The U.S. new-vehicle market entered May with mostly stable inventory levels and a modest decline in overall volume as automakers deliberately rebalance inventory by clearing out MY2025 vehicles.

Industry days’ supply, as measured by vAuto Live Market View, declined 2.4% month over month in April to 78, well below levels near 95 days recorded in January and February. Compared to April 2025, however, days’ supply was higher by 15.5%, a significant shift mostly explained by an accelerated sales pace last spring, which was artificially elevated by tariff concerns. Of note in the latest inventory report: total supply of MY2025 vehicles declined sharply, down 36% month over month, signaling a continued push to clear older models.

2.86M

Total Inventory

as of April 2026

78

Days’ Supply

$49,025

Average Listing Price

Industry View: Volume Remains Mostly Stable

April data appears mostly uneventful, with total available inventory declining to 2.86 million units, down 1.1% from March but higher from year-earlier levels by 8.2%. The underlying volume drivers show a market actively working through a transition and balancing two competing priorities: clearing outgoing model year inventory while maintaining discipline on newer production.

Across several major automakers, the decline in MY2025 supply suggests an intentional effort to move older units, particularly in segments where inventory had expanded meaningfully earlier in the year. Steady sales velocity and targeted incentives had the desired effect. At the end of April, approximately 93% of total inventory was MY2026 product.

At the same time, newer model year inventory appears to be entering the market at a more measured pace. This reflects a degree of production discipline, as total volume of available inventory declined compared to March, even with implied total sales down 2% month over month. The result is a more controlled inventory environment, where overall supply and incentive levels remain mostly stable.

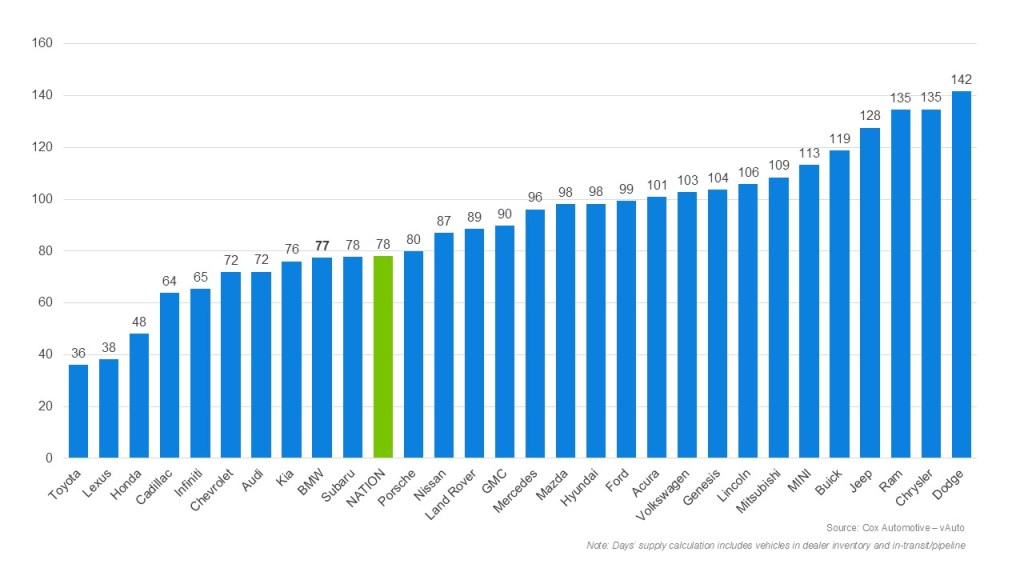

April Days’ Supply of Inventory by Brand

Looking across key volume brands, April data mostly shows how inventory levels are being well managed in most cases. Domestic automakers continue to show pockets of inventory expansion in core truck and utility segments, but these increases are being offset by efforts to reduce older model-year stock. In contrast, several import brands show a more balanced profile, with steadier supply levels but some variability in sales pace across sedan segments indicating consumer’s focus on affordability.

Pricing and Incentives: Prices Increase but Remain Below Long-Term Averages

The average listing price increased to $49,025 in April, up a notable 0.9% from the revised lower March reading ($48,605) but higher by only 1.3% year over year — an increase below long-term averages. As in prior months, stability in pricing likely reflects a combination of disciplined inventory management and downward price pressure driven by affordability challenges, waning consumer sentiment, and a slowing market.

Industry-wide incentive spending is being held down by stable inventory levels, and there is little evidence of broad-based price reductions. Instead, automakers appear to be relying on targeted incentives to move specific inventory, particularly older model-year vehicles, while protecting pricing on newer units.

According to Kelley Blue Book estimates, the average transaction price (ATP) for a new vehicle in April was $49,461, up 1.8% from one year earlier. ATPs were higher by 0.7% from March, above the long-term average of 0.3%. Incentive spending declined month over month in April, falling to 6.9% of ATP from 7.2% in March, likely reflective of good inventory management.

The Bottom Line: Stability Masking Strategic Rebalancing

April’s inventory data points to a market that is neither tightening nor loosening materially but rather holding steady in the face of strengthening headwinds. The sharp reduction in model year 2025 inventory, combined with steady pricing and modest improvements in days’ supply, reflects a coordinated effort to hold supply more in line with demand.

The key takeaway is that the market is not simply stabilizing — it is actively working through older inventory while maintaining control over new supply. As the industry moves through the second quarter, the ability to sustain that balance will determine whether stability holds or new pressures begin to emerge.

View Historical New Vehicle Inventory reports.