Revised, Feb. 16, 2022 – New-vehicle inventory, particularly for domestic automakers, continued to climb, exceeding 1 million units near the end of December, according to a Cox Automotive analysis of vAuto Available Inventory data. Prices also kept rising, setting new records, with the average listing price exceeding $45,000.

1.09M

Total Inventory

as of Dec. 20, 2021

35

Days’ Supply

$45,778

Average Listing Price

The total U.S. supply of available unsold new vehicles stood at nearly 1.1 million near the end of December. That compared with the revised November available supply of 935,100 vehicles. December marked the first time since early August that supply hit and even edged past 1 million units.

Still, available supply is down 62% behind the same period in 2020. In raw numbers, the current supply of unsold new vehicles is more than 1.8 million vehicles less than the stock of a year ago and more than 2.5 million less than in 2019.

The days’ supply of unsold new vehicles was 35 as January opened, up from 30 at the start of December. The total days’ supply bottomed out at the end of September at 25. Still, the day’s supply at the end of December remained 48% below the end of 2020.

For comparison, new-vehicle inventory in December 2020 was about 2.9 million units for a 68 days’ supply. In pre-pandemic December 2019, supply was 3.5 million vehicles for an 82 days’ supply, according to Cox Automotive data.

The Cox Automotive days’ supply is based on the daily sales rate for the most recent 30-day period. Because of improved inventories throughout the month, December sales came in a bit above forecast. Full month December sales were down 26% from December 2020, with one more selling day. The December seasonally adjusted rate of sales was 12.4 million, down from 12.9 million in November. Compared to earlier years, the December 2021 SAAR was well below 2020’s 16.3 million and 2019’s 16.9 million.

The following commentary, while directionally correct, is unrevised from the original publication on Jan. 14, 2022.

“Inventory levels have been improving modestly, and sales in December increased from November reflecting this supply improvement,” said Charlie Chesbrough, Cox Automotive senior economist. “The expectation is that this trend will continue throughout 2022 as many of the supply chain disruptions of 2021 begin to fade away. However, the rise of the Omicron variant has the potential to disrupt production capabilities yet again, so the risks to the vehicle market, and its available supply, remain elevated.”

There is widespread agreement that the global computer chip shortage that hit vehicle production last spring will continue through 2022. Opinion as to what degree varies widely. Generally, most auto company executives and analysts expect the chip supply and, thus, vehicle production will be much improved through 2022, particularly in the second half. Still, continued tight inventories are forecasted as consumer demand for vehicles, supported by postponed purchases and strong economics, stays high as the near-empty pipeline of new vehicles is refilled.

Prices keep climbing

In December, the average listing price – or asking price – for new vehicles set another record $45,778, up from a revised $45,084 at the end of November. By comparison, in the same period of December 2020, the average listing price was $40,650. In December 2019, it was $38,362, according to Cox Automotive data.

Average transaction prices (ATP) – the price buyers actually paid – also set a record of $47,077, according to a Kelley Blue Book report. December marked the ninth straight month of ATP increase. The average incentive declined to $1,816, at least a 20-year law. The average incentive as a percent of the average price fell to an all-time low of 3.9%.

The average listing price for luxury vehicles was $65,389 in December, a big jump from $63,845 in November. The non-luxury average listing price was $41,994, up from $41,376, according to Cox Automotive data.

December sales drain luxury inventory

As is traditionally the case, December was a strong month for luxury sales, driven by better-than-expected inventory throughout the month. Of the more than 1.1 million new vehicles in inventory at the end of December, 146,591 were luxury vehicles for a days’ supply of 32; 948,522 were non-luxury vehicles for a 35 days’ supply. Ultra-luxury vehicles rounded out the supply.

In December, the number of days it took to sell a vehicle – just under 27 – and the number of days a vehicle remained in inventory sunk to record lows, according to Cox Automotive’s data.

The lowest supply is in the cheapest price category, below $20,000, where there are few offerings to begin with, and inventory fell to under 4,500 vehicles for an 18 days’ supply. Price categories between $20,000 and $50,000, the bulk of the market, had between 31- and 33-days’ supply, up from the previous month. Vehicles priced above $50,000 had about a 40 days’ supply.

Domestics build inventory; Asian and luxury brands have lowest supply

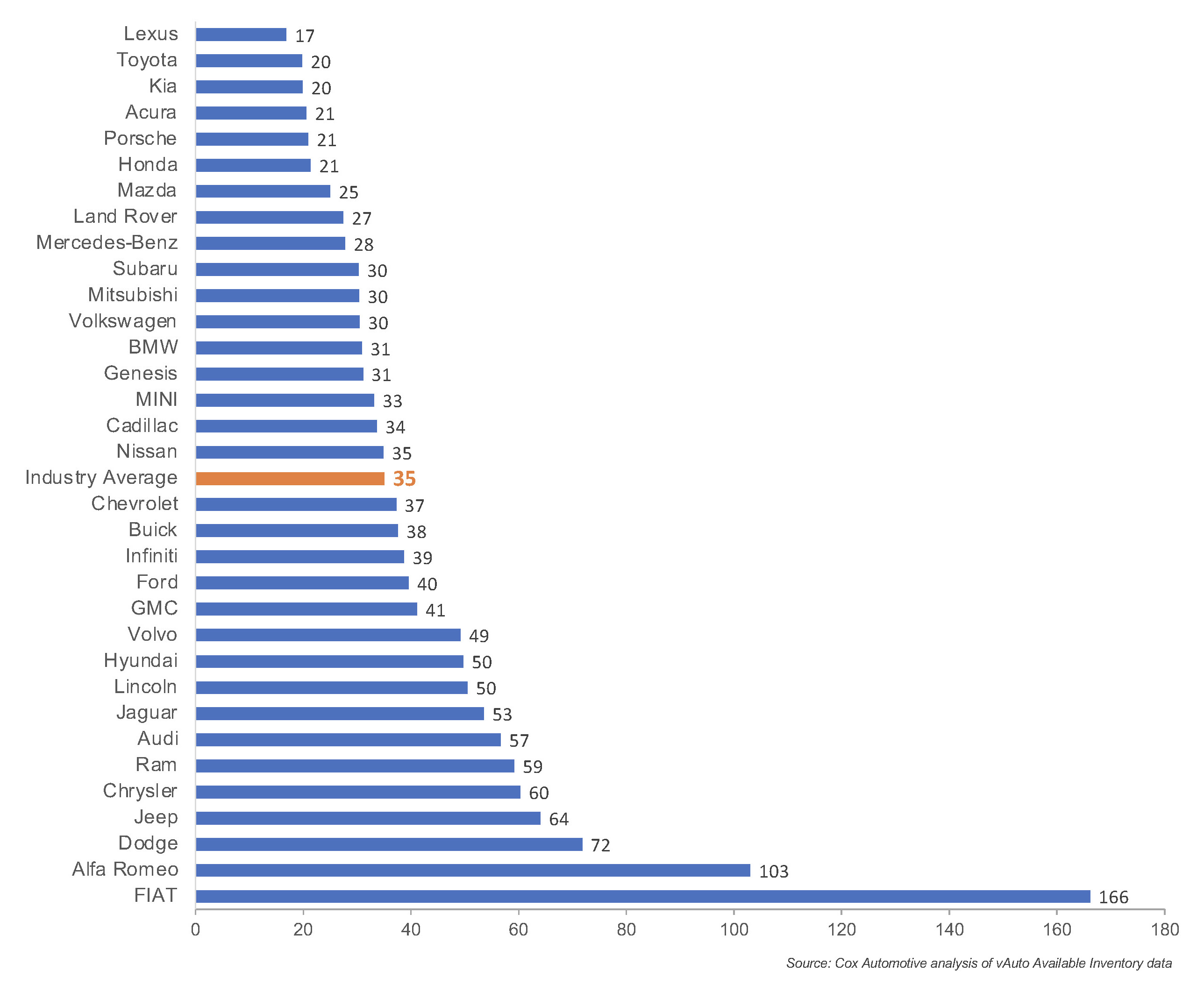

Domestic automakers saw inventory build in December. Of domestic brands, only Cadillac was below average and only by a bit. Stellantis brands – Alfa Romeo, Dodge, Jeep, Chrysler and Ram – had the most inventory.

National Days’ Supply By Brand

Lexus and Toyota, respectively, remained at the bottom for inventory. Toyota hopes to catch up, scheduling record production in January.

Following brisk December sales, luxury brands saw their inventories depleted. Acura, Porsche, Land Rover and Mercedes-Benz, BMW and Genesis had below-average inventory along with Lexus. On the non-luxury side, Kia, Honda, Mazda and Subaru were at the low end.

In terms of segments, small to mid-size car supplies were in the lowest supply, largely because Asian automakers are the biggest producers and sellers of cars. SUV categories, especially luxury ones, were below average in supply as well.

Larger and entry-level luxury cars had higher supplies. Full-size pickups, dominated by domestic automakers, were building in inventory.

More insights are available from Cox Automotive on new-vehicle inventory, using a 30-day rolling sales methodology to calculate days’ supply.

Michelle Krebs is executive analyst at Cox Automotive.