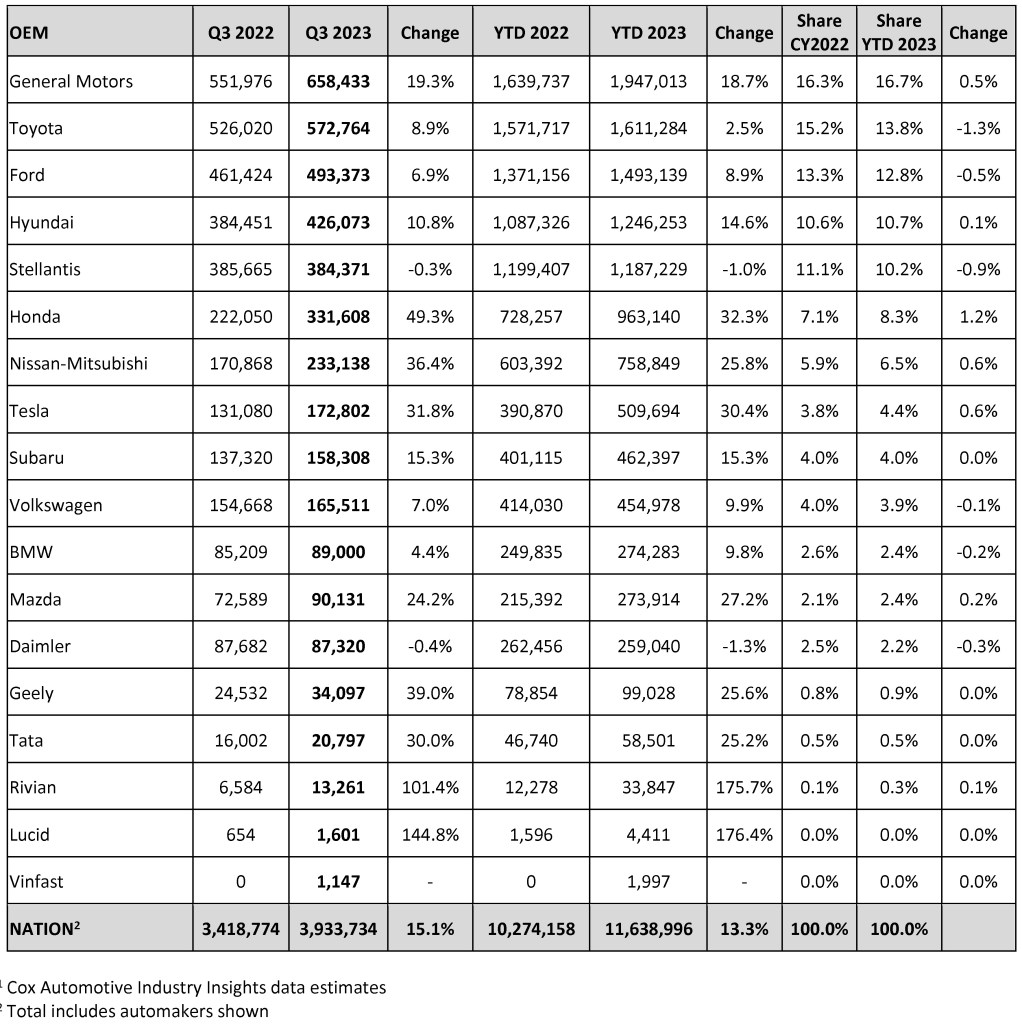

Updated, Oct. 4, 2023 – As forecast by Cox Automotive late last month, new-vehicle sales in Q3 in the U.S. were solid, spurred on by vastly improved inventories, higher fleet sales and consumers still in market despite elevated prices and high auto loan rates. Initial estimates suggest the Q3 new-vehicle market finished slightly above Cox Automotive’s 15%, 3.93 million forecast, up from 3.42 million in Q3 2022. Particularly strong results from General Motors, Toyota, Hyundai Motor Group and Nissan helped spur the bottom line.

Nearly all automakers posted double-digit percentage gains over year-ago levels. Honda sales jumped by almost 53%, and Nissan by more than 40%. Stellantis was an outlier, with sales volumes declining more than 1% year over year in Q3, driven partly by the strategic pursuit of higher transaction prices on lower volume. Stellantis buyers, historically, have also been more credit-challenged and are likely feeling more acutely the industry’s higher auto loan rates.

It is now all but certain that Hyundai Motor Group – which includes Hyundai, Kia and Genesis – in 2023 will move past Stellantis into fourth place in overall sales volumes, behind Ford Motor Company, Toyota, and General Motors. In 2019, Hyundai was 7th in the U.S. market by volume, behind Stellantis (then called Fiat) and also Honda/Acura and Nissan/Infiniti/Mitsubishi.

The story of 2023 is the recovery in new-vehicle inventory, and the Cox Automotive Industry Insights team will report end-of-September inventory levels later this week. As September began, new-vehicle inventory across the industry was 68% higher than in 2022; notes and commentary from the major automakers point to the higher inventory levels – more choice for consumers – helping fuel healthy sales. Cox Automotive data suggests higher incentives are helping as well. Fleet sales have also been significantly higher year over year in 2023. Sales into rental and commercial fleets have increased notably after a drought in 2021 and 2022, up roughly 60% and 40% year over year, respectively.

As our chief economist noted in a recent update on the UAW situation, there is little evidence in the September data that would suggest the strike against the domestic automakers impacted sales. That may change in October and Q4 if the strike continues and expands. GM seems to be the most exposed, with the lowest inventory levels. Stellantis is less so.

During the Cox Automotive Q3 Forecast Call last week, the team suggested that vehicle sales through the end of September had indeed been a pleasant surprise. Our full-year forecast, which was raised at the end of Q3, now puts the market on course to finish between 15.3 and 15.4 million. But as we head into Q4, there is no shortage of obstacles in place for both the consumer and the economy that will put downward pressure on the sales pace, particularly on the retail side.

ATLANTA, Sept. 26, 2023 – The U.S. auto industry’s robust year-over-year sales recovery continued in the third quarter, according to a forecast released today from Cox Automotive. Despite rising interest rates on new-vehicle loans and a strike by the United Auto Workers against the major domestic automakers, sales volumes in September are forecast to reach nearly 1.3 million, an increase of more than 13% from 2022. Sales in Q3 are expected to surpass 3.9 million, a jump of more than 15% from the same timeframe one year ago.

“As the first three quarters of 2023 come to a close, ‘pleasantly surprised’ may be the sentiment of many auto analysts,” noted Cox Automotive Senior Economist Charlie Chesbrough. “The market has faced high interest rates, real affordability issues, and ongoing inflation, which could have led to large declines in vehicle sales. However, pent-up demand has been fueling the vehicle market this year. Consumers, and even more so large fleets, have become buyers as inventory improves. Year-over-year sales gains have been surprising indeed.”

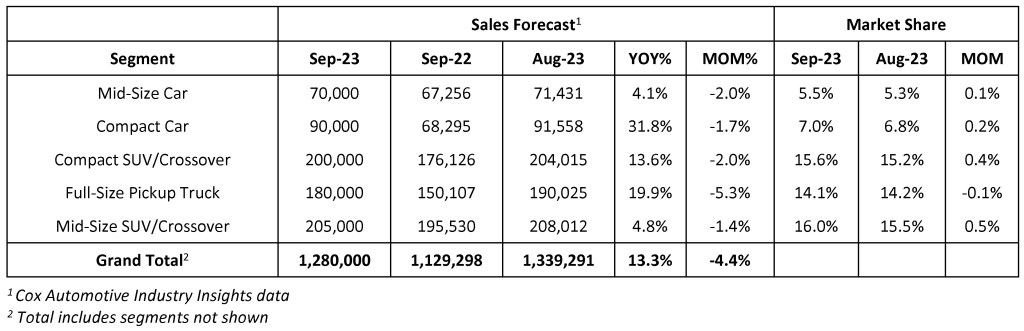

In the final month of Q3, the September seasonally adjusted sales pace, or SAAR, is expected to finish near 15.5 million. This is a modest increase from the 15.0 million level recorded in August and closer to the 15.7 million pace from July. In terms of volume, September’s sales are expected to show a more than 13% gain over last year’s supply-constrained market. Sales volume, however, is forecast to be lower by 4% compared to last month, mainly due to fewer selling days. September has 26 selling days, one less than August.

Q3 2023 U.S. New-Vehicle Sales Forecast

Supply Recovery Fuels Strong Q3 For Honda, Nissan; GM Outpaces Overall Market.

As Q3 draws to a close, industry-wide inventory levels are up more than 63%; inventory volume is above 2 million units, an increase of over 800,000 from year-earlier levels. Days’ supply is up 33%. Sales incentives have increased notably from the start of the year as inventory builds, enticing more consumers into the market.

“The market’s success this year, however, has not been a retail success story,” added Chesbrough. “According to our analysis, the market has enjoyed large increases in rental and commercial fleet sales – up 62% and 40% year to date, respectively.” During the recent new-vehicle inventory shortage, these channels had been starved of inventory. That, however, has been changing in 2023, and fleet sales have been rising.

General Motors will continue to be the industry leader in sales volume in 2023, with year-to-date sales forecast to be higher by nearly 19% through Q3. The other large players, including Toyota, Ford and Stellantis, are expected to underperform the industry through the first nine months.

In Q3, Honda and Nissan are forecast to beat the industry widely, with year-over-year increases of 49% and 36%, respectively. Tesla is also expected to post a positive Q3 performance, with sales up more than 31%. Tesla sales performance has been enhanced by price cuts of nearly 20% year over year.

Q3 2023 U.S New-Vehicle Sales Forecast1

All percentages are based on raw volume, not daily selling rate. There were 77 selling days in Q3 2022 and 78 in Q3 2023.

Following Strong Momentum in Q3, Cox Automotive Increases Full-Year Forecast

As the market enters the final quarter of 2023, the Cox Automotive Industry Insights team has increased its full-year new-vehicle sales forecast to between 15.3 and 15.4 million units, up from the forecast of 15 million at the end of the first half. Retail new-vehicle sales are forecast to end the year up 7% compared to 2022; fleet sales are forecast to increase by 40%.

“In the auto industry right now, interest rates are public enemy No. 1 – the leading factor holding back business,” said Cox Automotive Chief Economist Jonathan Smoke. “Limited Inventory was the leading factor one year ago, but now it’s interest rates, the economy and credit availability, which all make affordability more challenging. Ultimately, these are not good signs for demand continuing to be strong or improving in the fourth quarter.”

Smoke added, “The UAW strike is clearly a major factor that, should it persist, could reverse gains the industry has made on inventory. The “Stand Up” tactic by the UAW has so far minimized the initial disruption, but the approach could enable a much longer disruption than has been possible historically. So far, the impact has been negligible.”

About Cox Automotive

Cox Automotive is the world’s largest automotive services and technology provider. Fueled by the largest breadth of first- and third-party data fed by 2.3 billion online interactions a year, Cox Automotive tailors leading solutions for car shoppers, automakers, dealers, retailers, lenders and fleet owners. The company has 25,000+ employees on five continents and a family of trusted brands that includes Autotrader®, Dealertrack®, Kelley Blue Book®, Manheim®, NextGear Capital™ and vAuto®. Cox Automotive is a subsidiary of Cox Enterprises Inc., a privately-owned, Atlanta-based company with $22 billion in annual revenue. Visit coxautoinc.com or connect via @CoxAutomotive on Twitter, CoxAutoInc on Facebook or Cox-Automotive-Inc on LinkedIn.

Media Contacts:

Mark Schirmer

734 883 6346

mark.schirmer@coxautoinc.com

Dara Hailes

470 658 0656

dara.hailes@coxautoinc.com