May’s new-vehicle market was defined by a clear three-part story: Inventory stayed essentially steady, sales accelerated, and days’ supply tightened as a result. vAuto Live Market View showed 2.89 million units in inventory in May, up modestly from April and broadly in line with the 2026 average, while the faster sales pace pulled supply lower across most brands.

Even with consumer confidence subdued and inflation concerns back in focus, the daily retail selling rate rose 6.5% from April and 9.6% year over year. Listing prices also climbed to a 2026 high of $49,307, indicating that demand is still holding up even as vehicle prices migrate higher.

2.89M

Total Inventory

as of May 2026

76

Days’ Supply

$49,307

Average Listing Price

Steady Supply, Faster Sales

Compared with the tariff-driven volatility of 2025, the 2026 market has been notably more orderly. Retail sales momentum has improved since January, and May marked the strongest daily sales pace of the year. At the same time, inventory has remained within a relatively narrow range, allowing days’ supply to fall from the weather-distorted February peak of 96 to 76 in May.

May inventory reached 2.89 million units, up from 2.86 million in April, 5.6% above January, and 13% higher than a year earlier. Even so, the broader pattern remains one of steady supply rather than renewed accumulation. That year-over-year increase also reflects a tougher comparison base: Spring 2025 inventory was depleted by a sales pace that ran above 17 million SAAR in March and April, draining dealer lots.

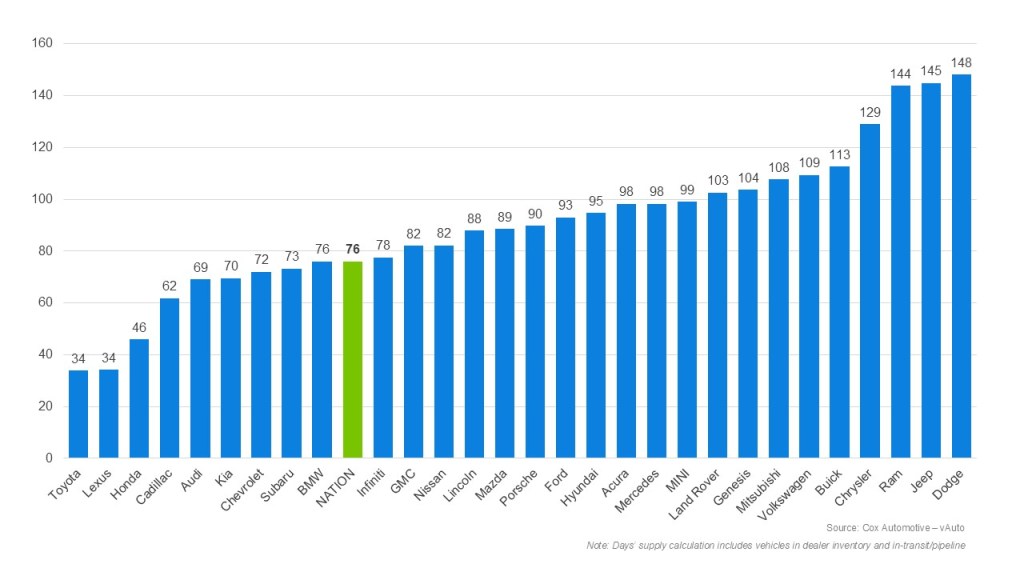

May Days’ Supply of Inventory by Brand

At the brand level, Nissan remains the clearest example of the broader thesis: Days’ supply fell to 82 in May, down from both April and a year earlier, largely because sales accelerated. The opposite pattern remains most visible at Stellantis, where Chrysler, Dodge, and Jeep continued to post materially higher supply levels year over year as inventory growth outpaced demand. Together, those cases explain the market well: Tighter supply where sales are working, looser supply where sale volume is not clearing inventory fast enough.

Pricing Holds, Pressure Persists

Prices continue to show discipline, but that should not be mistaken for improved affordability. The average listing price rose to a 2026 high of $49,307 in May, up 1.2% year over year. Roughly 56% of available inventory was priced below $50,000, and 25% sat in the $30,000-to-$40,000 range, showing there is still volume in the core of the market even as the average remains elevated.

Kelley Blue Book data reinforces that point. Average transaction prices fell 0.5% month over month to $49,220 and were up just 1.2% from a year earlier, the smallest annual gain of 2026 and well below the typical May increase. MSRP growth was also subdued at 1.6% year over year. In other words, pricing has not broken higher—but financing costs and household budget pressure still mean many consumers do not experience this market as meaningfully easier.

Incentives rose to 7.1% of ATP in May, continuing a gradual climb, but not to a level that suggests widespread distress. Instead, the market is still showing selective support: Incentives are helping sustain demand while pricing strength remains concentrated in high-volume segments such as midsize SUVs, compact SUVs, and full-size pickups.

Balanced, Not Easy

The market looks balanced, but it is not broadly comfortable. Demand is still holding up better than many expected, supported in part by a solid labor market and wealth effects at the higher end, yet elevated financing costs and household budget pressure continue to cap how far that strength can carry. For automakers, the key takeaway is that inventory discipline is working. Supply is tighter not because the market has become easy, but because sales are moving well enough to prevent inventories from building meaningfully.

View Historical New Vehicle Inventory reports.