The headline is easy to write. The average new vehicle transacts consistently at or around $50,000. It is also easy to understand why that number gets so much attention.

The point came through clearly in Cox Automotive’s 2026 Mid-Year Review presentation. The big number matters, but on its own, it can steer the affordability conversation in the wrong direction.

Average MSRP—the sticker price—is not simply a measure of how vehicles are priced. It is an average of more than a million data points each month, reflecting both automaker pricing and consumer choice. Increasingly, the new-vehicle market is being supported by wealthier households, and buyers are choosing vehicles with more features, more technology, and more capability.

That does not mean affordability is not a problem. It is. But the problem is bigger than the sticker price on the vehicle. The broader economic environment matters, and it matters a lot.

Start With the Household Budget

For consumers, dealers, and the industry, affordability is real. But it is not a vehicle-pricing story alone.

As Cox Automotive Chief Economist Jeremy Robb noted in the recent Mid-Year Review, the core issue facing consumers is the erosion of purchasing power. For many households, the cost of living has risen faster than income over the past several years, pressuring nearly every line of the budget.

Vehicles are one of the largest purchases consumers make, so they are highly visible in any affordability debate. But they now compete with higher costs for housing, energy, insurance, groceries, and other everyday essentials. That is the context consumers bring with them when they walk into the market.

Then Look at What the Average Price Actually Measures

Since January, the average new-vehicle MSRP in the U.S. has been north of $51,000. But that figure reflects the mix of vehicles sold. Like the average temperature in a given year, it includes plenty of readings below the average and plenty above it.

Base models still exist. Automakers continue to build them, and they are available on dealer lots. But many consumers are choosing better-equipped trims and vehicles with more advanced features. At the same time, more affluent households are accounting for a larger share of new-vehicle demand, and those buyers often gravitate toward higher-priced models.

A big part of that shift comes from the evolution of what consumers now expect as standard. Safety features such as automatic emergency braking, pedestrian detection, and lane departure warning were once premium add-ons. Today, they are widely expected.

Many of these features are not mandated by regulations. Organizations like the Insurance Institute for Highway Safety do not establish requirements. They provide ratings, and those ratings carry significant weight with consumers, purchase decisions and, in some cases, insurance costs.

Automakers are not building to the legal minimum. They are building to consumer expectations and competitive realities. Safety, technology, and convenience features have become part of the baseline product. That added capability carries real value, and real cost.

A Decade of Change, and a Better Product

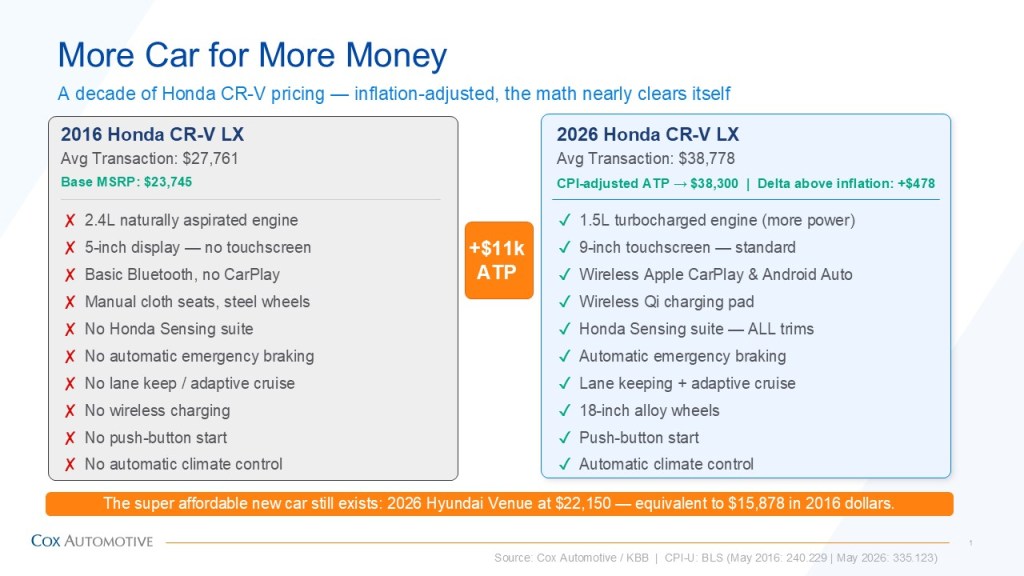

The Honda CR-V, a consistent consumer benchmark, helps show the point. Over the past decade, the average transaction price for a CR-V has increased by roughly $11,000, from around $28,000 in 2016 to about $39,000 today.

That sounds like a big increase. Adjusted for inflation, however, the difference nearly disappears. In real terms, the price is essentially where it was 10 years ago.

What has changed dramatically is the product itself. Today’s CR-V includes turbocharged performance, advanced infotainment, wireless smartphone integration, and driver-assistance technologies that were optional or unavailable a decade ago. It is a better, more capable vehicle by almost any measure. Once adjusted for inflation and income growth, the price has barely moved.

The same pattern appears at the entry point. The most affordable new vehicle today is priced around $22,000, which translates to just under $16,000 in 2016 dollars. The nominal entry price has moved higher, but much of that increase reflects inflation rather than a fundamental reset in affordability.

Consumers Are Not Being Irrational

There is also a common-sense piece to this. When the price gap between a base vehicle and a better-equipped model is relatively small, many buyers choose the vehicle with more features, better fuel efficiency, or stronger long-term usability.

That behavior is rational. Consumers are thinking about total value, not just the lowest entry price. Over time, those choices shift the sales mix and lift the industry average. The headline number moves, but the underlying story is consumer choice.

So, What Does “Affordable” Really Mean?

The narrative that new vehicles have become unaffordable simply because sticker prices average near $50,000 misses the point. Today’s vehicles are more advanced, more capable and more content-rich than those sold a decade ago. In real terms, many have held their value remarkably well.

The bigger issue is the economic environment around the vehicle. Purchasing power has been stretched, household budgets are under pressure, and consumers are absorbing higher costs across nearly every part of daily life.

Vehicle insurance has risen sharply. Auto loan rates are higher, so borrowing costs more. Maintenance and repair costs are up. Gasoline is higher, too. So are housing, groceries, healthcare, and subscription services.

In that environment, it is no surprise that a new vehicle feels out of reach for many Americans. But the issue isn’t the car itself — it’s because life got more expensive.

The $50,000 headline captures attention, but not the full story. Vehicle affordability remains critical, and consumers feel it every day. But understanding why the market feels so expensive requires looking beyond the sticker price. The car is not the villain here. The broader cost environment is.