Revised March 16, 2022 – New-vehicle inventory, boosted by growing supply from domestic automakers, edged higher in the last weeks of January, according to a Cox Automotive analysis of vAuto Available Inventory data. Prices retreated from their December peak, dipping below $45,000.

1.06M

Total Inventory

as of Jan. 31, 2022

37

Days’ Supply

$44,814

Average Listing Price

The total U.S. supply of available unsold new vehicles stood at 1.08 million units at the close of January. That compared with the revised December available supply of 1.09 million vehicles. The supply dipped in the early weeks of January but edged higher in the later weeks of the month.

Still, available supply was down 60% from the same period in 2021. In raw numbers, the supply of unsold new vehicles as February opened was more than 1.6 million vehicles less than the stock of a year ago and 2.2 million less than in 2020.

The days’ supply of unsold new vehicles was 37 at the start of February, up from 35 in early January. The total days’ supply bottomed out at 25 at the end of September. Still, the days’ supply at the end of January remained 46% below the level at the end of January 2021.

The Cox Automotive days’ supply is based on the daily sales rate for the most recent 30-day period, in this case, ended January 31. New-vehicle sales in January dropped 10% from year-earlier levels. The January light vehicle seasonally adjust annual rate (SAAR) was 15.0 million, down from 16.8 million in January 2021 and 16.9 million in January 2020. January traditionally sees among the lowest sales volumes of any month.

“The new-vehicle supply continues improving just slightly, but sales remain stuck,” said Cox Automotive Senior Economist Charlie Chesbrough. “Sales should start gradually improving as well in the coming weeks from the inventory gains.” He forecast that production will increase with an easing of the chip shortage in the latter part of the year, and sales will rise. Prices will stay high but likely off their records.

Prices Dip Below Peak

After setting records month after month, the average listing price – or the asking price – dropped by the end of January to below $45,000 – $44,892, specifically. Still, that price was 12% above the average listing price in January 2021. The average transaction price – the price consumers paid – also decreased in January to $46,404, according to data from Kelley Blue Book, after reaching a record high in December 2021.

The lower overall average list price in January was driven mostly by a change in the mix of available vehicles. The good news for price-conscious shopper: The available inventory of vehicles priced below $30,000 increased in January compared to the end of December. At the same time, there were significantly fewer vehicles priced above $60,000. This inventory mix – more bargains, less luxury – helped push the national average down from the December record. Still, new-vehicle prices in the U.S. remain elevated and consumers are routinely paying above sticker for a new vehicle.

Import Brands Have Lowest Supply

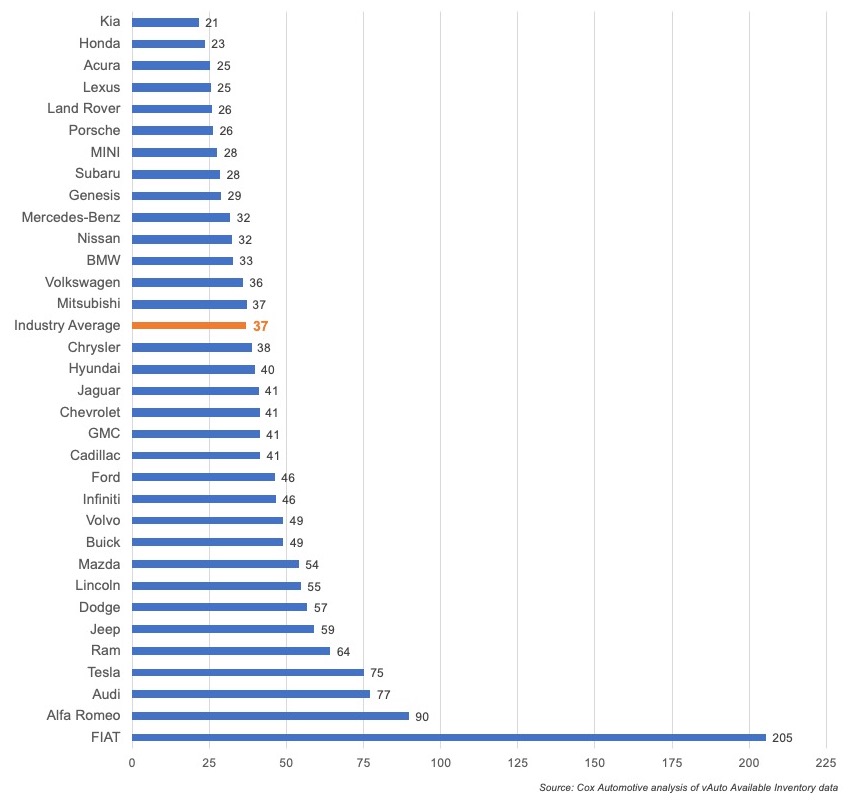

Brands with inventory levels below the industry average at the end of January were all imports. At the bottom were, starting with the lowest, Toyota, Kia, Honda, Acura, Land Rover, Porsche and Subaru. All domestic brands had above average inventory. Brands with the most, starting with the highest, were Buick, Volvo, Infiniti, Cadillac and GMC.

National Days’ Supply By Brand

Minivans returned to the bottom for inventory, due to Stellantis’ downtime at its Windsor, Ont., minivan plant again, and Toyota and Honda shortages. Also in short supply are large luxury crossovers, subcompact to midsize cars and hybrids along with most other SUV segments, particularly luxury ones.

Cars topped of the list for most inventory. Of the six segments with the most inventory, five were car categories. Full-size truck inventory also was building.

Specific models with the lowest inventories were all imports mostly from Honda, Toyota, Nissan and Subaru. An exception was the Chevrolet Tahoe. At the high end was Ram 1500 pickup, Mazda CX-5 and other domestic pickup trucks and SUVs.

In terms of price categories, the highest days’ supply was for vehicles priced between $50,000 and $60,000 and above $80,000. The cheapest vehicles – under $20,000 – had the lowest days’ supply at 28. All other segments had inventory between 32- and 37-days’ supply.

More insights are available from Cox Automotive on new-vehicle inventory, using a 30-day rolling sales methodology to calculate days’ supply.

Michelle Krebs is executive analyst at Cox Automotive.