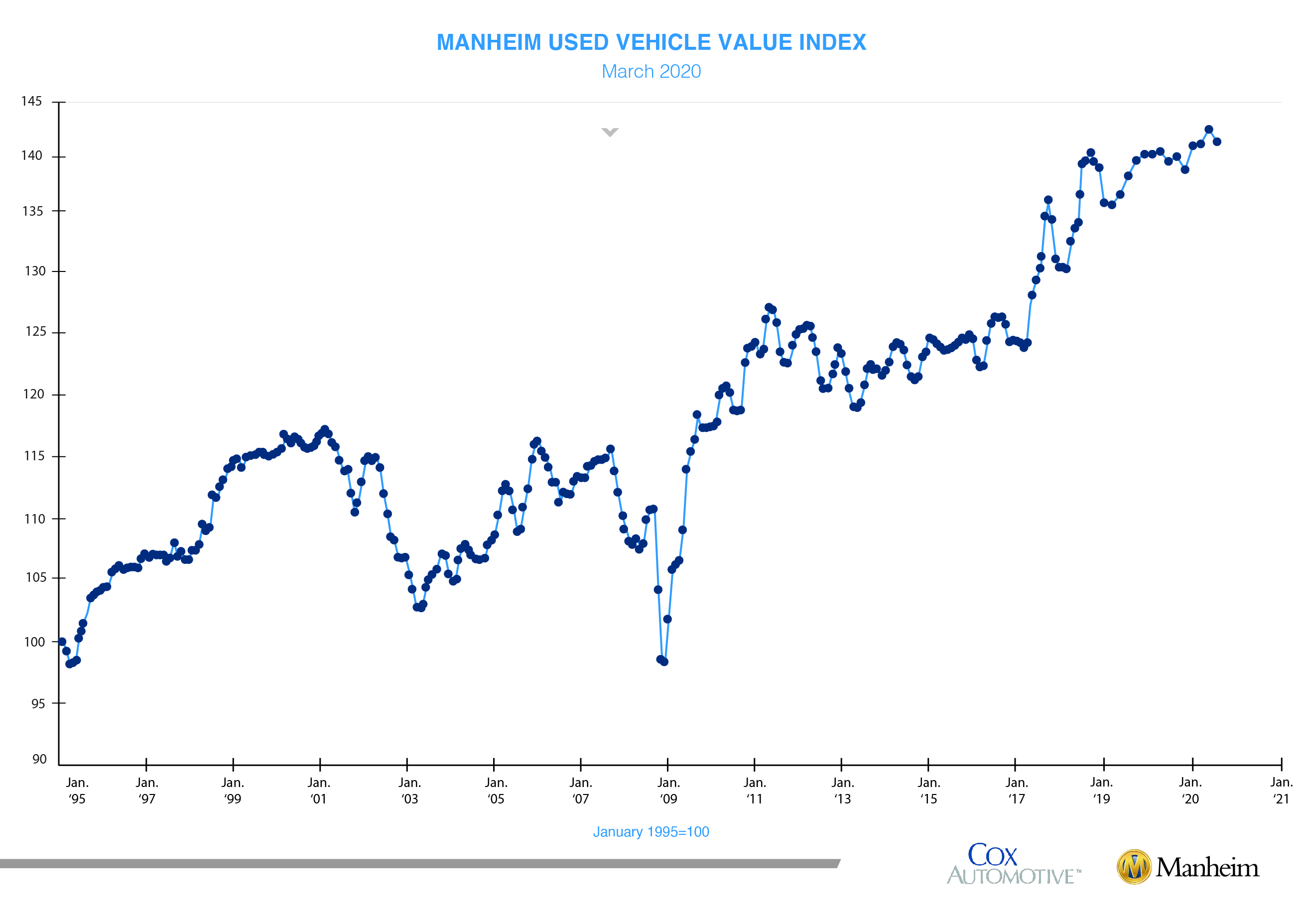

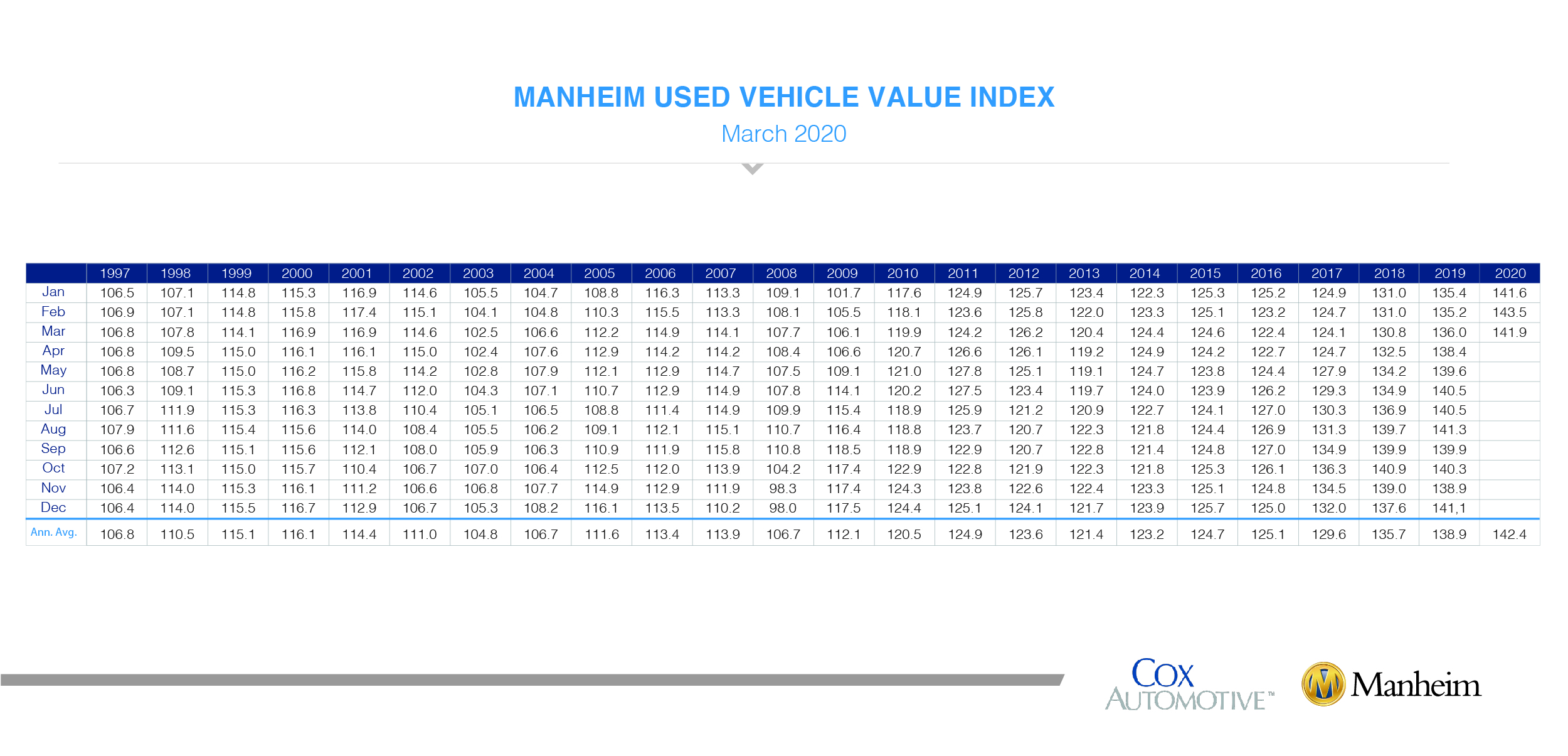

Wholesale used-vehicle prices (on a mix-, mileage-, and seasonally adjusted basis) decreased 1.10% month over month in March. This brought the Manheim Used Vehicle Value Index to 141.9, a 4.4% increase from a year ago.

After a start of increases in weekly Manheim Market Report (MMR) prices at the end of February, March saw the full-fledged start of tax refund season, which delivered the biggest weekly price increases since 2014. However, that all began to change as the month progressed. Three-year-old vehicle values in aggregate were up 1.7% after the first two weeks but began to decline and ended up 1% for the month. The worst-performing model year in March since the downturn began was MY 2019.

It should be noted that, given the unprecedented downturn in sales and market disruption that the industry is experiencing because of the COVID-19 pandemic, the decline we have observed thus far in MMR values at the vehicle level and at all aggregation levels does not fully reflect the declines occurring in the relatively limited number of sales transactions taking place.

On a year-over-year basis, most major market segments saw seasonally adjusted price increases in March. Luxury cars and SUVs/CUVs outperformed the overall market, while most other major segments underperformed the overall market.

Negative retail results for vehicle sales year-over-year. According to Cox Automotive estimates, total used-vehicle sales volume was down 18.4% year-over-year in March. We estimate the March used SAAR to be 32.0 million, down from 39.2 million last March and down from February’s 39.8 million rate. The March used retail SAAR estimate is 17.3 million, down from 20.6 million last year and down month over month from February’s 21.2 million rate.

March total new-vehicle sales were down 37.9% year over year, with two fewer selling days compared to March 2019. The March SAAR came in at 11.4 million, a decrease from last year’s 17.3 million and down from February’s 16.7 million rate.

Combined rental, commercial, and government purchases of new vehicles were down 27.6% year over year in March. Commercial (-17.7%) and rental (-34.3%) fleet channels were down year over year in March. Retail sales of new vehicles were down 40.5% year over year in March, leading to a retail SAAR of 8.7 million, down from 13.8 million last March and down from February’s 13.3 million rate. This is the lowest monthly retail SAAR since February 2010. Fleet sales are down 11.4% in 2020 through Q1, and retail sales are down 13.1%, as the overall new vehicle market is down 12.7% so far this year.

New vehicle inventories came in over 3.7 million units.

Rental risk pricing increased. The average price for rental risk units sold at auction in March was up 7.3% year-over-year. Rental risk prices were up 3.0% compared to February. Average mileage for rental risk units in March (at 45,900 miles) was up 1% compared to a year ago and down 12% month over month.

Coronavirus uncertainty amid declining conditions. National initial jobless claims jumped to 6.6 million for the week ending March 28. This was double the prior week’s record volume of 3.3 million. We will likely see a few more weeks of large new claims numbers, and we could see unemployment reach 10%–16% as a result. The U.S. lost more jobs in the last two full weeks of March than we did for the entire duration of the Great Recession. The extent of business closures, declining consumer confidence, and job and income losses point to the U.S. and most of the world heading into a recession quickly. The economic contraction in March and Q2 could be worse than at any point since WWII. The range of likely GDP real contraction for Q2 is from -10% to -18%.

The market and underlying economic conditions deteriorated rapidly in the second half of March; but because of the strong start of the month, the Manheim Index lost only 1.1% of its value. The decline in April is likely to be much more severe.

The Manheim Used Vehicle Value Index data file is available for download.

{kind=link}