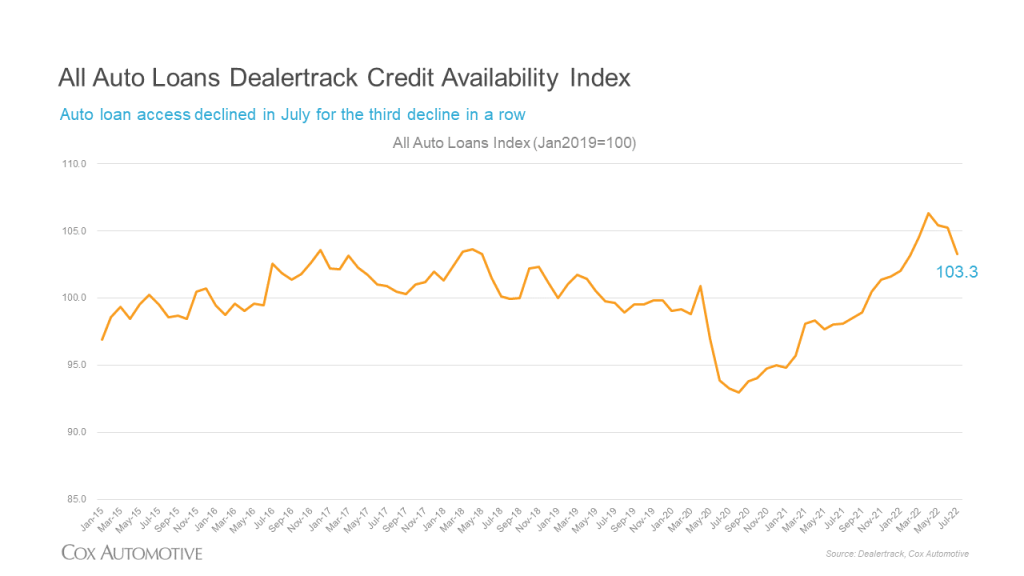

Access to auto credit declined across the board in July according to the Dealertrack Auto Credit Availability Index for all types of auto loans. The All-Loans Index declined 1.8% to 103.3 in July, reflecting that auto credit was harder to get in the month compared to June. The index has declined for three consecutive months, but access was looser by 5.3% year-over-year, and compared to February 2020, access was looser by 4.2%. The index in April 2022 had been the highest recorded in the data series going back to January 2015.

The credit availability factors mostly moved against consumers in July. The average yield spread on auto loans widened, so rates consumers saw on auto loans were less attractive in July relative to bond yields. The average auto loan rate increased by 26 basis points (BPs) in July compared to June, while the 5-year U.S. Treasury declined by 23 BPs, resulting in a wider average observed yield spread.

The approval rate fell, and the subprime share declined, which worked against consumer access to credit in July as well. The only factor to move in support of consumers in July was an increase in loan terms. Negative equity share and down payment size were stable in July relative to June.

All loan types saw tightening in July. All new loans and new loans through non-captives tightened the most. Used loans through independent dealers tightened the least in the month. On a year-over-year basis, all channels saw higher credit access with used CPO loans having loosened the most.

Credit access declined across all lender types in July compared to June, with credit unions tightening the most and captives and auto-focused finance companies tightening the least. On a year-over-year basis, all lenders had looser standards with auto-focused financed companies having loosened the most.

Each Dealertrack Auto Credit Index tracks shifts in loan approval rates, subprime share, yield spreads and loan details including term length, negative equity, and down payments. The index is baselined to January 2019 to provide a view of how credit access shifts over time. Across all auto lending in July, yield spreads widened, the approval rate declined, and the subprime share declined, so those factors moved against accessibility. Terms lengthened slightly and that helped mitigate some of the tightening.

Measures of consumer sentiment improved in July. The Conference Board Consumer Confidence Index® declined 2.7% in July when a smaller decline had been expected, and the June index was also revised down. Most of the index decline was driven by a 4.0% decline in expectations. Plans to purchase a vehicle in the next six months declined to the lowest level so far this year and were down substantially year over year. The confidence index has not fallen as much as the sentiment index from the University of Michigan, but that series improved in July. The Michigan index increased 3% from a record low in June, as it is much more sensitive to inflationary changes and stock market moves. Similarly, the Morning Consult Index of Consumer Sentiment increased by 3.3% in July. These more inflation-sensitive measures moved higher as gas prices declined 16% by the end of July from the peak in June.

The Dealertrack Credit Availability Index is a new monthly index based on Dealertrack credit application data and will indicate whether access to auto loan credit is improving or worsening. The index will be published around the 10th of each month.