Available new-vehicle inventory totaled 2.82 million units in June, down 2.4% from May and mostly unchanged from a year earlier. The daily new-vehicle sales pace slowed 5% from May, which benefited from five weekends, but remained 4.1% higher than a year ago, according to data from vAuto Live Market View.

Days’ supply increased to 80 in June, up from a revised-higher 78 in May, a shift that was driven more by softer sales than growing inventory. Overall, the new-vehicle market continues to look reasonably well balanced, with inventory levels holding mostly consistent throughout much of 2026, suggesting good discipline by most automakers.

2.82M

Available Units

80.3

Days’ Supply

$49,336

Average Listing Price

Inventory Is Still a Brand-Level Story

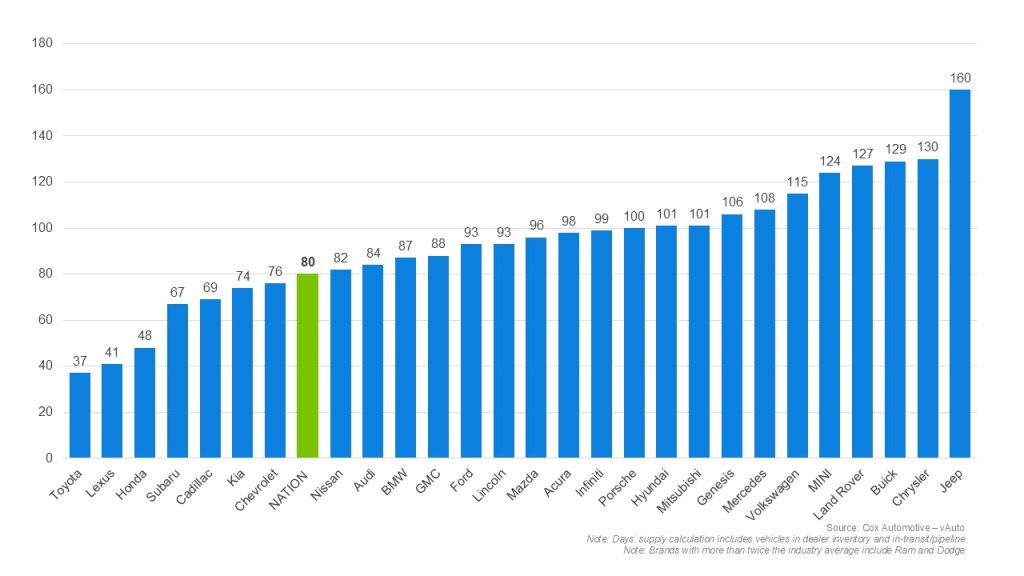

Toyota entered July with the tightest inventory, as measured by days’ supply, followed by Lexus and Honda. These brands continue to turn inventory quickly, reflecting a combination of strong consumer demand and relatively lean supply. Subaru and Cadillac also remained below the industry average, while Kia and Chevrolet finished the month at 74 days and 76 days, respectively.

June Days’ Supply of Inventory by Brand

Meanwhile, some brands continue to work through much larger inventory positions. Stellantis brands, particularly Jeep, Ram and Dodge, continue to address elevated inventory levels. High days’ supply at Stellantis has become a familiar part of the inventory narrative this year and highlights one of the market’s defining characteristics: While overall inventory levels may look balanced, supply is far from evenly distributed across brands. Worth noting: Even among brands with elevated days’ supply, incentive discipline appears to be holding. Jeep, for example, even with days’ supply at twice the industry average, had incentive levels at 6.7% of ATP in June, according to Cox Automotive estimates, below the industry average of 7%.

An additional development this year has been the general consistency in overall inventory management. While days’ supply was elevated in January and February, the industry has largely avoided the significant increases that often develop when consumer sentiment declines and economic pressure increases. In other words, the new-vehicle market seems mostly unfazed by higher gas prices and the uncertainty of a war in the Middle East. Through June, the market has been mostly steady in the face of traditional headwinds.

The Average is Near $50,000; Reality is Closer to $35,000

The average listing price of a new-vehicle increased to $49,336 in June, up 1.4% from a year earlier and higher by 0.3% from the revised-lower May estimate. The largest concentration of available vehicles, however, remains in the $30,000-to-$40,000 price range, where dealers had more than 688,000 units at month-end, roughly 24% of available inventory. The average listing price within that segment was $35,377, and days’ supply measured 70 days, well below industry average. In June, 28% of vehicles sold were priced in this $30,000-to-$40,000 range.

That helps explain why the industry’s average price can sometimes paint an incomplete picture. While average listing prices remain near $50,000, a healthy pool of vehicles – 34% of available inventory – sits much lower, priced below $40K. Recent data from Cox Automotive, including the June Cox Automotive/Moody’s Analytics Vehicle Affordability Index, continues to show that affordability pressures today are increasingly tied to broader economic pressures on American household rather than rapidly rising vehicle prices. (Read more here.)

Balanced, but Still Competitive

June’s inventory data suggests that inventory levels remain stable, sales remain healthy despite economic headwinds, and days’ supply continues to hold in a range that most automakers would consider manageable. And while affordability remains a challenge for many consumers, the industry’s largest inventory concentrations are still centered well below the headline making average of $50,000.

View Historical New Vehicle Inventory reports.