The EV market showed further signs of stabilization in May, following softer conditions in April. While new EV sales improved sequentially, overall demand remains below year-ago levels. The annual decline of 21.9%, however, was the smallest since government support was removed. At the same time, the used EV market continues to expand, supported by improving supply and a growing wave of off-lease returns, reinforcing the used market’s increasing role in broadening consumer access and supporting overall EV adoption.

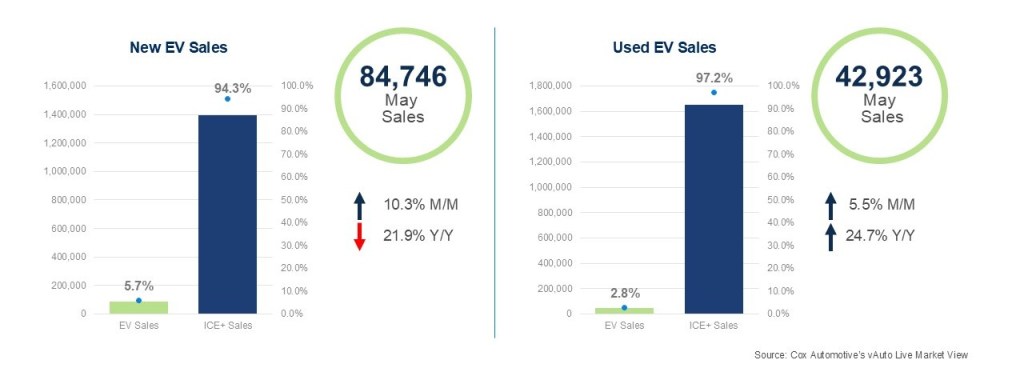

New and Used EV Sales – May

New EV Sales: New EV sales totaled an estimated 84,746 units in May, rising 10.3% from April but falling 21.9% from a year earlier. EVs accounted for 5.7% of total new-vehicle sales, indicating a sequential improvement from April but still a notably softer market than a year ago.

Tesla remained the volume leader with 40,578 units sold, followed by Hyundai, Cadillac, Toyota, and Chevrolet. Tesla’s share of the EV market eased to 47.9%, down from April, as several competitors posted stronger monthly gains. Among higher-volume brands, Hyundai, Cadillac, Toyota, and Subaru all gained ground in May, while declines at Chevrolet and Rivian limited the pace of the overall rebound. At the model level, the Tesla Model Y and Model 3 continued to dominate, while the Hyundai Ioniq 5, Ford Mustang Mach-E, and Toyota BZ led the next tier of volume.

Used EV Sales: Used EV sales reached 42,923 units in May, up 5.5% month over month and 24.7% year over year, with used EV market share holding at 2.8%. Tesla again led with 15,353 units sold through non-Tesla dealers, though volume declined slightly month over month, followed by sales of Hyundai, Chevrolet, Ford and BMW.

Following April’s more normalized pace, May reflected continued steady growth across the used EV market. Month-over-month gains were broad-based, with many brands proving popular, led by strong growth among Hyundai, BMW, Volkswagen, and Cadillac. The consistent year-over-year growth underscores continued expansion of the used EV business as off-lease returns and trade-ins build inventory depth across more brands and price points.

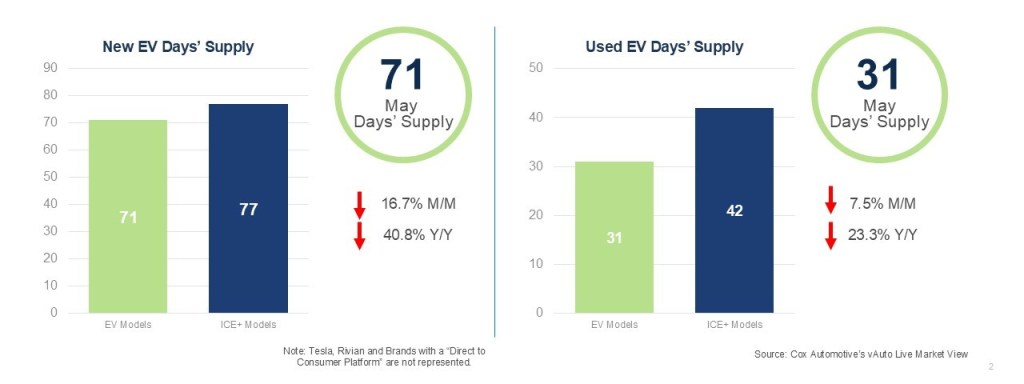

New and Used EV Days’ Supply – May

New EV Days’ Supply: Days’ supply edged lower to 71 in May, following a modest upward revision to April. Inventory remains more than 40% below year-earlier levels and has fallen below ICE+ days’ supply, highlighting continued tightening of new EV supply.

Inventory levels remain uneven across manufacturers, though trends among several higher-volume brands reinforce gradual normalization. Hyundai, Cadillac, Ford, and BMW all saw meaningful month-over-month declines in days’ supply, aligning with stronger sales volumes and careful inventory management.

Used EV Days’ Supply: Days’ supply fell to 31 in May, down 7.5% month over month and 23.3% below year-earlier levels. Used EV days’ supply remained well below ICE+ for a third consecutive month, representing the largest gap between the two segments since September 2025. The spread underscores continued tightening in the used EV market and faster inventory turnover relative to the broader used-vehicle segment.

Days’ supply tightened broadly among high-volume brands, led by Volkswagen and Honda. Tesla, Toyota, and Hyundai availability also remained relatively lean, reinforcing strong turnover across the used EV segment.

Note: Tesla and Rivian figures reflect only vehicles available through traditional dealerships and exclude vehicles at factory-owned outlets.

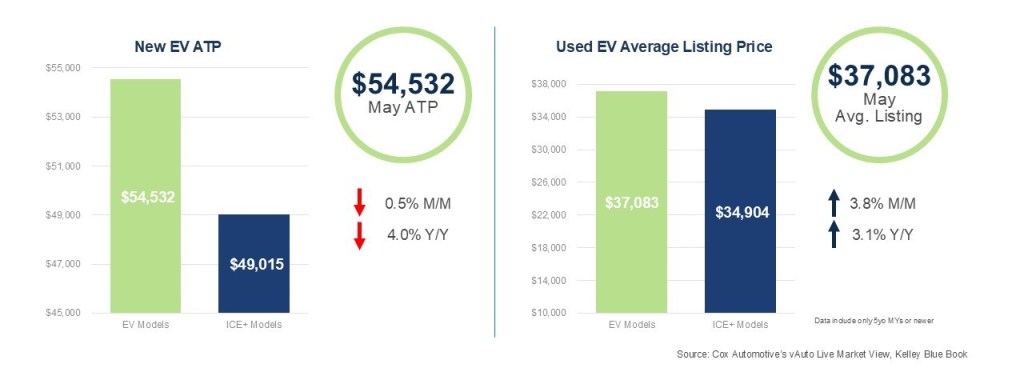

New and Used EV Prices – May

New EV ATP: The average transaction price (ATP) for a new EV in May was $54,532, down 0.5% month over month and 4% year over year, marking the 11th consecutive month of annual price declines. Incentives remained elevated and largely unchanged at 14% of ATP, or approximately $7,611 per vehicle.

The month-over-month movement primarily reflected volume-leader Tesla’s ongoing downward pressure on industry ATP, with pricing declining 1% month over month and 3.4% year over year in May. Industry pricing might have been lower if not for improved volume across several mid-to-higher priced EV models and brands, including Cadillac and BMW, and sales declines in lower-priced, high-volume entries, particularly Chevrolet.

For more detail, read the May Kelley Blue Book ATP report.

Used EV Listing Price: The average listing price for a used EV was $37,083 in May, up 3.8% month over month and 3.1% year over year. The increase was broad-based, with 31 makes posting higher prices, including several high-volume brands such as Tesla, Chevrolet, Hyundai, and Volkswagen.

Compared to ICE+, the used-EV price premium widened in May to $2,227, up from $1,398 in April, as used-EV price gains outpaced ICE+ on a month-over-month basis.

Looking Ahead:

New-EV sales are expected to trend slowly higher over time as new products reach the market and elevated incentives continue to support sales. Still, the path forward will remain uneven—as it has throughout the transition—driven by inconsistent consumer demand and shifts in automaker strategies. In the used market, the story is far more consistent and predictable. Improving availability is helping build momentum, while growing interest in more affordable EVs should support a gradual, healthy expansion in sales.

The EV Market Monitor gauges the health of the new and used electric vehicle (EV) markets by monitoring sales volume, days’ supply and average pricing. Each metric will be measured month over month and year over year.

Follow the link to view the entire series of EV Market Monitor reports.

For the official quarterly report on EV sales data, see the Q1 Electric Vehicle Sales Report.