Much has changed since the first week of March. COVID-19 cases keep getting worse and will lead to a substantial economic contraction in the second quarter. The rest of the year could see some recovery, but it is too early now to call. There is some hope on the horizon with drug trials for treatments and vaccines. Meantime, we will closely monitor numerous economic indicators and our own internal metrics in the weeks ahead.

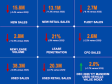

Vehicle sales fall: We measured a clear and significant drop in new and used retail sales in the week ending March 14. New retail vehicle sales declined 24% from the prior week and were down 29% year over year. Used vehicle sales saw a decline of 29% from its big jump the prior week and were down 19% year over year. Our leading indicators point to more declines ahead.

Consumer sentiment falls: The first estimate of March consumer sentiment from The University of Michigan saw a decline of 5% from the final reading in February. Both measures of current conditions and future expectations declined, but it was expectations that declined the most, down 7.4%.

As a frame of reference, as the Great Recession began at the end of 2007, consumer sentiment fell ahead of the recession started and fell 6% in the month just before the recession began. A newer and daily measure of consumer sentiment from Morning Consult shows confidence as of Friday, March 20 having declined 16.8% since Jan. 1.

Fed rate cuts: The Fed cut rates in a surprise emergency move last Sunday, March 15. Since last Tuesday, longer-term bond yields like those on the 10-year U.S. Treasury actually moved up. These rates influence consumer rates like on auto loans more than the Fed.

The opposite move in rates was a reaction to massive fiscal stimulus driving demand for shorter-term bonds at the expense of longer-term bonds and because of lender risk aversion leading to higher yield spreads. The 10-year bonds moved down at the end of the week and are now trending closer to the previous week’s average.

Auto rates mixed: Mortgage rates moved up last week and are more than 35 basis points higher than last month. We saw slight declines in average auto rates by the end of the week, but subprime new vehicle loan rates are not going down. The Fed is now trying to influence longer-term rates to move lower. They are having some success with the 10-year, but these moves are not translating to what consumers see because of lender risk aversion.

Retail sales drop: February retail sales fell 0.5%, which was below consensus expectations of growth. The retail sales data show that consumer spending softened even before COVID-19 was declared a pandemic. February saw declines in sales of clothing, furniture and electronics.

Housing mixed: Housing was the good news story of much of last year and the start of this year, but February was a bit more mixed. Housing starts declined 1.5% to a SAAR of 1.599 million, which was actually above consensus expectations as warmer weather in January and February helped drive more construction activity at a time of the year when it is typically much slower. The bigger concern is that permits fell 5.5% to a SAAR of 1.464 million, which was below consensus expectations. When the rate of starts exceeds the rate of permits, starts are likely to decline in future periods. Existing home sales had a strong February, as the existing-home sales SAAR jumped 6.5% to 5.77 million, the highest level of sales since 2007. This was thanks to a strong economy and lower mortgage rates.

Tax refunds down: Updated data from the IRS through Friday, March 13, show that tax refund volumes and amounts continue to be down even though processed returns are now even with this time last year. Total refunds are down 1.1% in number and down 0.6% in dollar amount. The average refund is up by 0.5% year over year. We estimate that well over half of the refunds have been disbursed, and that’s why the used vehicle market was so strong in the first week of March.

Jobless claims climb: Initial claims for jobless benefits jumped to 281,000 from 211,000 previously for the week ending Saturday, March 14. This was worse than analysts expected and is likely just a fraction of what we may see this week, which means the U.S. will be seeing a big jump in the unemployed by month end.

Check back tomorrow for a video that will include updated data.