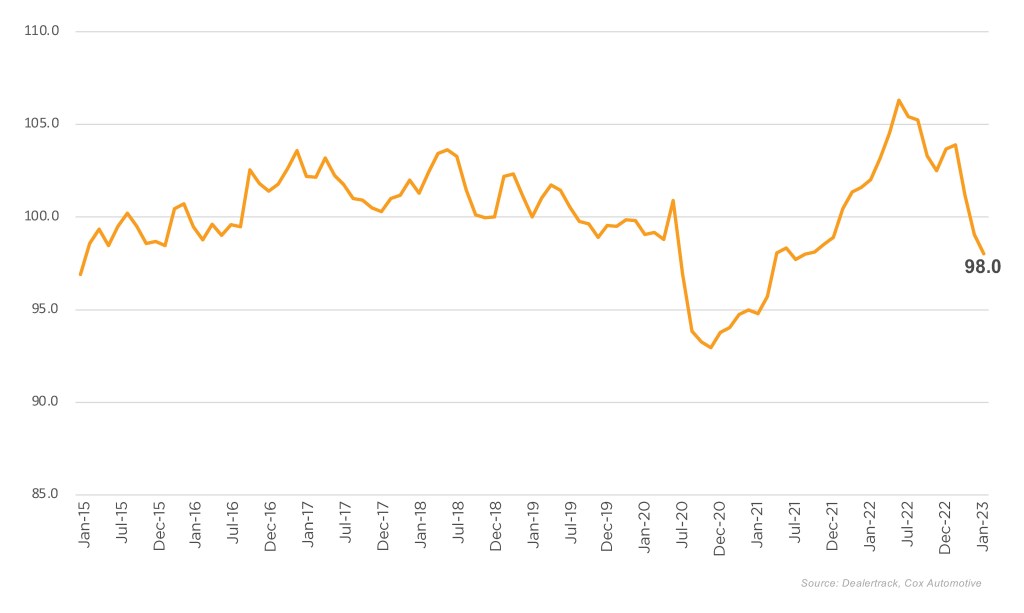

Access to auto credit tightened again in January, according to the Dealertrack Credit Availability Index for all types of auto loans. The All-Loans Index declined 1% to 98.0 in January, reflecting that auto credit was harder to get in the month compared to December. The decline in access reflected conditions that were tightest since June 2021. With the decline in January, access was tighter by 3.9% year over year, and compared to February 2020, access was tighter by 1.2%.

Dealertrack Credit Availability Index

Auto loan access declined again in January pushing access further down year over year

All Auto Loans Index (Jan2019=100)

Credit Availability Factors Mixed in January

Movement in credit availability factors was mixed in January. Yield spreads widened, the subprime share declined, and the share of loans with negative equity declined, and these moves limited credit access for consumers. However, consumers were helped by a lengthening in terms and a slightly higher approval rate. Down payments were unchanged but remained at a record high. The average yield spread on auto loans widened, so the rates consumers saw on auto loans were less attractive in January relative to bond yields. The average auto loan rate increased by 2 Basis Points (BPs) in January compared to December, while the 5-year U.S. Treasury declined by 11 BPs, resulting in a wider average observed yield spread.

In addition to rate changes, the most significant year-over-year changes were subprime share, approval rate and average down payment percentage. The subprime share declined to 10.3% in January from 11.0% in December and was down 1.5 percentage points year over year. The approval rate increased by 0.2 percentage points but was down 1.9 percentage points year over year. The average down payment percentage was up 1.8 percentage points year over year.

Access to Most Loan Types Tightened

Most loan types saw tightening in January, with only used loans acquired through independent dealers loosening, while certified pre-owned (CPO) loans tightened the most. On a year-over-year basis, all channels were tighter, with new loans having seen the most tightening over the last year.

Credit access tightened across most lender types in January, with only auto-focused finance companies loosening and banks tightening the most. On a year-over-year basis, credit access was tighter across most lender types except auto-focused finance companies. Over the last year, credit unions have tightened the most.

Each Dealertrack Auto Credit Availability Index tracks shifts in loan approval rates, subprime share, yield spreads and loan details, including term length, negative equity, and down payments. The index is baselined to January 2019 to show how credit access shifts over time.

Measures of Consumer Confidence Mixed in Janusry

The Conference Board Consumer Confidence Index® declined 1.7% in January, as views of the present situation improved, but future expectations fell by 6.7%. Plans to purchase a vehicle in the next six months were unchanged from December and were down slightly year over year. The confidence index did not decline as much during the pandemic as the sentiment index from the University of Michigan, but that series improved in January. The Michigan index increased 8.7%, driven primarily by improvement in the view of current conditions, which was up 15.2%. Consumers’ views of vehicle buying conditions have improved to the best level since July 2021. The daily index of consumer sentiment from Morning Consult measured modestly declining sentiment in January, as that index declined 1.5% for the month. Sentiment declined in January as the price of gasoline increased. According to AAA, the national average price for unleaded gas increased 9% in January to $3.50 per gallon on Jan. 31, which was up 4% year over year.

The Dealertrack Credit Availability Index is a monthly index based on Dealertrack credit application data and will indicate whether access to auto loan credit is improving or worsening. The index will be published around the 10th of each month.