The trend in new daily COVID-19 cases continued to increase as new variants spread. Vaccination progress accelerated, and we passed a critical milestone of more than 100 million Americans having received at least one shot of a vaccine.

The severe winter storms in February caused pending home sales to fall, just like we saw in new home sales, vehicle sales, and retail sales. But new-vehicle sales soared in March. Consumer confidence rose, and employment jumped as the jobs recovery accelerated, dropping the unemployment rate to a 12-month low.

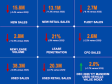

New-vehicle sales soar: Total new-vehicle sales were up 60% year over year in March with one more selling day compared to March 2020. The lockdown period that started in March last year made for an easy comparison. Against March 2019, total light-vehicle sales were down 1.2%, with all of the decline caused by sales into fleet.

The March SAAR was 17.8 million, a 56.2% increase from last year’s 11.4 million and a 2.5% increase from March 2019. It was the highest monthly SAAR since September and October 2018 following the aftermath of Hurricane Harvey.

Combined sales into large rental, commercial, and government buyers were down 20% year over year in March. A more complete report on new sales in March including retail sales, incentives, and pricing will be included in the next weekly summary.

Job picture improves: February saw an acceleration in the jobs recovery as job gains increased to 916,000 jobs, which was 41% more than the number expected and the best monthly gain since August. The prior two monthly numbers were revised up for a net increase of 156,000 more jobs than originally estimated.

The increases in March were widespread with the largest gains in leisure and hospitality, public and private education, and construction. Auto dealers added 9,100 jobs, which left dealership employment 5% below the February 2020 level.

The labor force participation rate increased 0.1% in March to 61.5%, which means that the decline in the unemployment rate was a result of an even larger gain in jobs than indicated by the change in the unemployment rate. The underemployment rate, which is the broadest measure of unemployment, declined to 10.7%. The percentage of the unemployed reporting being on temporary layoff, as opposed to permanent, declined to 20.9%, which was the lowest level since February 2020. The number of permanently unemployed declined by 65,000 in March.

The latest traditional continuing claims data from the week ending March 20 fell 46,000. The broadest measure of continuing claims, which includes pandemic unemployment assistance, has 18.2 million still on unemployment benefits in the latest data. Initial claims for the week ending March 27 increased by 61,000 to 719,000 claims, but the prior week’s numbers were the lowest in the pandemic thus far and were revised down from original estimates. Given restrictions declining as with the accelerating rollout of vaccines, initial claims should decline in future weeks.

Consumer confidence jumped: Consumer Confidence, according to the Conference Board, jumped 21.3% in March and left confidence down 17% compared to February 2020.

Plans to purchase a vehicle in the next six months increased in March to a 13-month high and even with purchase intention last June. Plans to purchase a home also increased in March to the highest level in the history of the Consumer Confidence data.

The Morning Consult Index measured 5.7% in gains in March after losing some momentum in the last week of the month. The index has resumed an upward trend to start April and is now down 12.8% since February 29, 2020.

Home sales fall: Pending home sales, which are based on new contracts signed, plunged 10.6% in February from January, leaving sales down 0.5% from a year ago. Contracts for the month were down in every region, but year-over-year contracts were up in the South and West and down in the Northeast and Midwest.

New home sales, which are also based on new contracts signed, declined 18.2% in February but were up 8.2% from a year ago. Severe weather impacted both types of sales. Pending home sales were likely more severely impacted by record low existing home inventory. The National Association of Realtors reported that “…only the upper-end market is experiencing more activity because of reasonable supply.”

An Auto Market Report video will be published in Smoke on Cars on Tuesday, April 6. To attend the Q1 2021 Manheim Used Vehicle Value Index call on Wednesday, April 7, at 11 a.m. EDT, RSVP now.