Highlights

- Job growth for April decelerated, falling short of expectations and adjusting down previous estimates, contributing to a broader discussion on labor market trends and economic indicators.

- The Federal Reserve left rate policy unchanged at the conclusion of their meeting last week and acknowledged a lack of progress in achieving their 2% inflation target.

- The automotive sector presents a mixed picture, with new-vehicle sales slowing and new-vehicle prices ticking upward in April. Fleet sales deteriorated further relative to the overall market.

Job Growth and Unemployment Dynamics

April’s job growth has taken a significant dip, falling below expectations and revising down the tally of previous months, contributing to a broader discussion on labor market trends and economic indicators as viewed through the lens of vehicle sales, Federal Reserve policies, and average transaction prices in the auto industry.

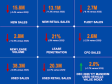

- April saw 175,000 jobs created, a figure notably lower than the anticipated 240,000.

- The unemployment rate slightly increased from 3.8% to 3.9%, with the labor force participation rate holding steady at 62.7%.

- The three-month moving average of new jobs fell to 242,000, which was the slowest pace in four months.

Federal Reserve’s Stance and Inflation Concerns

- The Federal Reserve maintains its interest rate policy amidst slow progress towards its 2% inflation target, hinting at future rate cuts possibly starting from July. [See the commentary published last week: Deflation and Fed’s Lack of Urgency Are Putting Durable Goods at Risk]

- A dovish approach toward quantitative tightening was unexpectedly adopted, influenced by April’s labor market softness.

- The Fed remains “on pause,” but understands rates are restrictive and need to be cut at some point this year.

Auto Industry Insights and Pricing Trends

- New light vehicle sales dropped by 3.3% year over year in April, with the initial estimated average transaction price rising to $48,510 – the highest mark since December but down 0.5% year over year. (The full Kelley Blue Book price report will be posted next week.)

- Despite a slight year-over-year decrease in average transaction prices, incentives from manufacturers remained significantly higher than the previous year.

- The average price relative to the average manufacturer’s suggested retail price (MSRP) moved up to 97.6% as the level of discounting declined modestly. The average MSRP increased 2.2% in April and was up 1.3% year over year.

- Fleet sales overall declined 5.6% compared to last year, with notable differences across rental, commercial and government segments.

- Sales into large rental fleets were down 2.0% year over year, while sales into commercial fleets were down 14.3%, but sales into government fleets were up 8.3%.