declining 210 bps month over month, from 19.5% in March to 17.4% in April. The April pullback follows March’s surge to its highest reading since March 2020. Despite the decline, subprime share remains elevated, up 370 bps year over year.

- Yield Spread: The yield spread narrowed by 59 bps (from 7.84 to 7.25) in April, a direct reversal from March’s 31 bps widening. The average contract rate declined 50 bps to 11.2%, while the 5-year Treasury yield rose 9 bps to 3.94%. The narrowing spread reflects more favorable borrowing conditions for consumers in April.

- Loan Term Length: The share of loans with terms greater than 72 months increased 90 bps month over month, increasing from 28.8% to 29.7% and setting a new all-time high in the dataset and surpassing the previous record of 29.3% set in February 2026. The measure is up approximately 470 bps year over year. The continued extension of loan terms reflects persistent affordability pressures. Even as loan rates dipped modestly in April, consumers continue to stretch repayment horizons to manage monthly payment burdens, extending the period of financial exposure.

- Negative Equity Share: The share of borrowers with negative equity declined 70 bps month over month to 58.5%, ending a three-month-streak of record highs. Despite this modest improvement, the share of loans with negative equity increased approximately 540 bps year over year, up from 53.1% in April 2025. The elevated level signals that a substantial share of borrowers continue to carry loan balances that exceed their vehicle’s value, a persistent source of risk for both borrowers and lenders.

- Down Payment Percentage: The average down payment percentage decreased 50 bps, declining from 13.9% to 13.4%, and is down approximately 130 bps year over year from around 14.7% in April 2025. The decline follows March’s modest uptick.

Channel and Lender Trends

- Channels: Credit access showed a mixed picture by channel in April. The largest month-over-month gains were in the Independent Used and Non-Captive New segments, followed by modest improvement in All New and Used CPO. All Used and Franchise Used saw slight month-over-month declines. Despite the monthly variation, all channels remain meaningfully above year-ago levels.

- Lender Types: Lender performance was mixed in April. Banks led the market with credit availability rising 1.6%, the strongest monthly gain among lender types for the second consecutive month. Finance Companies also improved, up 0.8%. Captives edged lower, declining 0.4%, while Credit Unions pulled back 0.9% after recovering in March.

Year-Over-Year Comparison

- Channels: The most notable year-over-year improvements were in All New and Non-Captive New, indicating continued strength in the new vehicle segment. Franchise Used and Independent Used also posted solid gains, while All Used improved broadly. CPO saw a more modest year-over-year improvement.

- Lender Types: Captives and Banks led year-over-year improvement, while Finance Companies also posted solid gains. Credit Unions saw a more modest year-over-year improvement.

Implications for Consumers and Lenders

- Consumers: April brought a more favorable pricing environment compared to March, with the yield spread narrowing nearly 60 bps and the average contract rate falling 50 bps. For consumers who financed in April, this represented a tangible improvement in borrowing cost. However, the broader picture carries important cautions. Loan terms reached a new all-time high of 29.7% with terms greater than 72 months, meaning more consumers are extending repayment to 6 or more years to manage monthly payments. Combined with negative equity that remains nearly 540 bps above year-ago levels, consumers face compounding financial risk that can be difficult to unwind, and should carefully consider the full terms of any financing offer, particularly total loan length and overall cost.

- Lenders: Banks again led credit expansion in April, posting the strongest monthly gain for the second consecutive month and continuing to extend their year-over-year lead. Finance Companies also improved. The pullback in Captive and Credit Union credit access is notable and may reflect portfolio management decisions in an environment where structural risk indicators remain elevated. The sharp retreat in subprime lending in April is a positive development from a risk management standpoint; however, the subprime share remains 370 bps above year-ago levels, and the new all-time high in loans exceeding 72-month terms signals that portfolio risk remains a key watchpoint. Balancing volume growth with disciplined underwriting will continue to be important as these longer-term indicators build.

The April 2026 Dealertrack Credit Availability Index closed at 102.4, its highest level since June 2022. The month’s most significant movement was a sharp pullback in subprime lending, which was the largest drag on the index. Narrowing yield spreads, longer loan terms, and a recovery in approval rates collectively offset that pressure. However, longer loan terms reached a new all-time high in doing so, and negative equity remains deeply elevated year over year despite a slight easing from March’s record, both signals that affordability challenges and balance sheet risk across the auto finance market persist.

View historical Dealertrack Credit Availability Index reports.

The Dealertrack Credit Availability Index tracks six factors that affect auto credit access: loan approval rates, subprime share, yield spreads, loan term length, negative equity and down payments. Reported monthly, the index indicates whether access to auto credit is improving or declining. This typically means that it is cheaper and easier for consumers to obtain a loan or more expensive and harder. The index is published around the tenth of each month.