Key Metrics

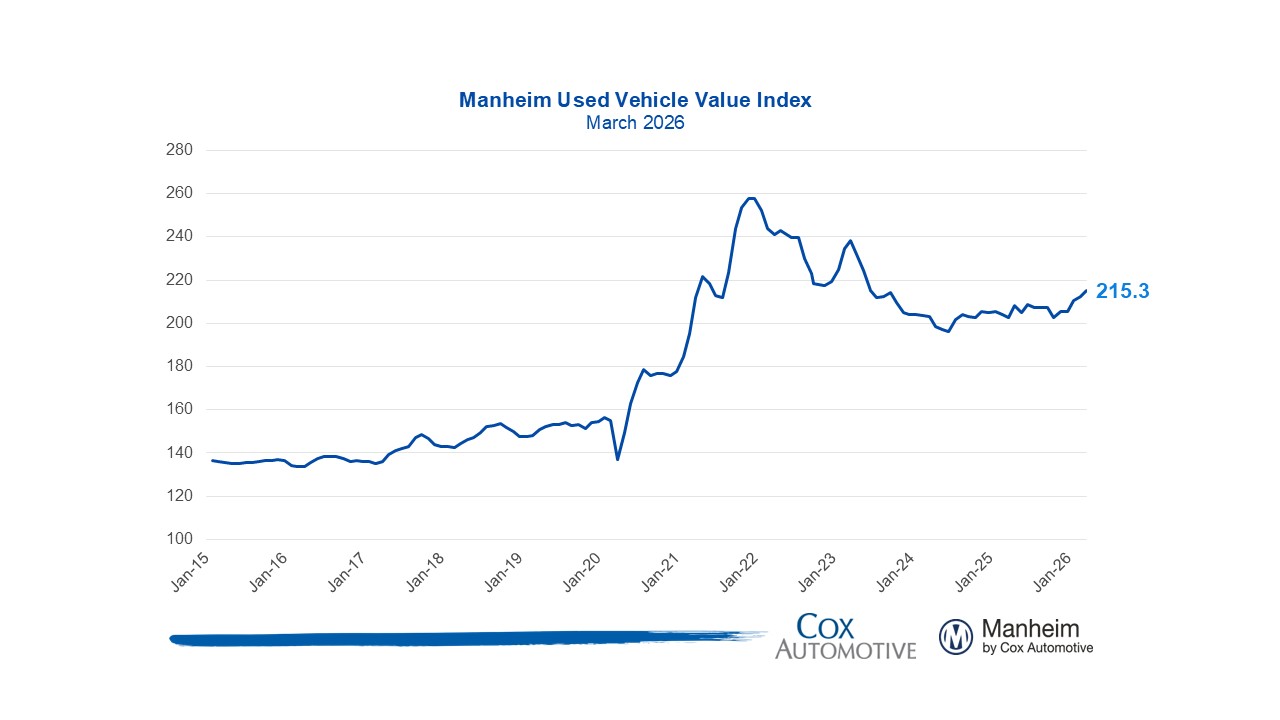

- The Manheim Used Vehicle Value Index (MUVVI) rose to 215.3, reflecting a 6.2% increase for wholesale used-vehicle prices (adjusted for mix, mileage, and seasonality) compared to March 2025. The March index is up 1.4% month over month. The long-term average monthly move for March is flat.

- Non-adjusted wholesale vehicle prices are now up 5.7% year over year, and up 4.2% against February. The long-term average monthly move in non-adjusted values is an increase of 3.4% in March.

Expert Perspective — Jeremy Robb, Chief Economist, Cox Automotive

“As soon as this year began, prices at Manheim started moving higher as dealers anticipated strong demand from higher tax refunds to consumers. Sales conversion rates, a clear sign of demand, were higher against 2025 for every week but one in Q1, and vehicle value trends at auction show we are well ahead of last year and where we would normally be during a spring bounce in the wholesale markets.

EV prices at wholesale are rising just as higher off-lease maturities for electric vehicles return to the market, pushing EV weighting to a record 3.9% in the MUVVI data for March. We expect dealers are anticipating increased interest for used EV’s as gas prices have now risen above $4.00 per gallon and are stocking up on EV inventory.

As we move towards summer, we expect Manheim values to hold their ground with many more consumers yet to file their tax returns this year. The end of March typically proves to be the ‘peak’ for price action at Manheim, but the way this tax-refund season is unfolding, it could continue for a bit longer. We thought we’d see some impact from the Middle East conflict, and that may still happen. But right now, the data is clear: used-vehicle demand is healthy and inventory levels are relatively tight.”

Prices, Retention & Sales Conversion

- MMR prices for the Three-Year-Old Index increased 2.2% in March.

- MMR retention averaged 100.5%, flat year over year and up 0.2 percentage points from February.

- Sales conversion was 68.2% for the period, 4.6 percentage points higher than the most recent three-year average for March and up 5.5 percentage points from the upward revised February rate.

Takeaway: MMR prices for the Three-Year-Old Index increased slightly more than is typical for this period. MMR retention increased slightly and is seasonally normal for this time of year. Meanwhile, sales conversion indicates strengthening demand, remaining well above usual levels for this time of year.

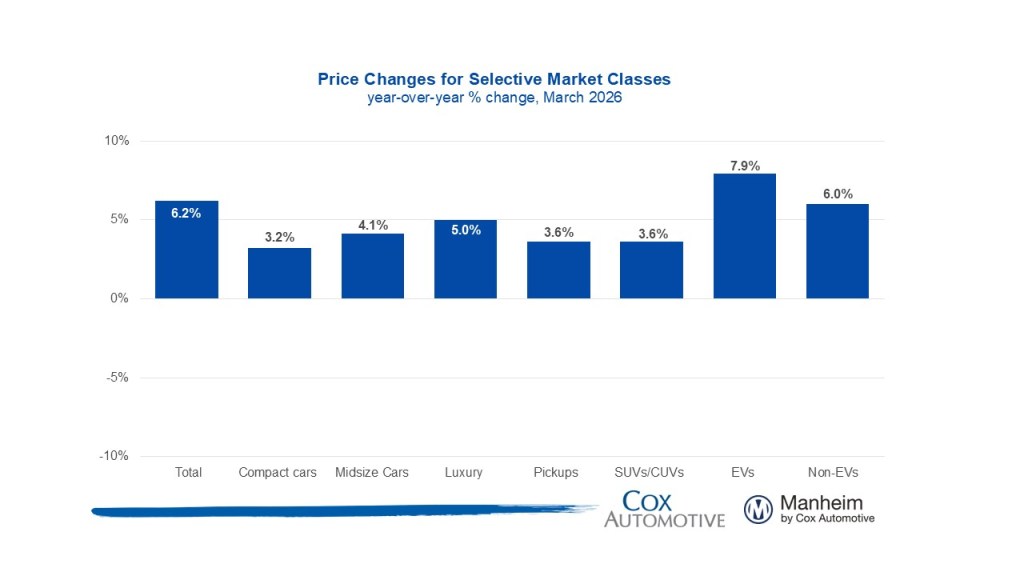

Segment Performance: Year-Over-Year Price Changes

Overall market prices were up notably from a year ago, led by strength in the luxury and midsize car segments, while compact cars posted the weakest gains.

Takeaway: All major vehicle segments are above year-earlier levels; however, the luxury segment continues to outperform the overall market. Continued strength in this segment has been observed throughout the past year. Compact cars and trucks continue to see relatively weak price growth compared to this time last year.

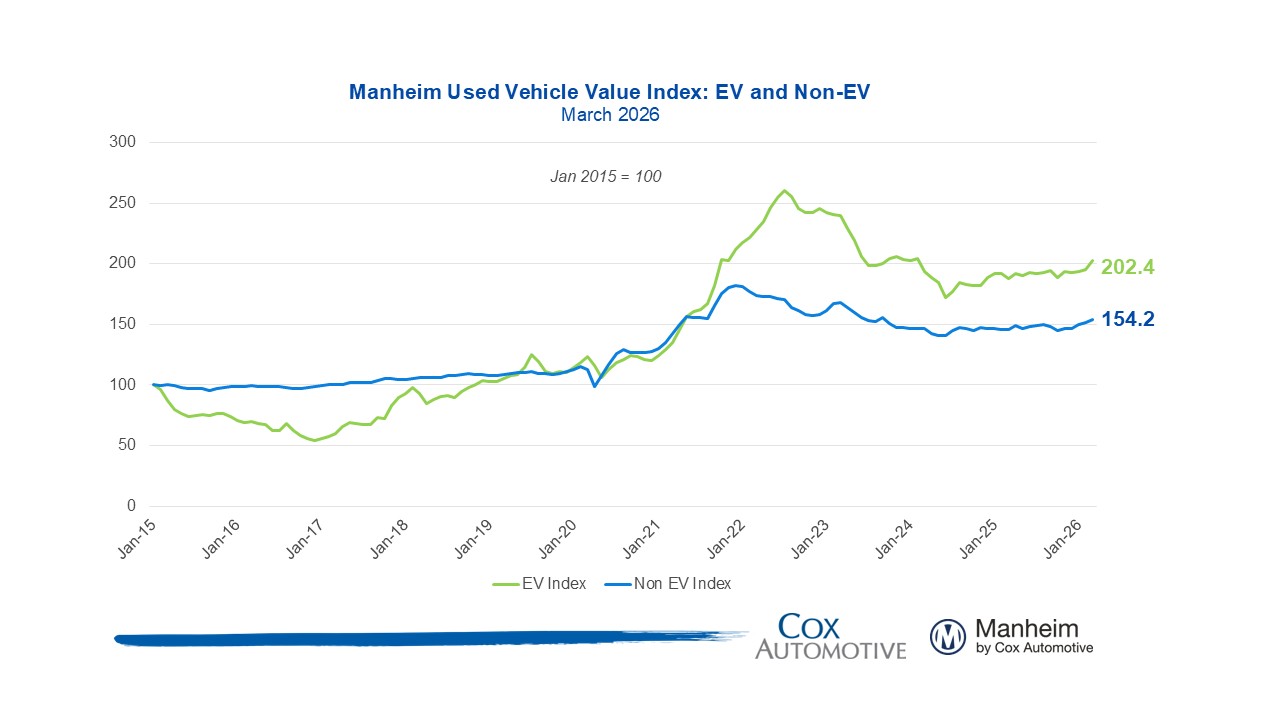

EV versus Non-EV Index

- EVs: The Electric Vehicle (EV) Index was up 7.9% year over year and up 3.7% from February.

- Non-EVs: The Non-EV Index was up 6.0% year over year and higher by 1.8% from February.

Takeaway: Both EV and Non-EV have seen notable price gains against this time last year, with EVs showing strength in the last month. Importantly, EV values have increased even as EV availability improved as more off-lease EVs return to market. In March, strong EV sales helped Manheim set a record for wholesale EV volume in Q1.

Wholesale Supply & Rental Prices

- Wholesale supply: At the end of March, wholesale days’ supply fell to 24.5 days, higher by 1 day year over year and lower by 2.5 days compared to February.

- Rental prices: Prices for rental vehicles are higher by 7.5% year over year, as they climbed in March, up by 0.7% from February. Rental values on a non-seasonally adjusted basis are 8.9% above 2025’s level and rose 3.7% in March, driven in part by lower average mileage, down 13% against last March overall.

Takeaway: Days’ supply in March was higher than recent historical norms but experienced a smaller decline than is typical from February.

View historical MUVVI reports here.

For more information on Manheim, visit Manheim.com.

The Manheim Used Vehicle Value Index (MUVVI) is a trusted benchmark for tracking wholesale used-vehicle prices in the U.S., which helps dealers and analysts gauge market shifts and anticipate retail trends. The official measure is reported on the fifth business day of each month. The mid-month MUVVI number is a checkpoint number, is not an official reading and should not be compared to the official index reading. The mid-month is not a flash estimate, and it is not meant to provide any directional estimate of the full-month number. The next complete suite of monthly MUVVI data will be released on Tuesday, April 7, 2026. Register to attend the Q1 MUVVI call on Tuesday, April 7, 11 a.m. EDT.

For questions or to request data, please email manheim.data@coxautoinc.com. If you want updates about the Manheim Used Vehicle Value Index, as well as direct invitations to the quarterly call sent to you, please sign up for our Cox Automotive newsletter and select Manheim Used Vehicle Value Index quarterly calls.

Note: The Manheim Used Vehicle Value Index was adjusted to improve accuracy and consistency across the data set as of the January 2023 data release. The starting point for the MUVVI was adjusted from January 1995 to January 1997. The index was then recalculated with January 1997 = 100, whereas prior reports had 1995 as the baseline of 100. All monthly and yearly percent changes since January 2015 are identical. Learn more about the decision to rebase the index.