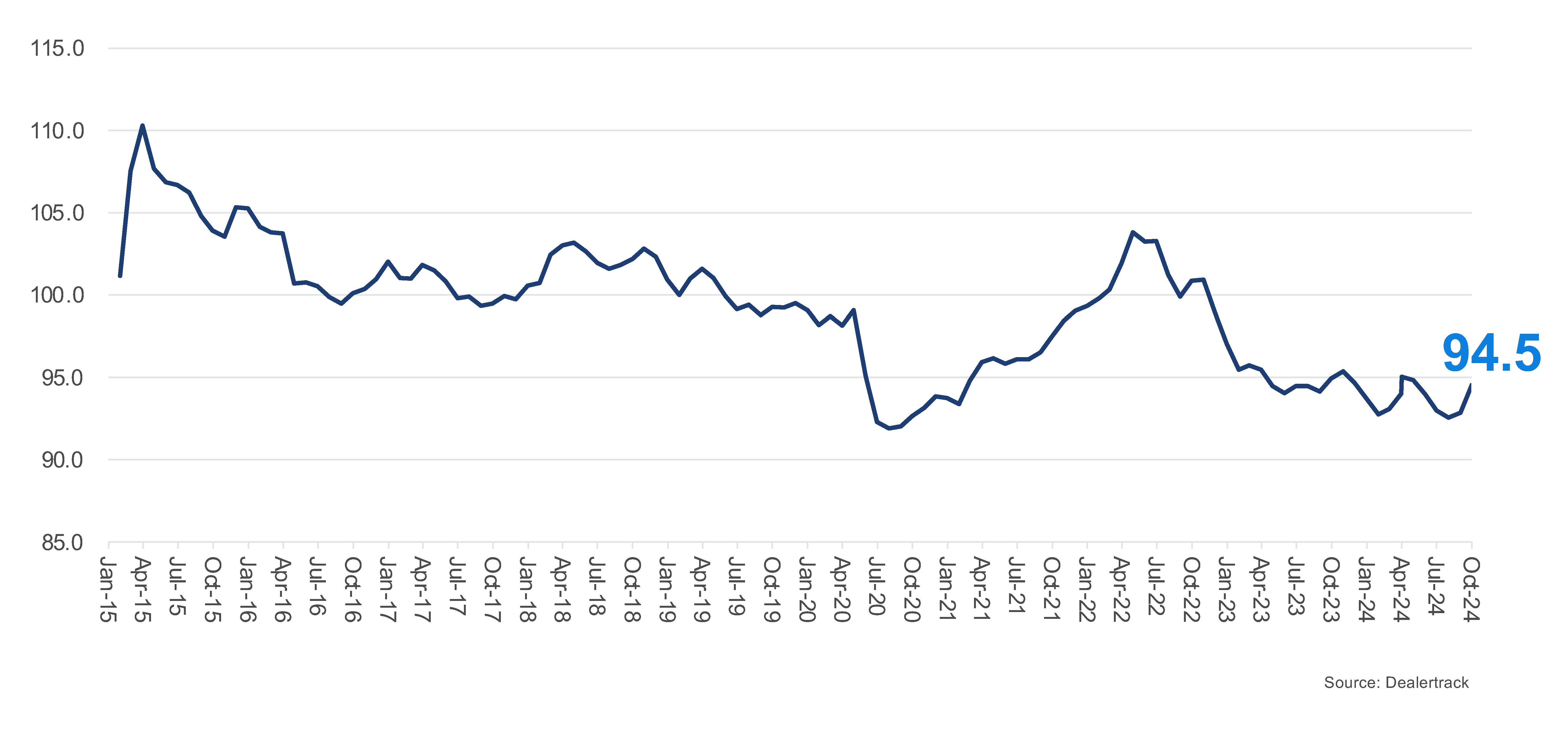

Access to auto credit increased in October as credit loosened across all channels and across all lender types, according to the Dealertrack Credit Availability Index. The All-Loans Index was 94.5 in October, up 2.2% from the September reading but down 2.1% year over year. This marks the largest month-over-month increase in auto credit access since March 2022.

Dealertrack Credit Availability Index1

Auto loan access improved in October but remained down year over year

All Auto Loans Index (Jan2019=100)

The Dealertrack Credit Availability Index improved due to increased approval rates, a higher share of subprime loans, and the shortening of yield spreads, all contributing to easier access to consumer credit.

Credit Availability Loosens in October Across All Channels

Credit availability eased in October for all sales channels. This marks a second consecutive month of easing after tightening the entire summer. Certified pre-owned loans loosened the most, while credit availability for used loans loosened the least. Consumers financing non-captive new loans and used loans through independent dealers have better access to credit than pre-pandemic levels. Overall, credit access was tighter than a year ago, with new loans showing the least tightening and certified pre-owned loans experiencing the most tightening compared to last year.

Lenders Show Significant Credit Availability Improvements in October

In October, credit availability increased for all lender types. Credit unions showed the most significant loosening, while auto-focused finance companies loosened the least. Still, auto-focused finance companies are the only lender type offering more access to credit now than before the pandemic. Compared to the previous year, auto-focused finance companies loosened the most, whereas banks experienced the greatest tightening.

Yield Spread Tightens as Approval Rates Drop, Subprime Share Rises

In October, the average yield spread on auto loans tightened by 52 basis points (BPs), making auto loan rates more favorable compared to bond yields. The average auto loan rate dropped by 11 BPs from September, while the 5-year U.S. Treasury increased by 41 BPs, leading to a smaller yield spread. Notably, auto loan rates have decreased by 124 BPs since March.

The approval rate increased by 20 BPs in October and fell by 2.6 percentage points compared to the previous year. Meanwhile, the subprime share increased by 20 BPs in October and increased by 1.2 percentage points year over year. This marks the third consecutive rise in subprime share.

Long-Term Auto Loans and Negative Equity Rise in October, Down Payments Fall

The share of loans with greater than 72-month terms fell 30 BPs after an increase last month and was down 0.9 percentage points year over year. The number of loans with negative equity decreased by 30 basis points in October, following four months of increases, but remained up 1.6 percentage points year over year. The down payment percentage was flat in October compared to the previous month. The down payment percentage has either declined or been flat every month since February but is up 1.6 percentage points compared to last year.

Each Dealertrack Auto Credit Index tracks shifts in loan approval rates, subprime share, yield spreads and loan details, including term length, negative equity, and down payments. The index is baselined to January 2019 to provide a view of how credit access shifts over time.

Measures of Consumer Confidence Improved in October

The Conference Board Consumer Confidence Index® jumped 9.6% in October, when only a slight increase had been expected, and September’s index was revised higher. Consumers’ views of both the present and the future improved. Consumer confidence was up 9.7% year over year. Plans to purchase a vehicle in the next six months increased substantially to the highest level since December 2019. According to the sentiment index from the University of Michigan, consumer sentiment increased 0.6% in October compared to September and was up 10.5% year over year. Views of the current situation improved, but expectations declined. The median consumer expectation for inflation in a year was stable compared to September at 2.7%, the lowest level since December 2020. The median expectation for inflation in five years declined to 3.0% from 3.1% in September. The consumers’ views of buying conditions for vehicles improved to the best level since April. The daily index of consumer sentiment from Morning Consult extended the streak of increases to five straight monthly gains. The index was up 1.4% for the month, which left the index up 10.3% year over year. According to AAA, the national average price for unleaded gas was $3.12 per gallon in October, down 2.6% from the end of September and down 9% year over year.

The Dealertrack Credit Availability Index is a monthly index based on Dealertrack credit application data and will indicate whether access to auto loan credit is improving or worsening. The index will be published around the 10th of each month.

1In November 2023, the data behind the Dealertrack Auto Credit Availability Index was reset by our data sciences team as part of a migration to a new data management system. All points in the data set were reestablished, with January 2019 in the index set at 100 (as it had been previously). The All-Loans Index plot used in this post utilizes the new data set. The absolute numbers have shifted, but the trends and narrative have not. For more information, contact the Cox Automotive team.