Key Metrics

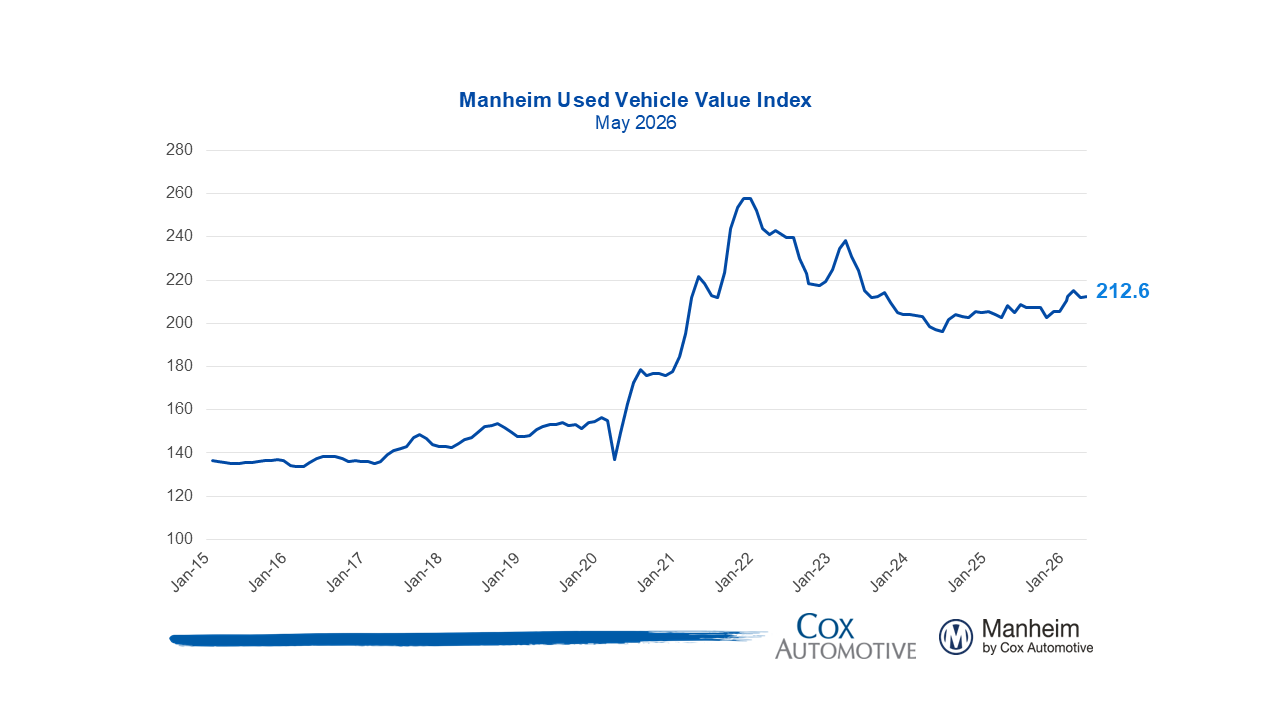

- The Manheim Used Vehicle Value Index (MUVVI) rose to 212.6, reflecting a 3.6% increase for wholesale used-vehicle prices (adjusted for mix, mileage, and seasonality) compared to May 2025. The May index is up 0.3% month over month. The long-term average monthly move for May is an increase of 0.9%.

- Non-adjusted wholesale vehicle prices are now up 3.1% year over year, and down 1.2% against April. The long-term average monthly move in non-adjusted values is a decrease of 0.3% in May.

Expert Perspective — Jeremy Robb, Chief Economist, Cox Automotive

“Wholesale value trends continue to normalize from a strong start to the year, as we start to move into summer months and consumers continue to contend with higher gas prices. The Manheim Index overall remains higher against last year, yet it wasn’t as strong as we normally see within the month. As values were much higher in February and March, they just started to normalize and depreciate in May, with non-seasonally adjusted prices falling a bit over one percentage point in the month. But the big picture shows good balance in supply and demand, with days’ supply sitting at pretty seasonal levels, even if it remains a bit below last year.

In May of last year, we were still contending with tighter supply from tariff-induced demand, and currently, sales conversion (dealer demand), still looks good at Manheim. Further, we continue to see dealers bidding up the prices of EVs faster than Non-EV values at Manheim, consistent with gas prices that remain higher by 38% against last May. EV mix at Manheim holds steady for now, and it will continue to increase over the year as off-lease EV supply continues to rise.

Affordability concerns continue, as we’ve seen higher appreciation in older units at Manheim this year – a trend we’ve been calling out recently. Additionally, some of the most affordable segments are showing the highest gains so far this year with compact cars higher by 12.3% in non-adjusted values since December, the highest of any major segment. With only one month left in the first half of the year, trends look decent for wholesale markets. The second half could bring some volatility as off-lease supply continues to ramp up, which could pressure some segments in the back half.”

Prices, Retention & Sales Conversion

- MMR prices for the Three-Year-Old Index decreased 1.3% in May.

- MMR retention averaged 99.5%, up 0.4 percentage points year over year and down 0.2 percentage points from April.

- Sales conversion was 59.9% for the period, 4 percentage points higher than the most recent three-year average for May but down 3 percentage points from the April rate.

Takeaway: MMR prices for the Three-Year-Old Index decreased a typical amount for this period. MMR retention fell less than is seasonally normal for this time of year. Meanwhile, sales conversion indicates a further softening of demand but remains above usual levels for this time of year.

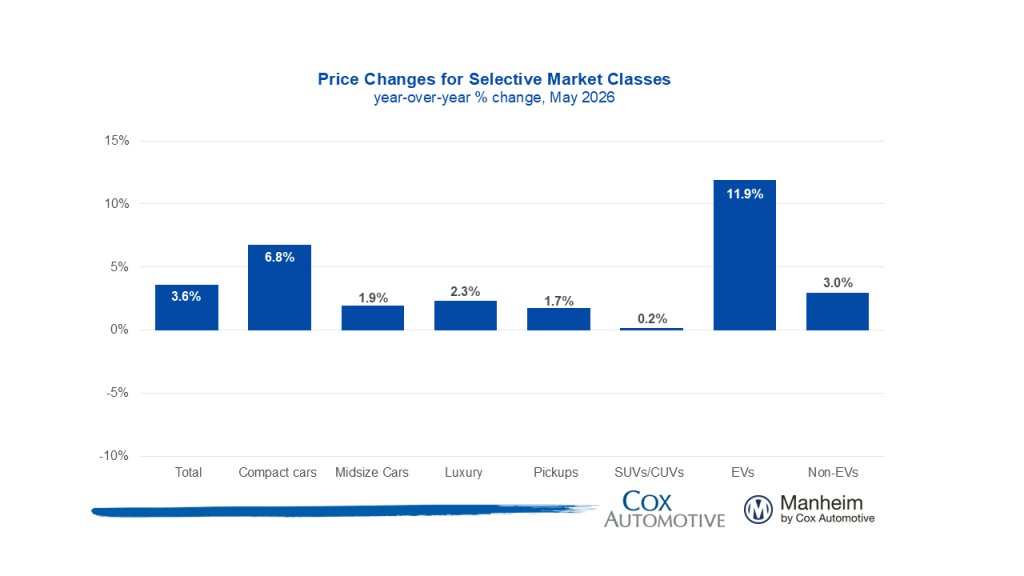

Segment Performance: Year-Over-Year Price Changes

Overall market prices were up from a year ago, led by continued EV strength and recent growth in compact cars.

Takeaway: While the compact car segment posted gains above industry average for the first time in 2026, the story in May was the continued strength of EVs at Manheim. Even with more availability, strong EV performance continues. SUVs, meanwhile, continue to lag the overall market and were the weakest among the major segments in May.

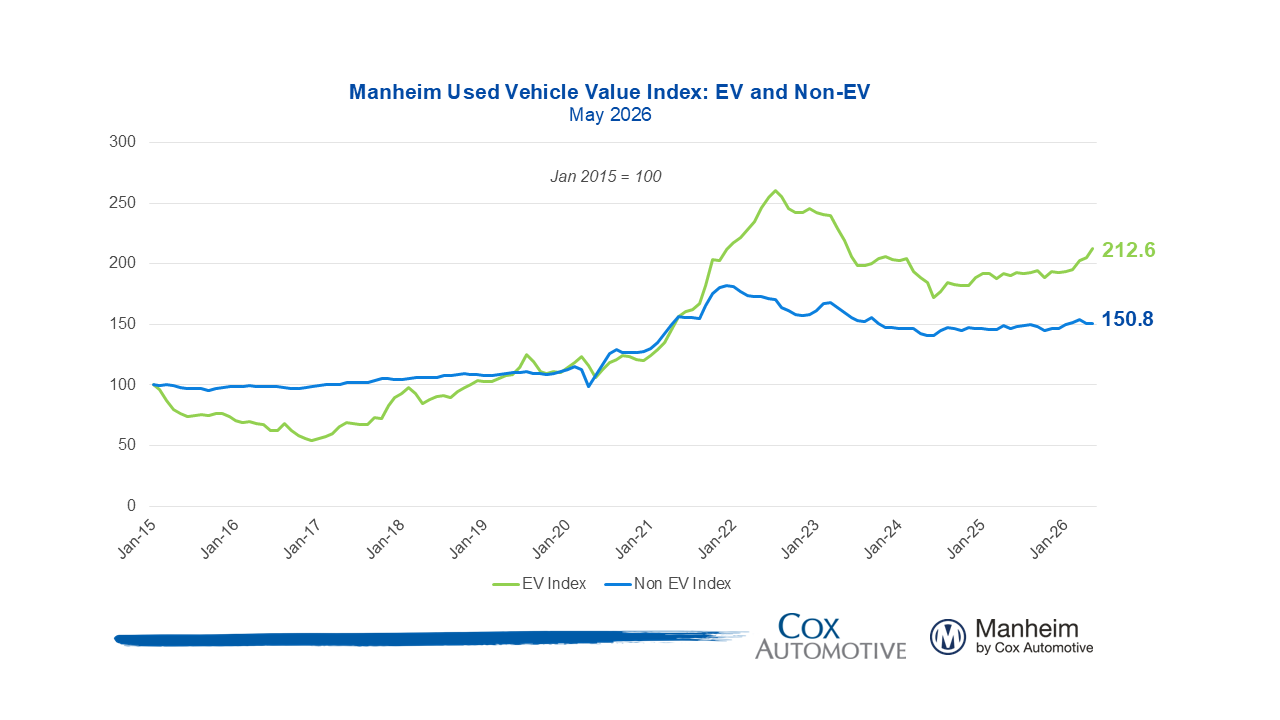

EV versus Non-EV Index

- EVs: The Electric Vehicle (EV) Index was up 11.9% year over year and up 3.5% from April.

- Non-EVs: The Non-EV Index was up 3% year over year and flat from April.

Takeaway: Both EV and Non-EV continue to see elevated prices against this time last year, with EVs showing continued strength in the last month while Non-EVs held steady.

Wholesale Supply & Rental Prices

- Wholesale supply: At the end of May, wholesale days’ supply rose to 26 days, higher by 1 days year over year and higher by 1 day compared to April.

- Rental prices: Prices for rental vehicles are higher by 2.4% year over year, falling in May, down by 1.6% from April. Rental values on a non-seasonally adjusted basis are 1.7% above 2025’s level but fell 2.7% in May, while having lower average mileage, down 15.1% against last May.

Takeaway: Days’ supply in May was elevated against last year, yet remains within seasonal boundaries. Rental values fell against April, consistent with an increase in average mileage M/M.

View historical MUVVI reports here.

For more information on Manheim: VISIT MANHEIM.COM

The Manheim Used Vehicle Value Index (MUVVI) is a trusted benchmark for tracking wholesale used-vehicle prices in the U.S., which helps dealers and analysts gauge market shifts and anticipate retail trends. The official measure is reported on the fifth business day of each month. The next complete suite of monthly MUVVI data will be released on May 7, 2026.

For questions or to request data, please email manheim.data@coxautoinc.com. If you want updates about the Manheim Used Vehicle Value Index, as well as direct invitations to the quarterly call sent to you, please sign up for our Cox Automotive newsletter and select Manheim Used Vehicle Value Index quarterly calls.

Note: The Manheim Used Vehicle Value Index was adjusted to improve accuracy and consistency across the data set as of the January 2023 data release. The starting point for the MUVVI was adjusted from January 1995 to January 1997. The index was then recalculated with January 1997 = 100, whereas prior reports had 1995 as the baseline of 100. All monthly and yearly percent changes since January 2015 are identical. Learn more about the decision to rebase the index.