ATLANTA, May 26, 2026 – The Q2 2026 Cox Automotive Dealer Sentiment Index (CADSI) shows a second consecutive quarterly gain in dealer current market sentiment, driven by stronger conditions following a healthy spring selling season. However, expectations for the months ahead declined sharply, reflecting growing concern about the economic outlook and consumer demand.

“The gains this quarter are in line with seasonal expectations we’ve seen in the past,” said Mark Strand, deputy chief economist at Cox Automotive. “Sales in March and April were healthy and helped boost current sentiment, but rising inflation, elevated fuel costs and geopolitical uncertainty are weighing on dealer confidence for the months ahead.”

Key Findings from Q2 2026 CADSI

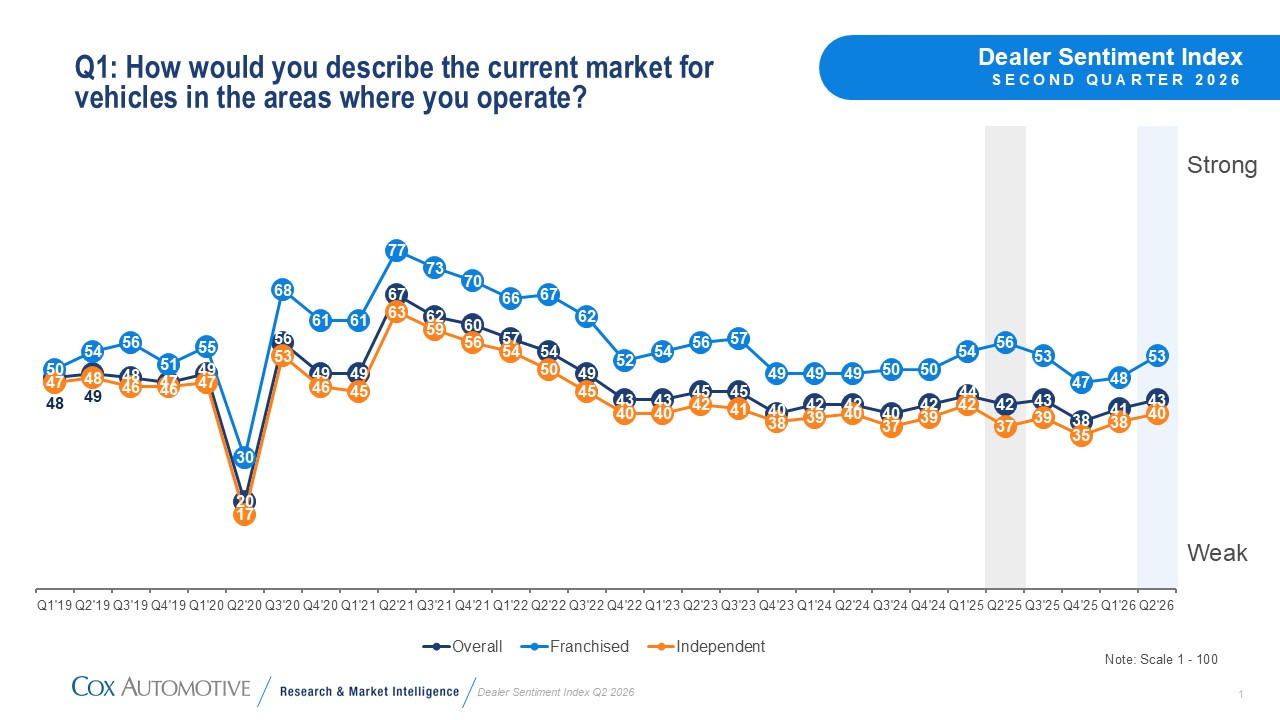

- Market Sentiment Improves but Remains Weak: Current market sentiment rose to 43 in Q2, up from 41 in Q1, marking a second consecutive quarterly increase. Despite the gain, the index remains below 50, indicating most dealers still view conditions as weak. Franchised dealers reported a current market index of 53, an increase of five points and signaling generally positive conditions. While independent dealer sentiment improved in Q2, it remained well below the positive threshold at 40.

- Future Outlook Weakens Sharply: Expectations for the next three months declined to 47 from 56 in Q1, falling below the positive threshold. Both franchised and independent dealers reported declines, with independent dealers seeing a more pronounced drop. While significant, the pullback was seasonally normal and follows the typical Q1 “spring bounce.” It also reflects increasing concern about inflation, economic conditions and softening consumer demand.

- Traffic Improves but Remains Soft: Sentiment toward customer traffic showed a notable rebound in Q2, rising 8 points to 36 from near-record lows in Q1. While still below the level considered strong, traffic is now closer to year-ago levels. Gains were observed by both franchised and independent dealers, with franchised dealers reporting stronger performance, particularly in online traffic.

- Profitability Edges Higher: Dealer profitability improved modestly in Q2, with the profit index rising to 36 from 32 in Q1. Despite the gain, profitability remains below last year’s level and well below the threshold of 50. Elevated costs continue to pressure margins, with the cost index rising to 74, its highest level in more than a year.

- Sales Environment Mixed: New-vehicle sales sentiment improved to 53, reflecting stronger sales in March and April. However, sentiment remains below year-ago levels. Used-vehicle sales sentiment was unchanged at 44 and lower than one year ago, continuing to signal weak conditions overall. A widening gap persists between dealer types, with franchised dealers reporting strong used-vehicle conditions, while independent dealers continue to face challenges.

- Inventory Stabilizes and Pricing Pressure Persists: New-vehicle inventory levels for franchised dealers held steady, while used-vehicle inventory remained tight, particularly for independent dealers, where supply constraints intensified. Despite inventory still being constrained, dealers report feeling elevated pressure to reduce prices compared to one year ago. However, the price pressure index, while above year-ago levels, is at historically normal levels.

- EV Sentiment Shows Early Signs of Stability: Dealer sentiment toward electric vehicle sales improved modestly from recent lows, with both dealer groups reporting improved sentiment, signaling early signs of stabilization after a period of decline. While overall EV sentiment in Q2 remains below levels considered strong, independent dealers are seeing improving opportunities in the used EV market, supported by better pricing and availability. At the same time, franchised dealers remain less optimistic, reflecting ongoing concerns about current and future EV sales.

Key Factors Holding Back Business, Led by Economy and Political Climate

Dealers identified several key headwinds limiting business activity in Q2, led by broader economic concerns. The Economy remains the top factor holding back business, cited by more than half of dealers, reflecting ongoing concerns about inflation, fuel costs and overall consumer affordability.

Factors Holding Back Business in Q2

| Q2 2026 | Q1 2026 | Q2 2025 | ||

| 1 | Economy | 55% | 52% | 51% |

| 2 | Market Conditions | 40% | 37% | 40% |

| 3 | Political Climate | 36% | 31% | 33% |

| 4 | Expenses | 33% | 34% | 32% |

| 5 | Interest Rates | 32% | 34% | 42% |

Market Conditions rank as the second most-cited challenge, as dealers continue to face uneven demand, pricing pressure and soft consumer confidence. Political Climate is now the third most significant factor, up from number five last year and last quarter, with concern rising notably in Q2 as dealers point to geopolitical tensions and policy uncertainty weighing on confidence.

Operational and financial pressures round out the top five. Expenses remain a persistent challenge, as higher operating costs continue to pressure margins, while elevated Interest Rates are limiting consumer purchasing power and making financing more difficult for many buyers.

Cox Automotive Dealer Sentiment Index Methodology

The Cox Automotive Dealer Sentiment Index (CADSI) is derived from a quarterly survey of a representative sample of franchised and independent auto dealers across the United States. The Q2 2026 CADSI is based on responses from approximately 958 dealers, including 502 franchised dealers and 456 independent dealers.

The survey was conducted from April 21 to May 4, 2026. Responses are weighted by dealership type and sales volume. Index scores assign values of 100 for strong/increasing, 50 for average/stable, and 0 for weak/decreasing. The margin of error is approximately ±3%.

About Cox Automotive

Cox Automotive is the world’s largest automotive services and technology provider. Fueled by the largest breadth of first- and third-party data fed by 2.3 billion online interactions a year, Cox Automotive tailors leading solutions for car shoppers, auto manufacturers, dealers, lenders and fleets. The company has 29,000+ employees on five continents and a portfolio of industry-leading brands that include Autotrader®, Kelley Blue Book®, Manheim®, vAuto®, Dealertrack®, NextGear Capital™, CentralDispatch® and Cox Fleet®. Cox Automotive is a subsidiary of Cox Enterprises Inc., a privately owned, Atlanta-based company with $23 billion in annual revenue. Cox Automotive has been included on Glassdoor’s Best Companies in Tech & AI 2026 and Best Place to Work in 2026 lists. Visit coxautoinc.com or connect via @CoxAutomotive on X, CoxAutoInc on Facebook or Cox-Automotive-Inc on LinkedIn.

Media Contacts:

Mark Schirmer

734 883 6346

mark.schirmer@coxautoinc.com

Dara Hailes

470 658 0656

dara.hailes@coxautoinc.com