Revised, May 11, 2023 – New-vehicle supply closed March at its highest level in two years despite surprisingly brisk sales, according to Cox Automotive’s analysis of vAuto Available Inventory data. Days of supply has remained relatively steady while the average listing price edged lower.

1.89M

Total Inventory

as of March 27, 2023

57

Days’ Supply

$46,949

Average Listing Price

The total U.S. supply of available unsold new vehicles on dealer lots and some in transit stood at 1.89 million units at the end of March, up from a revised 1.80 million at the end of February. The end of March marked the highest level of supply since April 2021. Supply was up 70% from a year ago, or 780,000 units higher.

Days’ supply was 57, down only a day from the end of February but up 58% from the same time a year ago. Historically, a 60 days’ supply across the industry was considered normal and ideal.

The Cox Automotive days’ supply is based on the daily sales rate for the most recent 30-day period that ended March 27, when about 1.02 million vehicles were sold, up 8% from the same period in the previous year.

For the full calendar month of March, total new-vehicle sales were up 9% from a year ago for a sales pace, or seasonally adjusted annual rate (SAAR), of 14.8 million, up from 13.6 million a year ago but down from February’s revised 15 million. Total sales in March were buoyed by double-digit increases in fleet sales, as has been the case for the past few months.

“During March, we saw sales surpass the 1-million mark for a 30-day period for the first time since early September 2021,” said Charlie Chesbrough, Cox Automotive senior economist. “Higher sales have been boosted, in part, by improving inventory, which has been running at around 1.8 million or so for the past several weeks.”

While inventory is up substantially from 2022 levels, it remains low by historical standards. At the end of pre-pandemic March 2019, the total supply was 3.87 million vehicles for a 94 days’ supply.

New-Vehicle Prices Fall Throughout March

The average new vehicle listing price – the asking price – fell weekly through March to below $47,000 for the first time since December. The average listing price at the close of March was $46,949, down from the revised $47,257 at the end of February. Still, the average price is up 6% from a year ago.

The average transaction price (ATP) – the price paid – in March slipped again, closing the month at $48,008, down 1.1% or $550 from February, according to Kelley Blue Book. These are still high prices, up 3.2% or nearly $1,784 from a year ago.

“With some brands and segments nearing too-high levels of inventories, we are seeing discounts and incentives increase,” said Chesbrough. “We are beginning to see more incentives, particularly leasing deals, crop up.”

Indeed, the two-year trend of Americans paying over the manufacturer’s suggested retail price (MSRP) ended for the first time in 20 months. Further, automakers’ spending on incentives rose to the highest level in a year, reaching a still-low 3.2% of the ATP in March, averaging $1,516 per vehicle.

Supply Shows Wide Variation by Brand, Segment, Price and Region

At the close of March, the industry had non-luxury vehicle inventory totaling 1.60 million vehicles, up from 1.53 million at the end of February, for a 55 days’ supply. The inventory of luxury vehicles (excluding uber luxury ones) stood at 290,852 units, up from 271,591 at the end of February, for a 60 days’ supply.

Import non-luxury and luxury brands had the lowest inventories. The highest inventories were a mix of domestic brands, dominated by Stellantis’ brands, and a mix of luxury makes.

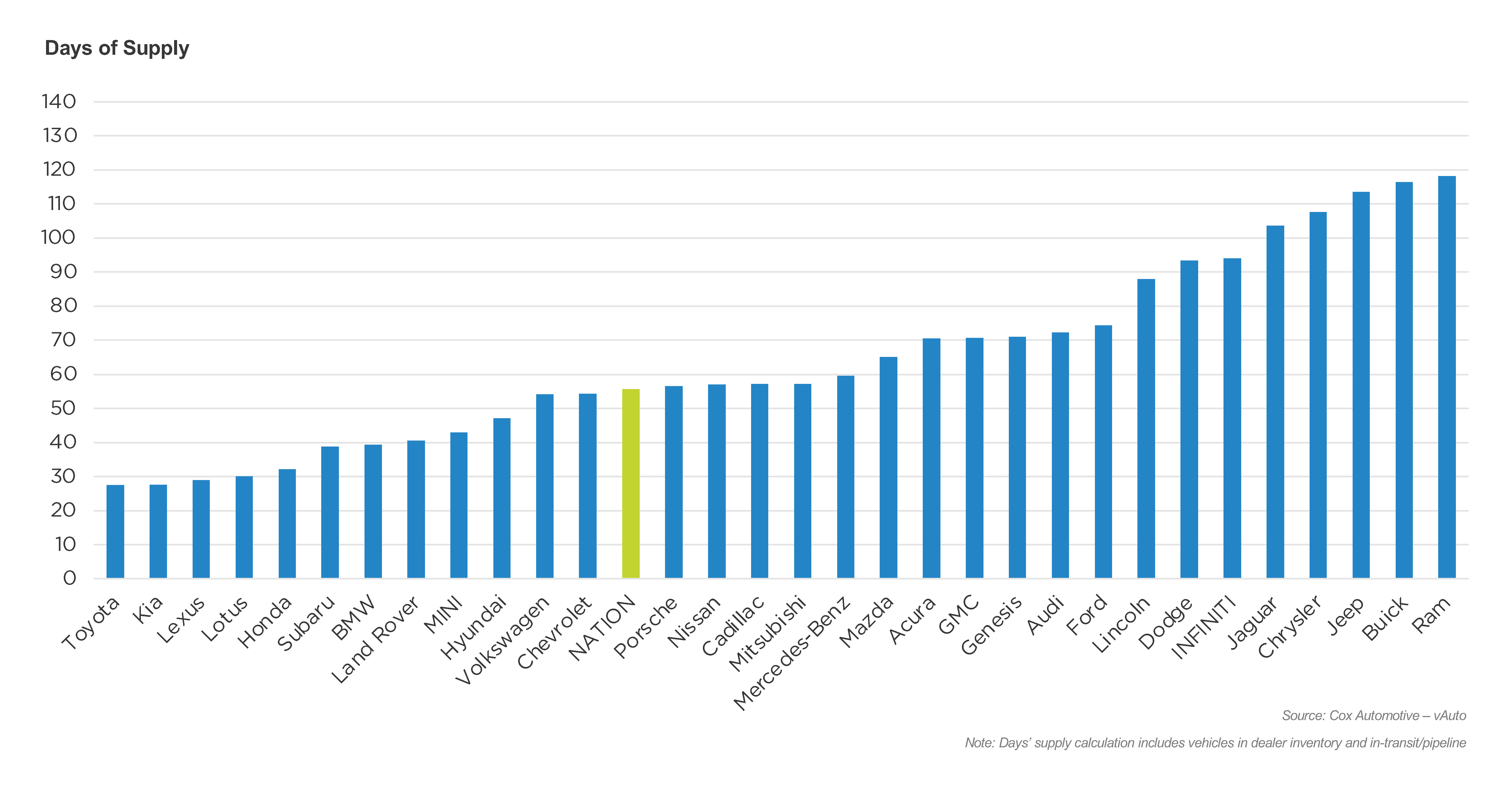

Non-luxury brands with the lowest inventory were Toyota and Kia, under 30 days’ supply, followed by Honda, Subaru, Hyundai, Volkswagen and Chevrolet, all with below-industry average supply. Luxury brands at the low end were Lexus, with under 30 days of supply, followed by BMW and Land Rover.

Non-luxury brands with the highest inventory were mostly Stellantis brands, with four among the top for supply. Ram was the highest with 119 days’ supply, followed by Jeep and Chrysler. Luxury brands with the highest inventory were Buick, at 117 days’ supply, followed by Jaguar and Infiniti.

March Days’ Supply of Inventory By Brand

Aside from low-volume, high-performance cars, vehicles that are often popular with budget-minded Americans— subcompact cars, compact cars, and mid-size cars—had the lowest supply, followed by minivans, and compact and subcompact SUVs. Excluding niche uber luxury, full-size cars and luxury cars had the highest inventory, followed by full-size pickup trucks at 85 days’ supply, which is up from the end of February but not completely out of line for what is normal for pickup trucks because they come in a wide array of configurations.

Of the 30 best-sellers for the 30 days that ended March 27, Kia Telluride, Subaru Crosstrek, Toyota RAV4, Toyota Camry and Subaru Forester all had under 30 days of supply.

Of the 30 best-sellers for the period, full-size pickup trucks from the Detroit Three had the biggest supply. The Ram 1500 had a 102 days’ supply. Ford F-150 and Chevrolet Silverado had days’ supply between 80 and 90 days. GM has idled two full-size truck plants to reduce inventory levels.

By DMA, Florida, California and Southern DMAs had the lowest supply. Northern ones had the highest. Miami-Fort Lauderdale had the lowest inventory, followed by Orlando-Daytona Beach, Los Angeles, Tampa and Atlanta, all less than 55 days’ supply. Minneapolis-St. Paul and Detroit had the highest at 72 days’ supply, followed by Boston and Denver.

Lower price categories had the tightest supply by the end of March. Under $20,000, a segment with an active supply of just under 2,700 units and a 24 days’ supply. Between $20,000 and $30,000, the days’ supply was 40. The $30,000 to $40,000 segment had a 43 days’ supply. The $40,000 to $50,000 category had a 54 days’ supply. The $50,000 to $60,000 category had a days’ supply of 69. The $60,000 to $80,000 group had the highest days’ supply at 82. The over $80,000 segment had a 59 days’ supply.

More insights are available from Cox Automotive on new-vehicle inventory, using a 30-day rolling sales methodology to calculate days’ supply.

Michelle Krebs is executive analyst at Cox Automotive.