Updated, July 2, 2026: Despite persistent economic headwinds, the U.S. new-vehicle market delivered a stronger-than-expected result in June. According to preliminary estimates, June sales likely reached 1.36 million units, up 7.2% year over year. The seasonally adjusted annual rate (SAAR) of new-vehicle sales in June likely finished near 16.5 million, above the Cox Automotive forecast of 16.1 million. Revised government data released in early July also showed a stronger sales pace earlier this spring, with March and April SAARs both revised higher.

The June performance was fueled in part by stronger fleet activity, particularly among domestic manufacturers, while retail demand remained resilient despite elevated interest rates, weak housing activity, and subdued consumer confidence. Notably, economic conditions that would typically slow vehicle sales had little apparent impact on June results.

As Cox Automotive Chief Economist Jeremy Robb noted during the Cox Automotive Mid-Year Review, “Even with all the economic noise, automotive demand has remained resilient.”

At this point, vehicle demand appears to be coming from household wealth rather than consumer sentiment. The economy continues to send mixed signals, but record equity markets are helping offset many of the pressures that would normally weigh on vehicle demand. As long as household wealth continues to grow, the new-vehicle market may prove more resilient than many traditional economic indicators would suggest.

With the first half now complete, the sales pace is running stronger than many expected, even as broader economic challenges remain in place. For a full recap of first half market performance, watch the Cox Automotive 2026 Mid-Year Review.

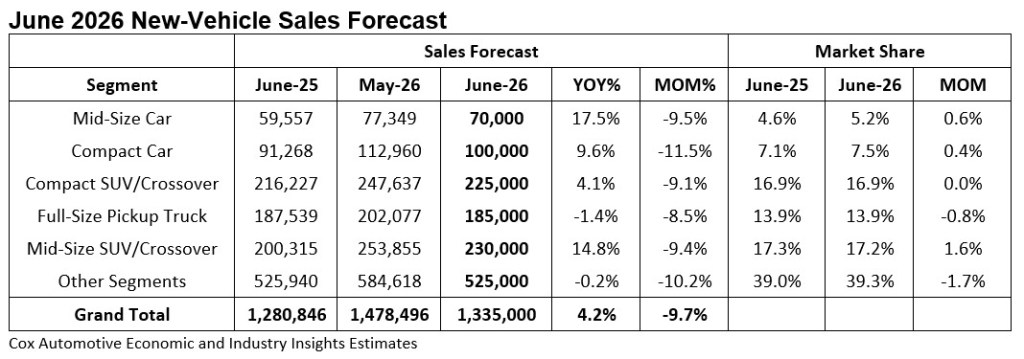

ATLANTA, June 24, 2026 – The June SAAR is expected to finish near 16.1 million, roughly in line with March, April and May—an unusual period of consistency given recent volatility and high energy prices. June sales volume, forecast at 1.34 million units, will show a gain compared to June 2025, but a decline from May. June has 25 selling days, one more than last year and one less than last month.

With healthy June sales, second-quarter volume is forecast to finish above the weather-impacted first quarter. Even so, total new-vehicle sales in the first half of 2026 are tracking 3.6% lower year over year.

Despite continued economic and policy uncertainty, the new-vehicle market has proven to be relatively resilient in 2026. Recent geopolitical tension and higher gas prices have had a limited impact on demand, with shoppers largely holding steady. After a volatile stretch earlier in the year driven by weather and policy shifts, the monthly sales pace has largely stabilized.

Affordability remains a central constraint, increasingly shaped by broader household finances rather than vehicle prices alone. Elevated interest rates, higher costs for essentials, and tighter budgets are limiting purchasing power across income levels. Even so, strong equity markets and accumulated household wealth are helping support demand. Assuming no major policy shocks, the new-vehicle market in 2026 is expected to continue fluctuating in the high-15 to low-16 million range. The Cox Automotive full year forecast remains unchanged at 15.8 million, a decline of 2.9% from 2025.

“Although there is a tremendous amount of economic and policy uncertainty these days, the new-vehicle market seems to be relatively unfazed. Thus far, vehicle buyers have shrugged off the latest shock – the Iran War and higher gas prices – as new-vehicle sales have been fairly stable the last few months,” said Cox Automotive Senior Economist Charlie Chesbrough.

First-Half Sales Lower Compared to 2025

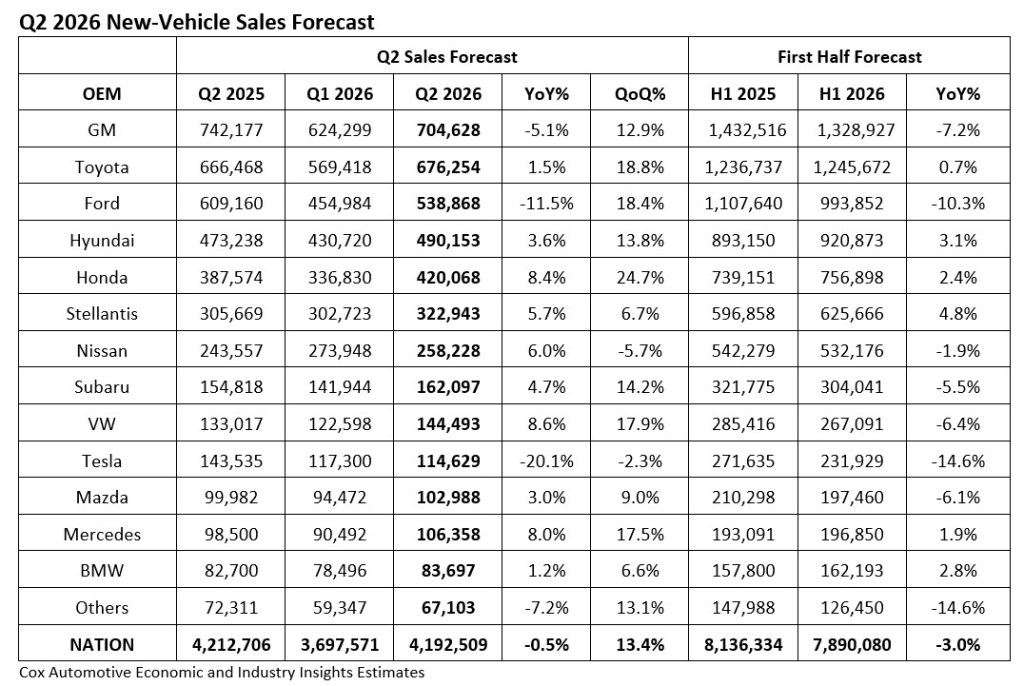

General Motors remains the volume leader through the first half of 2026, but its top spot is under pressure. The automaker is expected to finish the second quarter with just under 705,000 vehicles sold, down 5.1% year over year; first-half sales are tracking 7.2% lower. All GM brands are posting declines, led by Buick and Cadillac, each down more than 20% for the first half, resulting in a modest loss of market share.

Toyota momentum continues, and the company is emerging as a challenger for the top spot. Second-quarter sales are expected to rise 18.8% from the first quarter—well ahead of the broader market—fueled by strong demand for redesigned products and broad hybrid offerings. This growth is helping Toyota expand, narrowing the gap with GM to less than 100,000 units and setting up a potential shift in leadership by year-end if trends hold.

Elsewhere, performance across automakers is mixed. Hyundai Motor Group continues to deliver steady gains, with first-half share increasing by 0.7 percentage points. Stellantis sales have also rebounded, with volume up 4.8% and market share improving after several years of decline. In contrast, Cox Automotive sales estimates suggest Ford is facing a challenging year, with first-half sales expected to fall 10.3%, while Tesla is also under pressure, with volumes down 14.6% amid intensifying competition and fewer products to sell.

Cox Automotive Full-Year Forecast Remains Mostly Unchanged

Cox Automotive’s outlook for the 2026 new-vehicle market remains largely consistent with expectations set at the start of the year, reflecting a fundamentally steady environment despite unfavorable economic headwinds. The full-year new-vehicle sales pace is forecast to be 15.8 million units, a 2.9% decline from 2025. However, that decline is more a function of last year’s stronger-than-expected performance, rather than a meaningful deterioration in demand in 2026. Retail sales are projected to reach 12.9 million units, slightly lower than the Q1 forecast update, while fleet sales are expected to total 2.9 million units, down modestly year over year but improved from Q1 estimate.

The broader economic backdrop continues to present mixed signals, but not enough to materially alter the sales outlook. Inflationary pressures tied to energy costs and ongoing affordability challenges have weighed on consumer sentiment. Even with elevated interest rates and cautious consumers, the new-vehicle market has remained resilient.

“While some of the year-over-year comparisons look softer, our overall outlook for the new-vehicle market in 2026 hasn’t changed in a meaningful way since January,” said Cox Automotive Chief Economist Jeremy Robb. “Last year’s stronger performance set a high benchmark, but demand remains resilient. As inflation pressures begin to ease and the Fed stays focused on supporting economic stability, we believe the industry is positioned to maintain a steady sales environment through the remainder of 2026.”

For a deep dive into first-half market performance, watch the Cox Automotive 2026 Mid-Year Review.

Media Contacts:

Mark Schirmer

734 883 6346

mark.schirmer@coxautoinc.com