Data Point

With Steady Sales, New-Vehicle Inventory Begins to Look and Feel “Normal”

Thursday October 17, 2024

Article Highlights

- Inventory and days’ supply start to feel familiar when considering the last time markets felt normal in 2019.

- Newer metal continues to pour into dealerships, but with sales running 4% higher year over year, new-vehicle inventories remain stable.

- The U.S. consumer still prefers SUVs and trucks but will sacrifice size for more affordable models.

This has been the year of automotive market “blips.” In just the last four months, we have seen an industry-wide disruption due to a cyber breach, two major hurricanes within two weeks of each other, and significant selling-day variations in the last two months. And let’s not forget business disruptions in both factories and the major ports of the East and Gulf coast, several key model stop-sales, and finally, an election season that has everyone on the edge of their seat.

Perhaps most surprising, despite all the blips, things look remarkably “normal” in the recent new-vehicle inventory and sales data. According to an analysis of vAuto Live Market View data, sales volume and days’ supply at the start of October look to be getting back on track with the last year we all recall as “normal,” 2019.

2.76M

Total Inventory

as of Oct. 3, 2024

81

Days’ Supply

$47,823

Average Listing Price

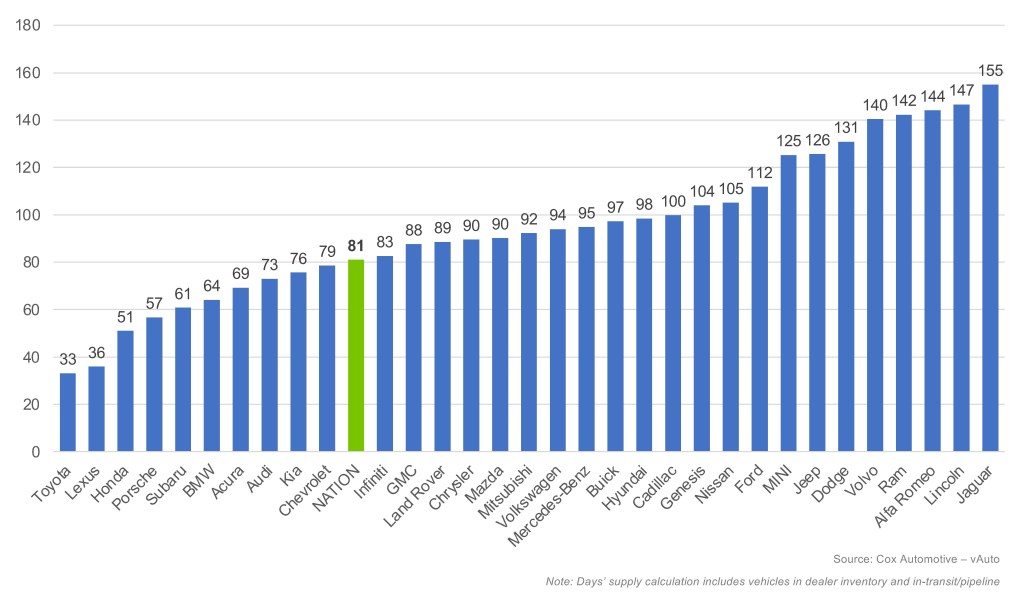

A new-vehicle days’ supply of 81 at the start of October is just one day more than the 80 days we saw back at the beginning of October 2019. Days’ supply continues to run below the average 83 days we saw in the first six months of the year and is up two days from last month. Considering the sales pace has declined 5.7% month over month and automakers continue to add MY25 vehicles to showroom floors, 81 days should warrant a feeling of steadiness.

The total U.S. supply of available unsold new vehicles opened October at 2.76 million units. This is up 25% year over year but down 20% from 2019 levels. Keep in mind that most dealerships have approximately 37% fresh MY25 product on their showroom floors, with automakers providing more incentives to move older metal.

In September, incentive spending rose modestly to 7.3% of the average transaction price ($3,522), according to the latest measure from Kelley Blue Book, up from 7.2% in August and well above the 4.8% reported one year ago. At this time in 2019, the market saw incentives at 10.3% of the average transaction price, suggesting there is still room to go if the going gets tough.

On Monday, at the Paris auto show, Stellantis CEO Carlos Tavares restated his intention to see U.S. inventories get below 350,000 before the end of the year. Cox Automotive data show incentive spend by Stellantis is increasing while MY23 vehicles are moving, which should begin to appease the U.S. Stellantis dealers. Notably, Dodge went from 22.5% prior model year inventory last month to 19.1% this month and reduced days’ supply by 18 days, now sitting at 131 days’ supply. Chrysler brand has moved closer to industry average. There are signs of improvement at Jeep and Ram, but there is still a lot of work to do between now and Dec. 31, if CEO Tavares intends to get his holiday wish.

SEPTEMBER DAYS’ SUPPLY OF INVENTORY BY BRAND

New Model Year Vehicles Push Prices Higher

The average listing price for a new vehicle in the latest report was $47,823, up just over 2% from a month earlier and up 0.9% compared to last year. As more MY25 models enter the showroom and used-vehicle inventory tightens, prices will likely remain stable.

The top 10 sellers in the U.S. continue to prove that the American consumer prefers a sub-$40,000 vehicle, but with four of the top 10 models listed at above $45,000 and as high as $61,669 (GMC Sierra 1500), full-size SUVs and trucks are still popular. The Honda CR-V, Toyota RAV4 and Chevrolet Trax show that the smaller SUV equals more affordable in most consumers’ minds, while the Toyota Camry and Honda Civic sales success suggest the sedan market is alive and well.

The average transaction price (ATP) of a new vehicle in the U.S. in September was $48,397, elevated by 0.8% from the month prior, according to Kelley Blue Book. However, with optimism that the election cycle is nearing a close, consumer sentiment – according to Morning Consult – is at a three-year high. Interest rates are also projected to move lower, which should help consumers and dealers alike as affordability concerns abate and balance sheets improve.

Erin Keating

Erin Keating is an Executive Analyst and Senior Director of Economic and Industry Insights at Cox Automotive. She has 25 years of experience in marketing and communications, including 10 years with Audi of America, where she also ran Audi Motorsport North America. With a focus on the wider industry, the individual automakers, and consumer shopping and buying behavior for new vehicles, Erin provides analysis and insights leveraging the breadth and depth of data from DRiVEQ, Cox Automotive’s data intelligence engine. Upon joining Cox Automotive, Erin was responsible for Enterprise Data Strategy – Partnerships. Erin is based in Atlanta.