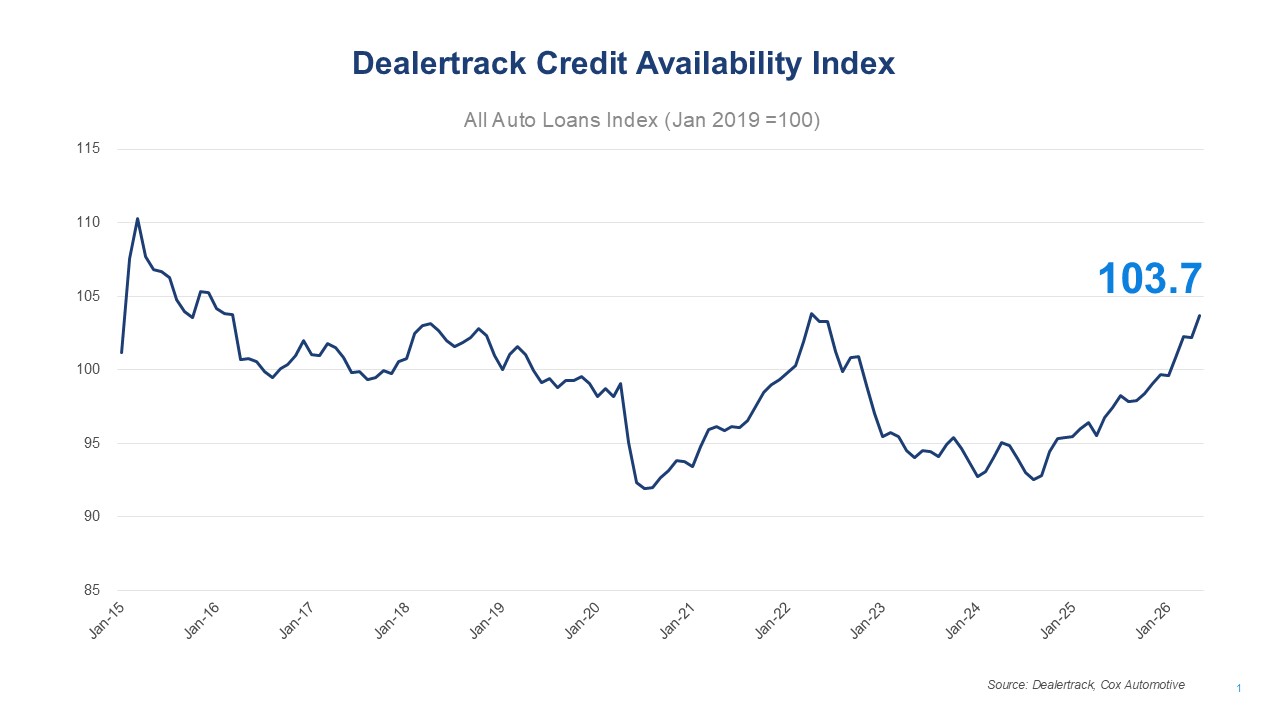

In May 2026, the Dealertrack Credit Availability Index rose to 103.7, its highest level since April 2022. The All-Loans Index increased 1.5% from April’s 102.2 and is up about 7.3% from May 2025. While the index posted one of its stronger monthly gains in recent years, the move was concentrated, with two components driving the advance and a decline in subprime share acting as the primary offset.

Key Metrics

- Approval Rates: The overall loan approval rate rose to 72.4% in May, up 180 bps from April’s 70.6%, a notable monthly gain, and up 50 bps year over year from 71.9%. The continued improvement in approval conditions was the second-largest contributor to the month’s index gain, behind only the yield spread.

- Subprime Share: The share of loans to subprime borrowers declined 70 bps month over month from 17.4% to 16.7%, the second consecutive monthly decline following March’s spike at 19.5%. Despite two months of pullback, subprime share remains up 270 bps year over year from 14.0% in May 2025, reflecting conditions that are still more positive for higher-risk borrowers than a year ago. The monthly decline partially offset the gains from the yield spread and approval rates.

- Yield Spread: The yield spread narrowed 53 bps (from 7.25% to 6.72%), accounting for the majority of May’s index gain. The narrowing reflected both modest rate declines across credit tiers and a modest shift in loan mix away from subprime borrowers, with the average contract rate falling 32 bps to 10.87% while the 5-year Treasury rose 21 bps to 4.15%. Year over year, the spread is now down 50 bps from 7.22% in May 2025.

- Loan Term Length: The share of loans with terms greater than 72 months reached 30% in May, a new all-time high in the dataset and up 30 bps from April’s 29.7%. The higher share is a positive for the index, as it reflects lenders extending longer terms to support broader credit access. Year over year, long-term loan share is up 370 bps from 26.3% in May 2025, reflecting a growing acceptance of longer loan durations on both sides of the transaction.

- Negative Equity Share: The share of loans with negative equity declined 120 bps from 58.5% to 57.3% in May. Despite the monthly easing, negative equity remains up 250 bps year over year from 54.8% in May 2025, with a substantial share of borrowers continuing to carry loan balances that exceed their vehicle’s value.

- Down Payment Percentage: Down payments edged up 10 bps from 13.4% to 13.5% in May, consistent with the largely flat trend throughout 2026. Down payment percentage is now running about 60 bps below year-ago levels of 14.1% in May 2025.

Channel and Lender Trends

- Channels: Credit access improved broadly by channel in May. The largest month-over-month gains were in Independent Used and All Used, followed by solid improvements in All New, Non-Captive New, and Franchise Used. Used CPO was essentially flat on the month. Despite the monthly variation, credit availability across all channels remains meaningfully above year-ago levels, with All New continuing to lead year-over-year gains.

- Lender Types: Lender performance was mixed in May. Credit Unions were the only lender type to improve, rising 1.4%, while Banks were essentially flat. Captives declined 0.3% and Finance Companies edged lower, down 0.5%. Despite the overall index advance, subprime tightening and negative equity easing were large enough drags at the individual lender level to outweigh the upward contribution of narrowing yield spreads for three of four lender types. All four lender types remain well above year-ago levels, with Captives and Banks continuing to lead year-over-year improvement.

Year-Over-Year Comparison

- Channels: The most notable year-over-year improvements were in All New and Franchise Used, indicating continued strength across both new- and used-vehicle segments. Independent Used and Non-Captive New also posted solid gains, while All Used improved broadly. Used CPO saw a more modest year-over-year improvement.

- Lender Types: Captives and Banks continued to lead year-over-year improvement, while Finance Companies also posted solid gains. Credit Unions, while improving recently on a month-over-month basis, posted the most modest year-over-year gain.

Implications for Consumers and Lenders

- Consumers: May brought a more favorable financing environment relative to April. The yield spread narrowed 53 bps and the average contract rate fell 32 bps to 10.87%, reflecting both modest rate declines across credit tiers and a modest shift in loan mix away from subprime borrowers. For consumers who financed in May, this represented more favorable borrowing costs. Approval rates also improved meaningfully, giving more buyers access to financing.

- The broader picture, however, carries important cautions. The share of loans exceeding 72 months reached 30% in May, a new all-time high, and remains nearly 370 bps above year-ago levels. Negative equity still runs 250 bps above May 2025 levels, and down payments are about 60 bps below year-ago levels. The combination of longer terms, lower down payments, and more negative equity carried forward increases total loan cost and risk exposure over the life of the financing, regardless of how manageable the monthly payment appears. Consumers should carefully consider the full terms of any financing offer, particularly total loan length and overall cost.

- Lenders: Despite the total index reaching its highest level since April 2022, three of four lender type indices fell or were flat in May, a signal that portfolio-level dynamics varied significantly from the headline. Approval rates expanded and yield spreads narrowed in May, driving the overall index gain and indicating more favorable conditions for borrowers. However, the narrowing yield spreads also represents a narrowing margin for lenders, which adds stress.

- The continued pullback in subprime share for a second consecutive month is shifting the loan mix toward less risky borrowers, though subprime remains meaningfully elevated relative to a year ago. Long-term loan share reaching a new all-time high and negative equity remaining well above year-ago levels are also key watchpoints. Writing loans at extended terms to borrowers already carrying negative equity represents a compounding of duration and collateral risk in the portfolio, and the concentration of loans with these characteristics continues to grow. Balancing volume growth with underwriting discipline in the current environment remains a key consideration.

Bottom Line: The May 2026 Dealertrack Credit Availability Index closed at 103.7, its highest level in four years. The advance was driven primarily by a narrowing yield spread and a sharp recovery in approval rates, with a modest increase in long-term loan share adding incremental support. A pullback in subprime lending served as the primary offset. Extended loan terms at a new all-time high and elevated negative equity remain key watchpoints even as the headline index improves.

View historical Dealertrack Credit Availability Index reports.

The Dealertrack Credit Availability Index tracks six factors that affect auto credit access: loan approval rates, subprime share, yield spreads, loan term length, negative equity and down payments. Reported monthly, the index indicates whether access to auto credit is improving or declining. This typically means that it is cheaper and easier for consumers to obtain a loan or more expensive and harder. The index is published around the tenth of each month.